“It would be very advantageous to allow the currency to appreciate as a way of controlling inflation.”

-George Soros, April 10th, 2011

That’s a very simple but critical comment Soros made last week at the Bretton Woods meetings in New Hampshire. He wasn’t talking about the US. He was talking about China.

He or she – whoever the overlord of policy making may be – should be thinking long and hard about what a US Currency Crash not only means for The Inflation that’s priced in US Dollars, but what they can do to fight it for the sake of their starving citizenry.

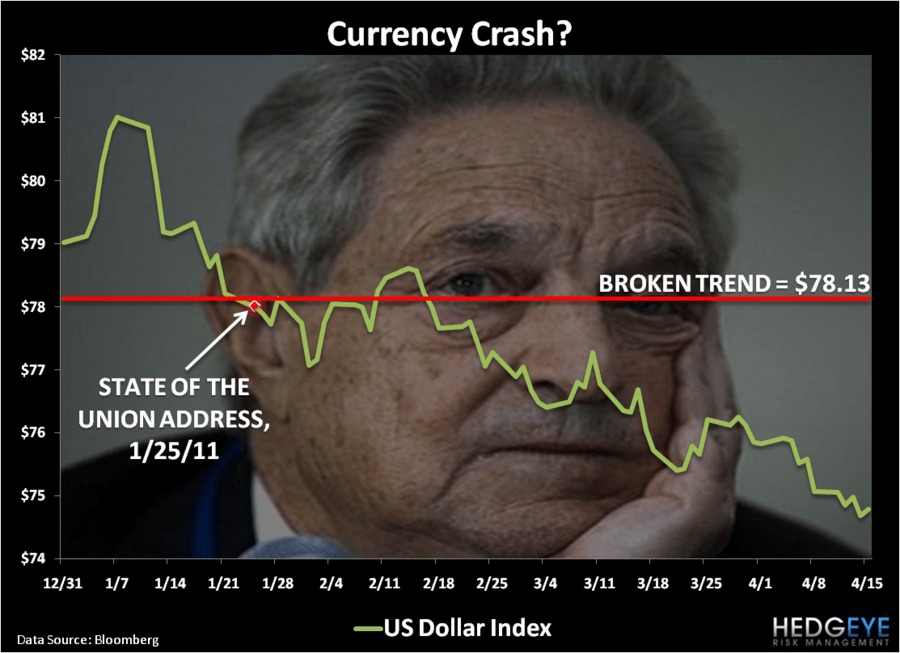

US Currency Crash?

It’s in motion folks – and if it happens, I think it happens in the next 3 months.

That should read as a bold statement, because it is… And the best way to put a picture with that prose and turn up some volume will be to dial into our Q2 Global Macro Theme conference call today at 11AM EST (email if you’d like to participate).

As is customary, Big Alberta and his Hedgeye knights have prepared the anchor with a 50 slide presentation that will lock us into making the risk management calls that we don’t think you can afford miss.

As a reminder, with the intermediate-term TREND overlay of Growth Slowing As Inflation Accelerates, our Q1 Global Macro Themes were:

1. American Sacrifice - a scenario analysis and calendar of catalysts for the US Dollar

2. Trashing Treasuries – long of The Bernank’s Inflation, short US Treasuries

3. Housing Headwinds II – part deux in the Josh Steiner chronicles of the best Housing work on Wall Street

This morning’s call will focus on what an expedited US Currency Crash could look like and the following Q2 Global Macro Themes:

1. Year of The Chinese Bull

2. Deflating The Inflation

3. Indefinitely Dovish

While we realize we have a target on our foreheads for calling out places like The Lehman Brother, The Bear Stearn, and The Banker of America, we have grown accustomed to it and we wear it with pride.

Living a risk management life of consensus and strong buy versus maybe buy it after we tell our super duper clients to sell into you isn’t a life to live. At Hedgeye, the name on the front of our jerseys mean more than the ones on our backs. We don’t make contrarian calls for the sake of being contrarian. We make these calls because we think they have the highest probabilities of being right.

Maybe we’re a little artsy with our Soho office. Maybe we’re a little jocky with our dressing room in New Haven. But when we make a call, there is no maybe – it’s long or short – and it’s on the tape.

On the Currency Crash call, I’ll save the juicy details for 11AM. We didn’t need to have a super secret one-on-one in Washington with a “consultant” to the professional politicians to make this call either. Over the last 3 years we’ve made 19 long and short calls on the US Dollar – and we’ve been right 19 times – so we’re going to stick with the process on that.

On The Chinese Bull…

Oh what a sexy call this one is going to be. The Hedgeyes versus the former roommate of a Yale Hockey player – Jim Chanos. We were bullish on China in 2009, bearish on China in 2010, and now we’re going to ride shotgun on this red bull before consensus does.

Last night’s Chinese GDP growth report beat our already above consensus estimate, coming in at +9.7%. While that’s a sequential slowdown versus the Q4 2010 China GDP report of +9.8% - that’s a deceleration in the slowdown – and on the margin, which is what matters most in making Global Macro calls, that’s what we call better than bad.

When better than bad is cheap (which Chinese equities are on an absolute and relative basis to both themselves and Asian Equities overall), that’s when shorts have to start covering. When better than bad is cheap and price momentum turns positive – that’s when Wall Street has to chase the asset’s price performance.

More on that and why we think Chinese inflation is setting up to deflate from the Elm City during our conference call. If it’s the beginning of the quarter, it’s Global Macro Theme time at Hedgeye.

My immediate-term support and resistance lines for oil are now $105.41 and $109.24, respectively (we bought our oil back this week at $106). My immediate-term support and resistance lines for the SP500 are now 1308 and 1325, respectively (we’re short the SP500).

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer