Initial Claims Fall 6k (10k net of revision)

The headline initial claims number fell 6k WoW to 382k (10k after a 4k upward revision to last week’s data). Rolling claims fell 6k to 389k. On a non-seasonally-adjusted basis, reported claims fell 4k WoW.

We have been looking for claims in the 375-400k range as the level that can begin to bring unemployment down. If this level is held, we expect to see unemployment improve. We consider unemployment to be ~200 bps higher than the headline rate due to decreases in the labor force participation rate. In other words, if the labor force participation rate were at the long-term average level of the last decade, unemployment rate would be 10.8% rather than 8.8%. So when we say that claims of 375-400k will start to bring down the unemployment rate, we are actually referring to the 10.8% actual rate.

Our healthcare team has done substantial work on unemployment by age, and we include one of their charts below. The bottom line is that most of the improvement in unemployment has gone to the 55-64 year old demographic and the 20-34 demographic, while the middle aged demographic has yet to see employment growth.

One of our astute clients pointed out the relationship between the S&P and initial claims shown below. We show the two series in the following chart, with initial claims inverted on the left axis.

Yield Curve Widens Slightly

We chart the 2-10 spread as a proxy for NIM. Thus far the spread in 1Q is tracking 35 bps wider than 4Q. The current level of 271 bps is slightly wider than last week (266 bps).

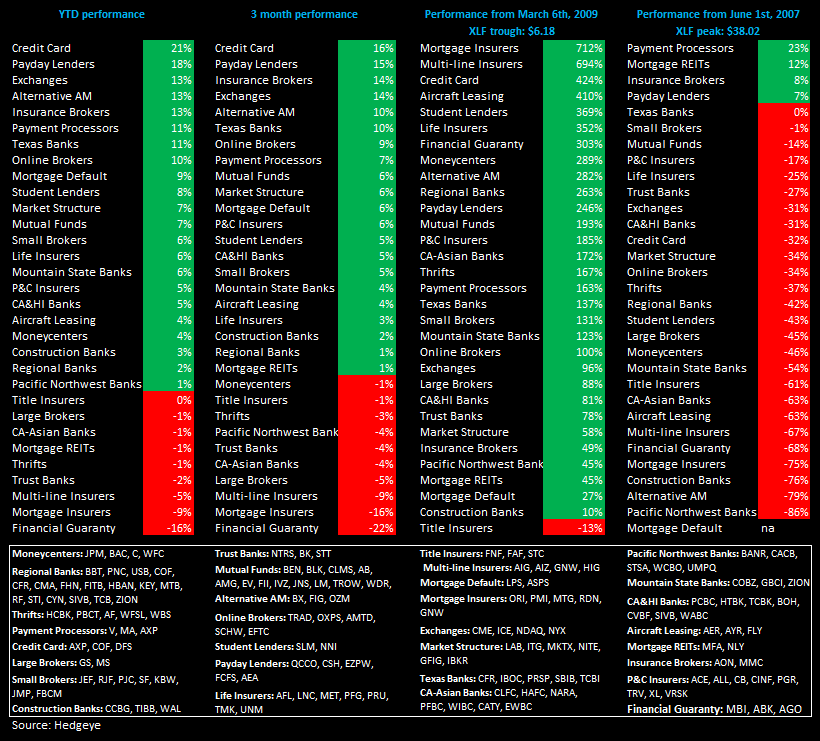

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations. We have adjusted our durations to show a different snapshot than we were previously.

Joshua Steiner, CFA

Allison Kaptur