Cheese prices bounced once again after a sustained period of trading down. The level of inflation in cheese has declined greatly but its rebound over the past week was the most substantial of all the commodities we monitor. All in all, looking at the table below shows more red than blue in the week-over-week column. Coffee continues to press higher, now up 94% year-over-year as it gained 2.2% over the past week. I continue to hold a cautious view of chicken producers (SAFM, TSN and PPC) despite corn’s week-over-week decline. The commodity surged 14% last week and, I believe, is likely to remain at these elevated levels for some time. This will likely lend support to protein (feed costs) and wheat (substitution effect) prices.

Cheese gained 3.2% on the week. As the chart below shows, cheese prices have come down considerably over the past month. Below, I gain provide some commentary from management teams from their most recent earnings calls with their views on cheese prices and the implications for their businesses.

DPZ:

"Yeah, so the forward curve and kind of looking at about three different sources right now have cheese actually easing a little bit through the rest of the year. We're at almost $2 right now. And so, our expectation is that we're going to see a little bit of easing, to give you on cheese. We've talked about this in the past, we've got a contract in place that basically reduces the volatility on cheese moves by about a third. So about two thirds of increases or decreases in cheese are passed through to our system.

I think the kind of consensus forecast out there right now for cheese are in the $1.70 to $1.75 range. And – you know so what you're looking at is kind of a $0.25 to $0.30 move and I think we've said in the past a $0.40 move in cheese is equal to a point at the store level P&L."

PZZA:

“We expect the favorable impact of early year sales results to substantially mitigate the unfavorable impact of currently projected commodity cost increases, most notably cheese, throughout the remainder of the year.”

DPZ is 95% franchised and, as such, management claims a degree of insulation from commodity costs. Of course, to the extent that price needs to be taken and royalties slow, the company is not immune from inflation. The downward move of cheese over the past month will raise hopes that a price increase can be avoided.

It’s also worth noting the strong week-over-week move in gas prices. Demand destruction is coming to the restaurant space this quarter. Clarence Otis, Darden CEO, said as much on DRI’s most recent conference call. Companies like CBRL (see post from yesterday), are particularly vulnerable.

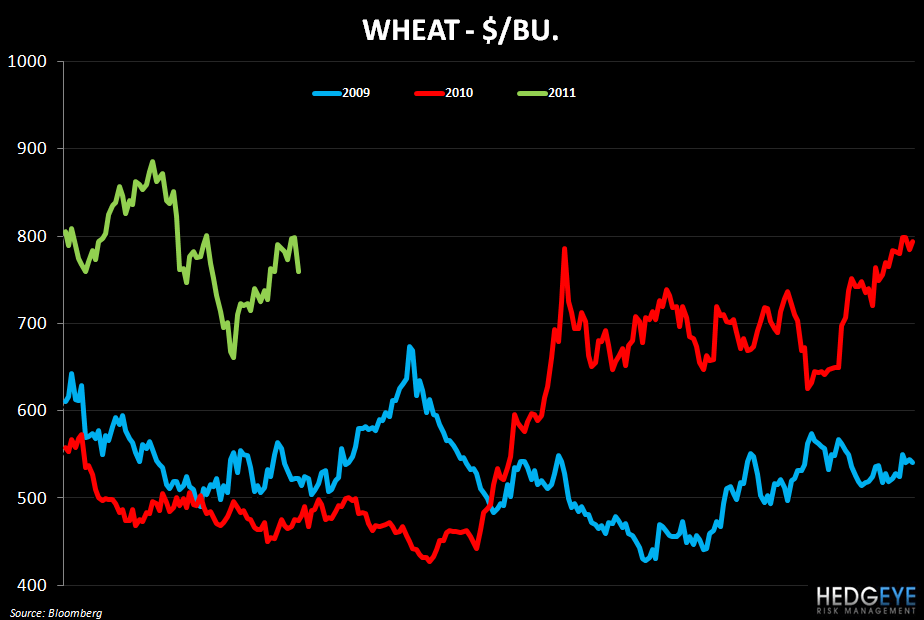

Wheat prices declined sharply last week as other grains, such as corn and rice, also saw downward price action. Media reports today suggest that wheat futures tumbled today as a result of speculation that demand will decline for U.S. commodities as the nuclear crisis seems to escalate in Japan. Some commentators see this decline as incongruous with the underlying dynamics of the wheat market, given the poor crop conditions currently in the U.S., but if a fall-off in demand were to occur, it could provide relief for PNRA. The company expects wheat costs for 2011 to be roughly flat versus 2010, as the company currently has nearly 75% of its wheat costs locked in for 2011, modestly below the 2010 price.

Howard Penney

Managing Director