THE HEDGEYE DAILY OUTLOOK

TODAY’S S&P 500 SET-UP - April 6, 2011

The US Government Shutdown has overtaken Japan and the Middle East as #1 headline news what does it mean for market pricing?

- Dollar DOWN = stoking inflation to new cycle and YTD highs (CRB and Oil both this morning)

- Euro UP = new highs, smoking all patriotic pig name callers in the US out of their holes – reminding Americans our fiscal issues are worse

- Short Term Treasuries UP = ripping higher with both government shutdown default premiums rising (debt ceiling) and inflation being perpetuated

As we look at today’s set up for the S&P 500, the range is 19 points or -0.80% downside to 1322 and 0.63% upside to 1341.

SECTOR AND GLOBAL PERFORMANCE

We are on day 3 of perfect with 9 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 325 (+70)

- VOLUME: NYSE 830.64 (+7.78%)

- VIX: 17.25 -0.86% YTD PERFORMANCE: -2.82%

- SPX PUT/CALL RATIO: 1.69 from 2.15 (-21.10%)

CREDIT/ECONOMIC MARKET LOOK:

Treasury 10-year yields approached 4-week high, extending jump of 6 bps yesterday after release of Fed’s March 15 minutes

- TED SPREAD: 22.78

- 3-MONTH T-BILL YIELD: 0.07% +0.01%

- 10-Year: 3.50 from 3.45

- YIELD CURVE: 2.66 from 2.68

MACRO DATA POINTS:

- 7 a.m.: Fed’s Lockhart to meet with media at Stone Mountain, Ga.

- 7 a.m.: MBA Mortgage Applications

- 10:30 a.m.: DoE inventories

WHAT TO WATCH:

- Alberta government proposes rules that would revoke some oil sands leases - Globe and Mail

- Bullish sentiment increases to 57.3% from 51.6% in the latest US Investor's Intelligence poll

- FOMC Minutes indicate that the Fed felt it was important to pay attention to the evolution of inflation expectations

- NYSE Euronext reportedly may bid for Nasdaq to disrupt hostile counteroffer for NYX from Nasdaq, ICE

- Taiwan Semiconductor Manufacturing cuts forecast for 2011 global chip industry sales excluding memory products to 4% growth from prev. forecast 7% growth; says Japan earthquake hurt expected demand.

- Portugal plans to sell up to EU1b in bills due October.

COMMODITY/GROWTH EXPECTATION

COMMODITY HEADLINES FROM BLOOMBERG:

- Wheat Seen Extending Rally as Corn Surge Spurs Swap in Feed for Livestock

- Gold Climbs to Record in ‘Flight to Safety’ as Silver Reaches 31-Year Peak

- Wheat Crop Conditions in China Seen Improving, Curbing Import Requirements

- Fishing Halted in Japan’s Ibaraki Prefecture as Nuclear Plant Taints Sea

- Copper Reaches One-Week High on Speculation Demand Will Maintain Its Pace

- Crude Oil Trades Near 30-Month High Before ECB Meeting, U.S. Supply Report

- Cocoa Advances on Ivory Coast Export Speculation; Coffee Prices Decline

- Corn Declines as Investors Lock-in Gains After Four-Day Rally; Wheat Gains

- Citigroup Boosts Commodity Investment Team to Tap Demand as Prices Surge

- China, India Consumers to Lead Surge in Global Dairy Demand, Fonterra Says

- Palm Oil Gains as Widening Soybean Oil Margin, Crude Advance Boost Demand

- Rubber in Tokyo Little Changed as China Rate Hike Offsets Thai Flooding

- Ivernia Says No Timetable Set to Restart Lead Mine in Western Australia

CURRENCIES

- Canadian Dollar Strengthens to Highest Since November 2007

- Yen weakened to 6-month low against dollar, tumbled against euro amid speculation BoJ will trail Fed, ECB in ending stimulus

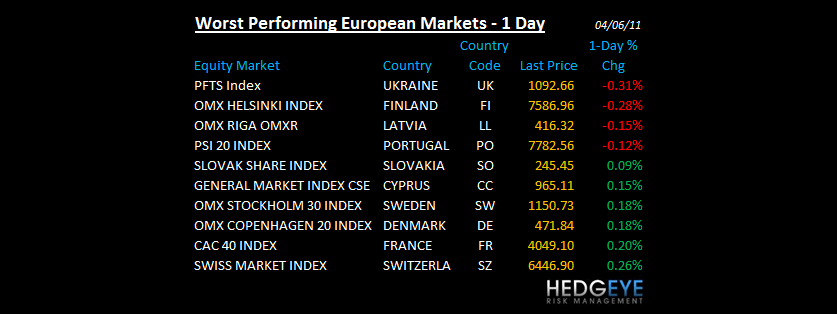

EUROPEAN MARKETS

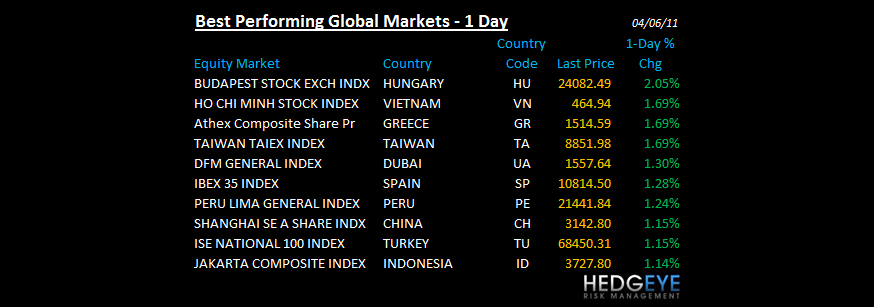

- Eastern European markets trade higher lower with the periphery again in focus and particularly Ireland and Portugal; Hungry and Turkey are the two best performing markets globally.

- Honda to Cut UK Output by 50%, Cites Japanese Parts Shortage

- UK Halifax Mar House Price Index +0.1% m/m vs consensus +0.2%

- Germany Mar construction PMI 61.8 vs prior 60.7

- UK Feb Industrial Production +2.4% y/y vs consensus +4.3%, prior revised +4.2% from +4.4%; UK Manufacturing Production +4.9% y/y vs consensus +5.8%, prior revised +6.6% from +6.8%

- German Feb. Factory Orders Rise 5x More Than Expected - Germany Feb industrial orders +2.4% m/m vs consensus +0.6% and prior revised +3.1% vs from +2.9%

- EuroZone Q4 GDP final +2.0% y/y vs preliminary +2.0%

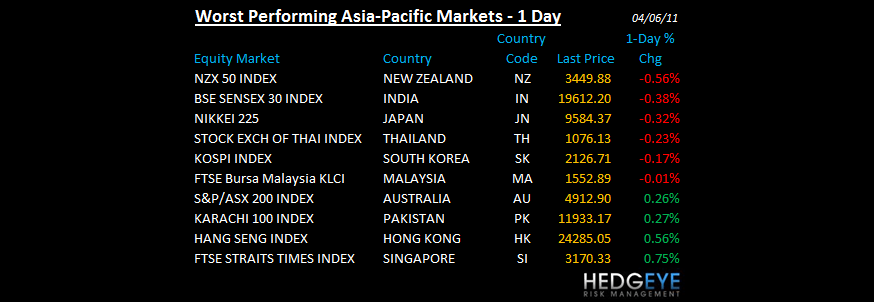

ASIA PACIFIC MARKTES:

The Asian markets turned in a positive performance except India, Thailand and South Korea. Thailand was closed for King Rama I Memorial and Chakri Day. China rose 1.14% despite yesterday’s surprise interest-rate increase and speculation that March inflation will be higher than expected.

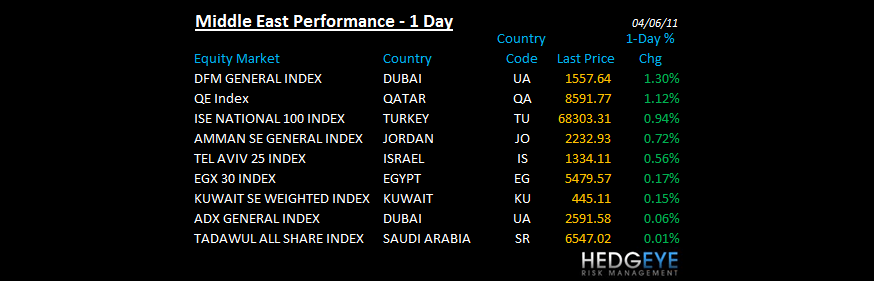

MIDDLE EAST

Howard Penney

Managing Director