“I suppose leadership at one time meant muscles; but today it means getting along with people.”

-Mohandas K. Gandhi

Yesterday, the ratings agency Standard & Poor’s downgraded their view of U.S. government debt from “AAA” stable to “AAA” negative for the first time since the attack on Pearl Harbor. The implication of this new rating is that there is now a 33% chance that the S&P downgrades U.S. government debt in the next two years. To be clear, our view of ratings agencies hasn’t changed—they are lagging indicators at best.

In this instance, though, Standard & Poor’s did provide insight on the current political debate in Washington. The basis of their call is that they believe it unlikely that the politicians in Washington will come to an agreement on a budget plan that will narrow the deficit over the long term. This is the point we made in our Q2 Theme call last Friday, so of course we agree.

On the Republican side of the debate is the budget proposed by Congressman Paul Ryan from Wisconsin whose key tenets are to cut taxes, cap the size of Medicare and Medicaid, and to dramatically slash discretionary spending. Conversely, the budget plan presented by President Obama raises taxes on the rich, cuts discretionary spending somewhat, and takes a hatchet to defense spending. These are meaningfully substantive and philosophical differences with very little common ground as a starting point for negotiation.

The reaction from the Obama Administration to the rating change from Standard & Poor’s was interesting. The White House effectively dismissed the action, while the Treasury Department doubled down on the politicians in Washington. In fact, according to Assistant Treasury Secretary Mary Miller, Standard & Poor’s revised outlook “underestimates” the nation’s leadership. I’m not sure exactly what Ms. Miller thinks is being underestimated about the politicians in Washington, but fair enough.

I used the quote above from Ghandi to underscore the core of leadership, which is getting things done in conjunction with your perceived adversaries. Unfortunately, many of our perceived leaders have failed the nation on this front in the last week. President Obama failed us by turning a prime time speech about his deficit reduction plan into a campaign speech that alienated Republicans, including Congressman Paul Ryan who was stoically watching the speech live. While Tea Party leader, and Presidential hopeful, Congressperson Michelle Bachman, failed us by once again bringing up the tired old questions about President Obama’s place of birth last weekend, rather than focusing on the critical deficit issues facing the nation.

If Standard & Poor’s action yesterday did anything, it brought the lack of political leadership to solve the deficit issue completely into the mainstream. Not surprisingly, stock market operators cast their votes appropriately. While the SP500 closed above our TREND line of 1,302, it did so barely at 1,305 and it is still trading below the TRADE line of 1,319. Volume also confirmed this vote as it accelerated 28.8% on the NYSE week-over-week. Volatility did the same with the VIX up 11%.

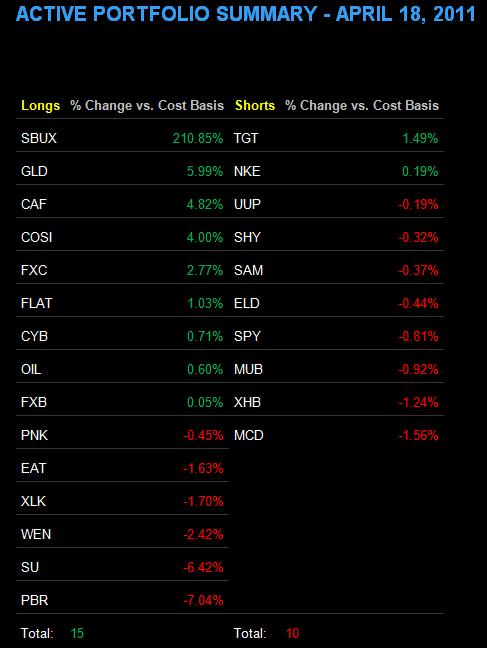

From a sector study perspective, financials became the first of the primary SP500 sectors to break down with yesterday’s market action. On some level, this is likely the early anticipation of the ending of quantitative easing, which removes the politicization of the short end of the yield curve and hurts the lucrative business of borrowing short and lending long. As we’ve posted below in The Chart of the Day, the spread between 2s and 10s is at a near all-time high in spread. (As a way to play this reversion to the mean, we are long the etf FLAT in the Hedgeye Virtual Portfolio, which is a Treasury curve flattener position.)

Our Financials Sector Head Josh Steiner also provided some color as a rationale for yesterday’s quantitative breakdown in the sector:

“Mortgage-related costs are on the rise and managements are being more open about the accelerating deterioration of fundamentals in that business. Bank of America stated on their call that multiple charges taken in the quarter were tied to ongoing home price deterioration. MSR write-downs at other banks are an additional indication of ongoing deterioration in that business, as JPMorgan highlighted with their $1.1 billion write-down.

While most companies are beating on the bottom line it is largely being driven by credit-related improvement, but this is illusory. Most of that credit improvement comes from reserve release, specifically in the credit card business. For instance, JPMorgan’s card services provision was $226 million in 1Q11 as compared with $1.6 billion in 3Q10. One might assume that credit losses had fallen to $226 million, but in reality net charge-offs were $2.2billion in 1Q11. In other words, the company released $2 billion in reserves (defined as the difference between losses and provisions).

This reserve releasing has been substantially propping up earnings for the last several quarters, but will be coming to an end in the next few quarters as delinquencies in that business are nearing their trough.

The catch? The banks have been using reserve release from their card operations to offset growing pressure and recurring “one-time” charges in their mortgage business. Reserve release in cards will end in the next few quarters but mortgage-related weakness will persist for much longer.

Bigger picture, the industry continues to face an environment of little to no loan growth, rising margin pressure, falling non-interest income and, in 2Q11, significantly rising FDIC deposit insurance premiums for most of the large banks. From a macro standpoint, the start of the Consumer Financial Protection Bureau on July 1, 2011 will coincide with the end of QE2 on June 30, 2011, both of which are likely to be incremental headwinds for the sector.”

Needless to say, Josh isn’t overestimating the future stock performance leadership of the financial sector.

Broadly, we will see this week which bell weather companies will lead, follow, or get out of the way as earnings seasons kicks off in full force. Today, Goldman (this morning), Intel, IBM, and Yahoo all report earnings.

One last leadership quote today from the venerable Nobel Laureate Paul Krugman, who said this about the Standard & Poor’s ratings change:

“That said, it’s worth remembering that S&P downgraded Japan in 2002… Japanese bonds became known as the “trade of death”, because people kept betting on an interest rate rise, and it kept not happening. So, no big deal.”

So according to Dr. Krugman, emulating Japanese fiscal and monetary policy is no “big deal”. I’m no Nobel laureate and my PH.D is from the School of Hard Knocks, but even I know that becoming Japanese economically IS a big deal.

Keep your head up and stick on the ice,

Daryl G. Jones

Managing Director