TODAY’S S&P 500 SET-UP - March 24, 2011

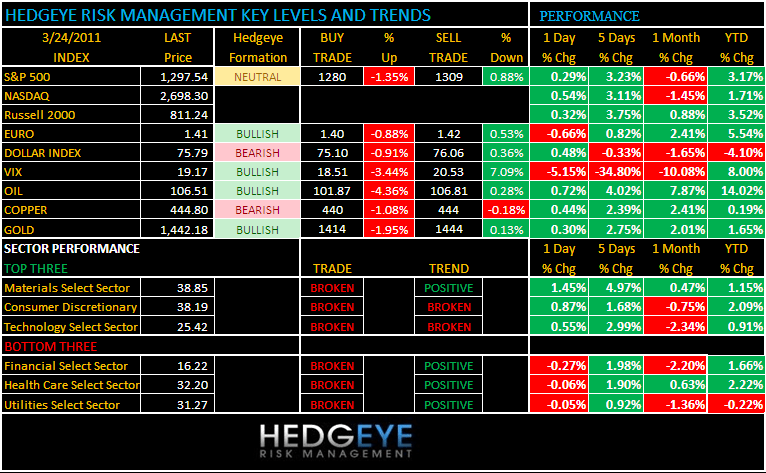

Now that we’ve traversed the daily double-dose of Middle East/Japan open-the-envelope-risk, it could very well be back to the “fundamental” grind. Germany, which is a country we’ve fundamentally liked for the last two years, reported a sequential slowdown in its MAR Manufacturing PMI this morning at 60.9 vs 62.7 in FEB. The evidence continues to support the theme of Global Growth Slowing; the USA looks to continue to put risk on the back burner. As we look at today’s set up for the S&P 500, the range is 29 points or -1.35% downside to 1280 and 0.88% upside to 1309.

PERFORMANCE:

As of the close yesterday we have 2 of 9 sectors positive on TRADE and 8 of 9 sectors positive on TREND.

- One day: Dow +0.56%, S&P +0.29%, Nasdaq +0.54%, Russell 2000 +0.32%

- Month-to-date: Month-to-date: Dow (1.15%), S&P (2.24%), Nasdaq (3.02%), Russell (1.48%)

- Quarter/Year-to-date: Dow +4.39%, S&P +3.17%, Nasdaq +1.71%, Russell +3.52%

- Sector Performance: - Materials +1.45%, Consumer Disc +0.87%, Tech +0.55%, Industrials +0.34%, Consumer Spls +0.17%, Energy +0.26%, Utilities (0.05%), Healthcare (0.06%), Financials (0.27%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 303 (+761)

- VOLUME: NYSE 878.55 (+6.64%)

- VIX: 19.17 -5.15% YTD PERFORMANCE: +8.00%

- SPX PUT/CALL RATIO: 1.40 from 1.98 (-29.39%)

CREDIT/ECONOMIC MARKET LOOK:

Currently, treasuries yields were the highest in more than a week.

- TED SPREAD: 22.69 +0.304 (1.360%)

- 3-MONTH T-BILL YIELD: 0.09% -0.01%

- 10-Year: 3.36 from 3.34

- YIELD CURVE: 2.66 from 2.67

MACRO DATA POINTS:

- 8:30 a.m.: Durable Goods orders, est. 1.2%, prior 2.7%

- 8:30 a.m.: Net export sales (cotton, corn, soybeans, soymeal)

- 8:30 a.m.: Initial jobless claims, est. 383k, prior 385k

- 9:45 a.m.: Bloomberg Consumer Comfort, est. (-48.5), prior (-48.5)

- 10 a.m.: Freddie Mac 30-year mortgage

- 10:30 a.m.: EIA natural gas, est. (-8)

- 1 p.m.: U.S. to sell $11b 10-yr TIPS reopening

- 7:30 a.m.: Fed’s Duke speaks to economist in Virginia

WHAT TO WATCH:

- Bullish sentiment among individual investors bounced back to 37.8% this week in American Assoc. of Individual Investors survey, reversing last week’s results where bears outnumbered bulls for the first time in 6 months.

- Portuguese PM resigns

- Moody’s cuts ratings on Spanish banks after sovereign downgrade

- U.S. aims to shift Libya command to NATO

- Top U.S. Republicans question purpose of Libya military intervention

COMMODITY/GROWTH EXPECTATION:

- CRB: 357.03 +0.15% YTD: +7.28%

- Oil: 105.75 +0.74%; YTD: +14.06% (trading +0.59% in the AM)

- COPPER: 442.85 +2.68%; YTD: +0.18% (trading +0.35% in the AM)

- GOLD: 1,437.80 +0.80%; YTD: +1.65% (trading +0.27% in the AM)

COMMODITY HEADLINES FROM BLOOMBERG:

- Worst Texas Drought in 44 Years Damaging Wheat Crop, Reducing Cattle Herds

- Commodities to Resume Rally to 2008 High After Temblor: Technical Analysis

- Crude Oil Rises a Fourth Day After Allied Forces Intensify Libya Attacks

- Gold Trades Near Record on Europe Debt Risk; Silver Reaches 31-Year Peak

- Wheat Falls as Higher Prices May Encourage Farmers to Increase Planting

- Coffee Slides to One-Week Low as Drought May Ease in Vietnam; Cocoa Falls

- Copper May Rise for a Third Day as Orders to Draw Metal From Stocks Surge

- India May Keep Rice, Wheat Export Curbs Even on Normal Monsoon, Adani Says

- Curbs on Food Imports From Japan Widen Amid Nuclear Contamination Concern

- Copper-Treatment Fees Jump in China as Quake Hurts Japan's Smelter Output

- France Shipped 3 Million Tons of Wheat to Algeria, According to Exporter

- Rice Stockpiling Program in Vietnam Is 45% Complete, Industry Group Says

- Natural Gas's Three-Year Drop Ending on Japan's LNG Demand: Energy Markets

- Rubber Futures Gain on Tight Supply From Key Producers, Crude Oil Advance

CURRENCIES:

- EURO: 1.4124 -0.66% (trading -0.03%% in the AM)

- DOLLAR: 75.794 +0.48% (trading -0.01% in the AM)

EUROPEAN MARKETS:

Generally, European markets are trading higher despite concerns over Portugal and a Moody’s downgrade of Spanish banks.

EuroZone Mar flash Manufacturing PMI 57.7 vs consensus 58.4 and prior 59.0

Germany Mar preliminary Manufacturing PMI 60.9 vs consensus 62 and prior 62.7

UK Feb Retail sales +1.3% y/y vs consensus +2.3% and prior revised to +5.1% from +5.3%

- United Kingdom: +0.88%

- Germany: +1.10%

- France: +0.60%

- Spain: +0.13%

- Greece +1.54%

- Italy: +0.49%

ASIAN MARKTES:

Most Asian market traded higher, with the exception of Vietnam and China down -1.35% and -0.06%, respectively.

- Japan: -0.15%

- Hang Seng: +0.39%

- Australia +1.01%

- China: -0.06%

- India: +0.79%

- Taiwan: +0.37%

- South Korea +1.22%

Howard Penney

Managing Director