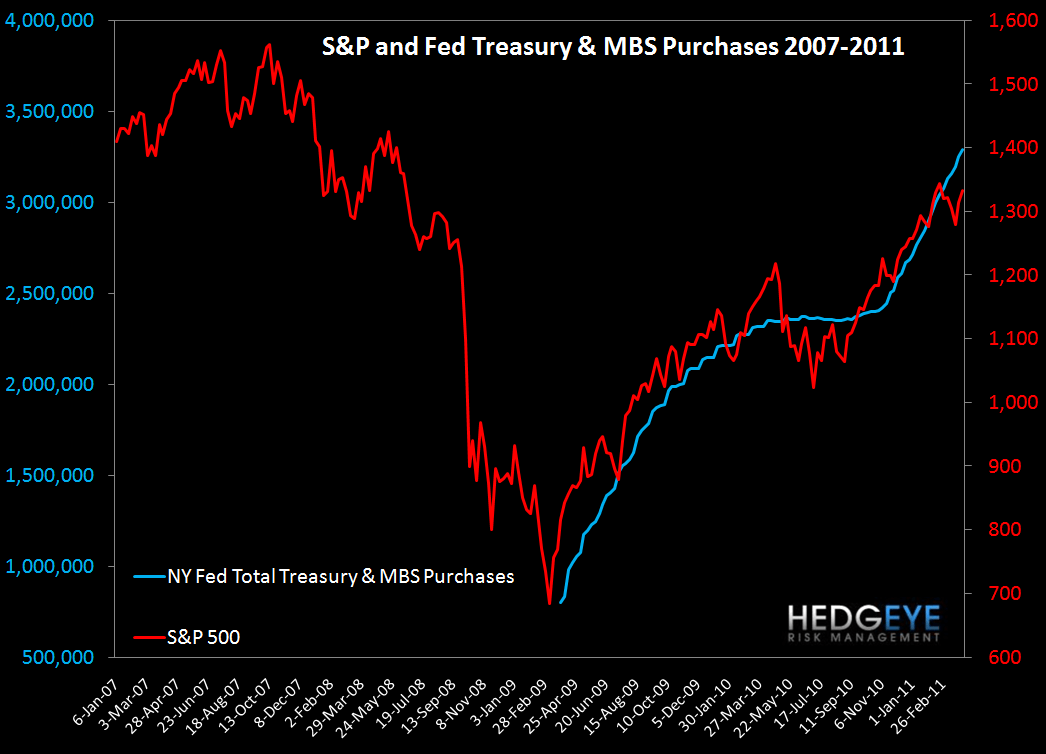

QE, Claims, and the Market

Inspired by a chart our macro team published last week showing Fed Treasury purchases and commodity prices, we show the impact of the Fed's Treasury and MBS purchases on the S&P and on claims. We observe in the charts below that the three series move in tandem. We see two plausible interpretations of this data.

1) Quantitative Easing drives claims down, which fuels an increase in the market.

2) Quantitative Easing drives the market higher, which decreases claims.

Regardless of which interpretation of this data you subscribe to, the reality is that QE2 ends in June, which cuts off this process at the source. The data suggests that in the absence of Fed purchases, the market and claims tread water or deteriorate. For this reason primarily, we are cautious on the Financials space overall heading into the summer months.

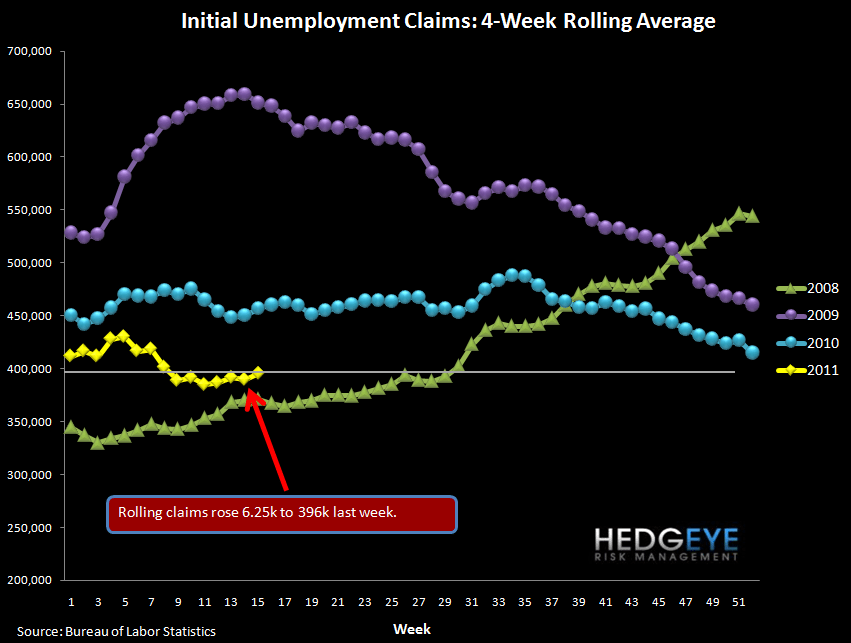

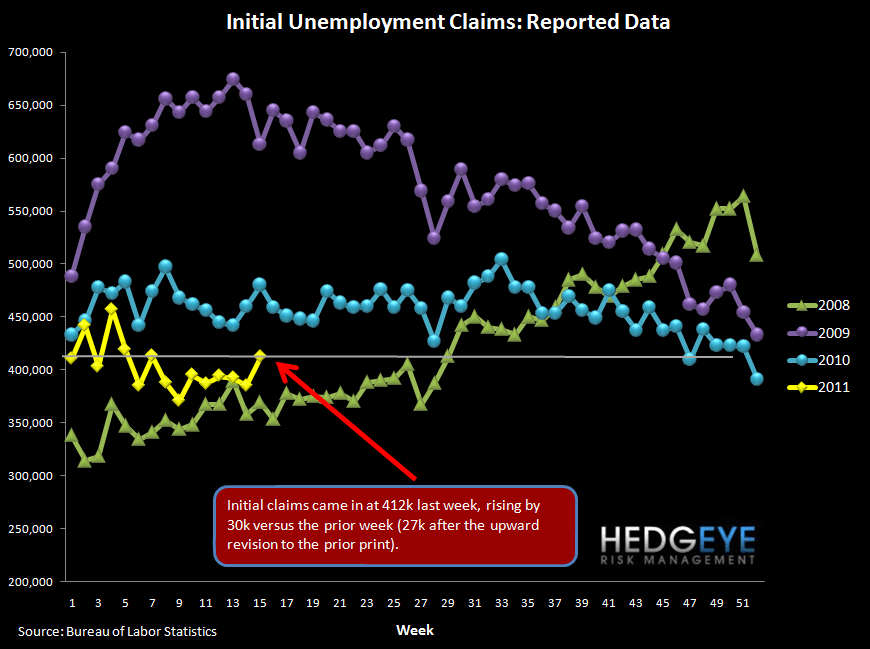

Initial claims rose 30k last week (27k after the upward revision to last week's preliminary report). This pushes claims back above the threshold of 400k that we watch as the trigger level for unemployment to fall. Rolling claims rose 6.25k to 395.75k.

The Bureau of Labor Statistics noted that the week following the end of a quarter usually sees an increase in claims. The week after the end of each quarter is marked with a white arrow in the chart below. Clearly, there is a seasonal pattern here. Last week, claims increased by more than the typical seasonal amount, which flowed through into the seasonally adjusted numbers and drove the 30k increase.

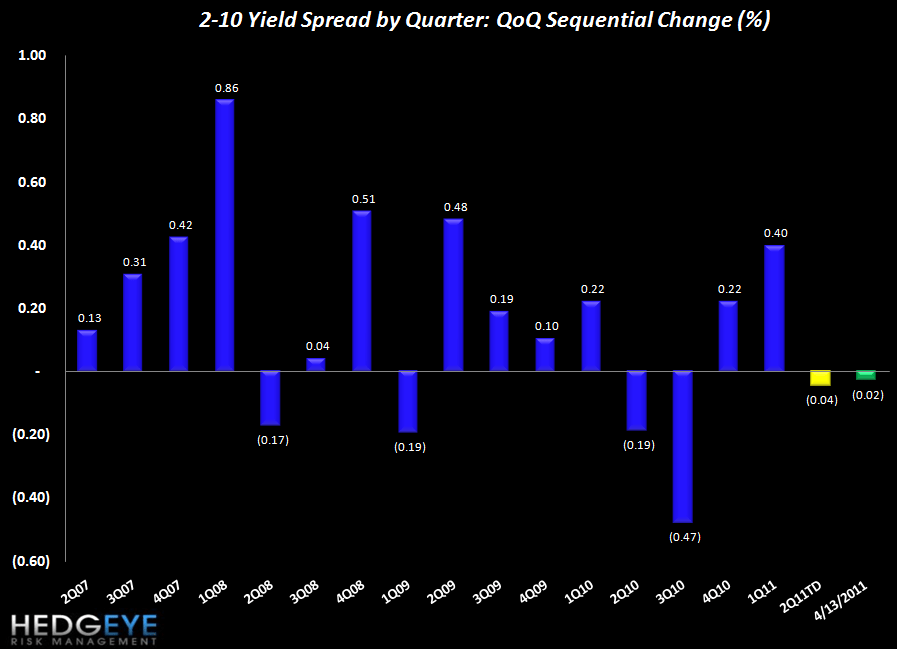

Yield Curve Remains Wide

We chart the 2-10 spread as a proxy for NIM. Thus far the spread in 2Q is tracking 4 bps tighter than 1Q. The current level of 273 bps is slightly tighter than last week (276 bps).

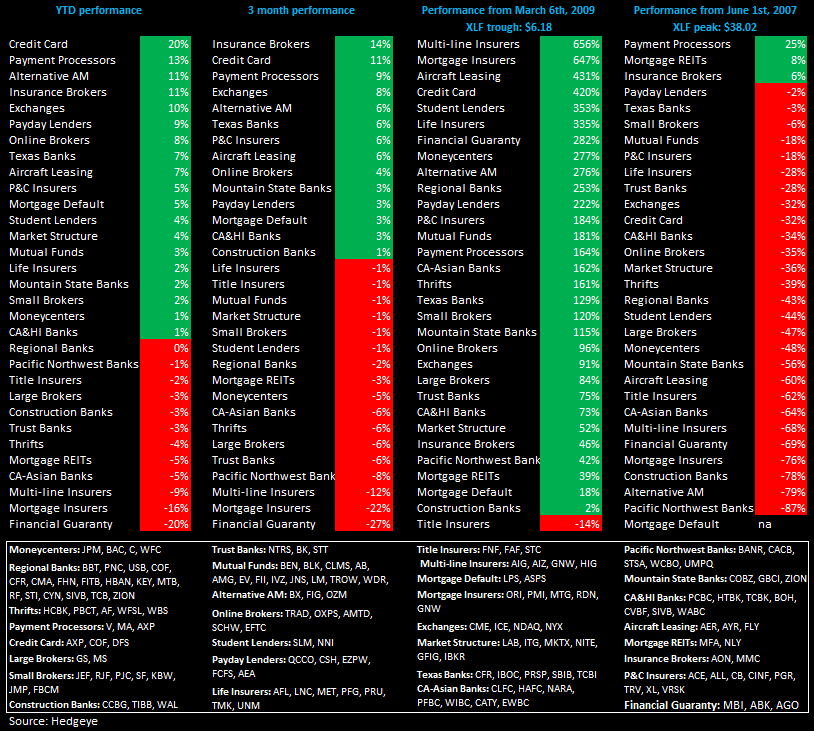

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur