Notable news items and price action from the past twenty-four hours.

- RT reported a disastrous quarter AMC. The stock traded down on accelerating volume during yesterday’s session is trading at $11.80 pre-market from yesterday’s close of $13.37. See my note, published earlier this morning, for more details. Most of the issues are RT specific but the group could trade lower today. I like EAT on any RT-related weakness.

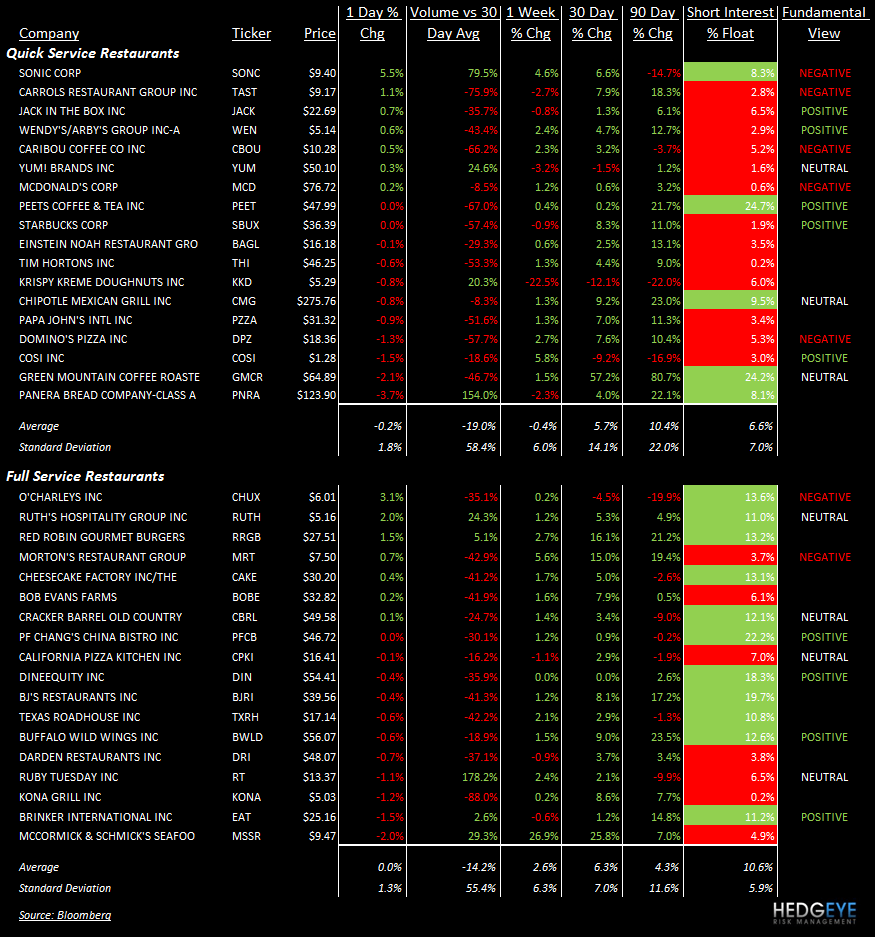

- PNRA declined 3.7% on accelerating volume. OTR Global has a “Mixed” read on Panera Bread, deteriorating from “Positive” in December.

- Japanese restaurants in India scrambled Wednesday to find replacement ingredients after the government imposed a blanket ban on food imports from Japan over radiation fears.

- From this month KFC will use high oleic rapeseed oil at its 800 outlets in UK and Ireland, at an estimated cost of £1m a year. The move will cut levels of saturated fat in its chicken by 25 per cent, according to the company.

- RUTH traded up nicely yesterday on accelerating volume – Hedgeye remains positive.

- YUM traded higher on accelerating volume.

Howard Penney

Managing Director