This note was originally published March 29, 2011 at 07:59 in

“Most of those in political office, quite understandably, are firmly against inflation and firmly in favor of policies producing it.”

-Warren Buffett, May 1977

I’ve studied Warren Buffett very closely since I came to America in the mid 90’s. I wrote my Senior Thesis about him while I was an undergrad at Yale. I’ve applied many of his value-investing strategies to both the long and short side of my portfolios for the last 12 years.

Sadly, Buffett’s Politics have compromised the integrity of some of his post 2008 investment opinions. His 2010 testimony on Moody’s reminded me that if there is a transparent and accountable investment God on this good earth, it’s not him. That said, if I were in his shoes, I’d probably game these government people for my own benefit too.

If you didn’t know that Buffett’s Politics largely focus on pushing his own book, now you know. His #1 priority has been, and always will be, generating returns for the shareholders of Berkshire Hathaway. If you think this jolly looking fella has you in mind when he sits down with The President of the United States, think again…

If you go back and study the late 1970s Buffett, you’ll find a man who didn’t need the market to succeed in order for his overall invested position to. In fact, I think if you go back and read the article that we snagged the aforementioned quote from (“How Inflation Swindles The Equity Investor” – Fortune Magazine, 1977) and change the date on it to 2011, you might think it was something Hedgeye’s Howard Penney wrote last night.

Ah the 1970s…

Those were the days when Growth Was Slowing As Inflation Accelerated. Those were the days when the US Government’s heavy hand of Big Intervention tried everything from the Fed monetizing America’s debt to both Nixon and Carter signing off on a debauchery of the US Dollar. Those were the days of the 1970s – days when plenty of buy-the-dip folks went away.

My defense partner (and Columbia Business School Value Investing Program graduate) Daryl Jones, wrote an outstanding research note intraday yesterday questioning the premise of buying-the-dip on “valuation” (email sales@hedgeye.com if you’d like a copy). Without rehashing the note in full, the conclusion was based on my old Yale professor’s (Robert Shiller) CAPE P/E multiple whereby the US stock market looks at least one standard deviation overvalued.

We’ve been saying this since the start of the year, but it’s worth repeating. With corporate margins at 30-year highs, it’s unlikely that earnings will grow into their multiple. And while this wasn’t the topic of Buffett’s 1977 article on The Inflation, he’d be the first to remind you that you don’t buy a cyclical (the SP500) on peak earnings and peak margins of a cycle (you buy it before the cycle turns, like we did with the SP500 in March of 2009).

Back to what The Warren Buffett really thinks about The Bernank’s Inflation…

1979 Shareholder Letter:

“Our book value at the end of 1964 would have bought about one-half ounce of gold and, fifteen years later, after we have plowed back all earnings along with much blood, sweat and tears, the book value produced will buy about the same half ounce.”

“The rub has been that government has been exceptionally able in printing money and creating promises, but is unable to print gold or create oil.”

“… but you should understand that external conditions affecting the stability of the currency may very well be the most important factor in determining whether there are any real rewards from your investment in Berkshire Hathaway.”

1980 Shareholder Letter:

“High rates of inflation create a tax on capital that makes much corporate investment unwise.”

“The average tax paying investor is now running up a down escalator whose pace has accelerated…”

“As we said last year, Berkshire has no corporate solution to the problem. We’ll say it again next year, too. Inflation does not improve our return on equity.”

Back to the morning Global Macro Grind…

No matter where you go this morning, there is no “stability of the currency” in this country. The US Dollar is already down again for the week-to-date. There’s only The Bernank and The Inflation. Sure we can turn on the TV and watch the latest disciple of the Keynesian Kingdom cheer on the last leg of The Policy to inflate. But we don’t have to support them. We should fight them – out loud - and hold them accountable… before it’s too late.

Inflation is sticky. So … as Growth Slows, you end up with The Stagflation. This morning, you can see slower global economic growth being priced into many asset classes, across durations:

- Asian Growth Slowing – Thailand reported an industrial production growth number last night of -3.4% (year-over-year) for the month of February versus a +4.1% growth report in January. While growth slowing on the East Side of this world isn’t new news (we’ve been calling for it since November), it’s scary to think that the slowdowns were this sharp BEFORE Japan’s quake.

- European Growth Slowing – Germany, which has been our favorite Western Economy for the last 2 years, is starting to show the first signs of high-frequency growth data slowing in March. This is not good. Neither is all of the Pig Paper countries falling down on the sword of GDP “growth” promises for 2011 (Portugal revised expectations to negative y/y GDP growth last week).

- Dr. Copper Slowing – Copper prices are getting pounded again early this week, trading down -2.3% so far for the week-to-date. Critically, the price of copper is now broken on 2 of our 3 core risk management durations @Hedgeye with TREND line resistance now at $4.36/lb.

Now, quickly, the US-centric stock market bull should be yelling at me – “buy-the-damn-dip.” At least until month and quarter end on Thursday… (that’s when most of us get paid). But that’s not going to stop gravity. If you want to do that – and I mean stop The Inflation before you stop The Stagflation – you’ll need to have your local Central Planner in Washington re-read Buffett circa 1977.

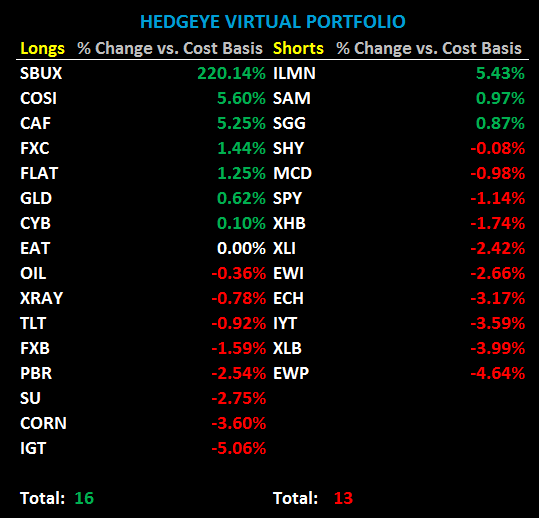

My immediate-term TRADE lines of support and resistance for WTI Crude Oil are $100.34 and $107.94, respectively (we are long oil). My immediate-term TRADE lines of support and resistance for the SP500 are 1292 and 1323, respectively (we are short the SP500).

God bless America and a Strong US Dollar.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer