When 2022 becomes 2023 (PRGO)

Perrigo reported Q3 EPS of $.56 vs. consensus of $.67. The shortfall was due to a deceleration in the CSCA segment. Organic sales growth was 8% and constant currency sales growth was 12.3% with the contribution from HRA.

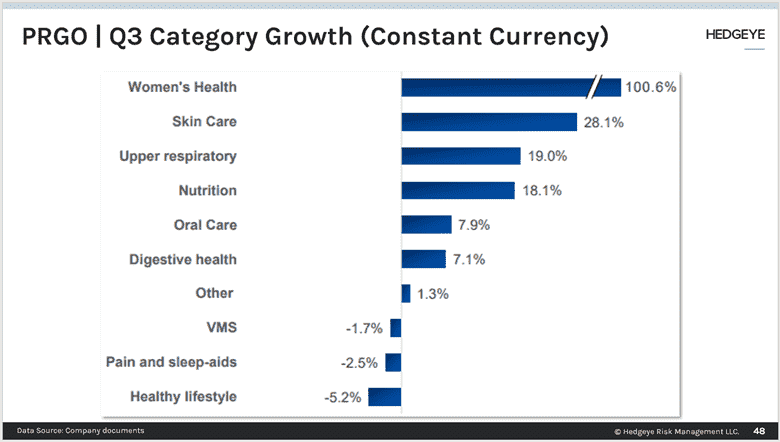

CSCA constant currency sales growth was 4.0% with organic sales growth of 7.3%. HRA added 3.3% to the reported sales growth. Within the CSCA segment, the Nutrition category grew by 18.1% due to increased demand for infant formula. The Upper Respiratory category grew 8.4% despite a 4.8% headwind from the divestment of the Latin American business. Three categories grew below the segment average, Pain & Sleep Aids which was negatively impacted by a divestment, Healthy Lifestyle which was negatively impacted by the discontinuation of diabetes products, and Skin Care which was negatively impacted by divestment and product discontinuation. The segment’s gross margins expanded by 40bps while operating margins contracted by 80bps.

CSCI constant currency sales growth was 28.6%, driven by the HRA acquisition. Fx offset the contribution of HRA as organic sales growth of 8.3% was similar to the reported sales growth of 8.4%. In 2023, management anticipates a €30M one-time expense for sales returns from distributors that will be included in non-GAAP results. The synergy target for HRA was increased to €50M by the end of 2024 which will also necessitate €30M of fixed cost infrastructure that will not be included in non-GAAP results. The segment’s gross margins expanded by 480bps while operating margins expanded by 390bps.

Perrigo is gaining share in the OTC category, +0.3% points in the U.S. and +1.9% in Europe, but less than investors’ expectations in the inflationary environment. While dollar share gains are more difficult when branded prices are increasing more, inventory levels are also holding back gains. The total U.S. OTC market decelerated from -13.4% in the 1H to +2.3% in Q3. In the U.S., Perrigo sell-through at retail decelerated from +9.1% in the 1H to +5.8% in Q3 while shipments decelerated from +15.3% in the 1H to +4.0% in Q3. Management attributed the deceleration to lower inventory levels, a weaker allergy season, and normalizing trends.

Margins

Gross margins expanded 210bps, in constant currencies gross margins expanded 310bps. Gross margins benefited from pricing, higher sales volumes, lapping two product recalls, and the acquisition of HRA. EBIT margins expanded 140bps, in constant currencies EBIT margins expanded 190bps.

Guidance lowered

Management lowered EPS guidance to $2 - $2.10 from $2.25-2.35, $.10 was due to Fx, and $.15 was due to inflationary cost pressures, labor pressures, and distribution costs. Organic revenue guidance of 9-10% was reaffirmed as was reported revenue growth of 8.5-9.5%. At current levels, Fx is a 5-6% headwind.

The accretion from the recently announced acquisition of Nestle’s Gateway infant formula plant is now included in guidance - $50M of EBIT, $40M incremental in 2023. Perrigo will now produce all of its own needs, improving the unit’s margins and offsetting lower demand in 2023 from Abbott returning fully to the market.

Moving to 2023

Entering 2022 there were several YOY positives including accretion from the HRA acquisition, price increases catching up to cost increases, and a cough/cold season that would lap a weak one that was also negatively impacted by fully stocked shelves from the previous year. During 2022, the Euro became a significant headwind while Abbott’s infant formula plant closure became an offsetting tailwind.

The outlook for 2023 becomes brighter as 2022 encounters additional challenges. In 2023, decelerating and falling cost increases along with pricing strengthen the margin outlook.CEO Murray Kessler said guidance for 2023 would start at $3 in EPS minus $.28 for Fx ($.10) and one-time inventory takebacks from European distributors ($.18 or €30M). Management has been guilty of setting expectations too loosely, utilizing almost back-of-the-envelope math with investors for the past two years. Then management has stuck with those expectations when formalizing guidance despite changes in business fundamentals, Fx, tax rates, or interest rates. Management looks to have set the starting point for 2023 at $3, repeating the mistake. The company can certainly earn more than $3 (even excluding the approval of Opill), but when the shares are implying EPS between $2 to $2.40, only EPS power should be discussed with a $3 starting point.

Where we come out

Importantly, the environment has several tailwinds for the low-price consumer healthcare manufacturer. Perrigo is not “hoping” for a stronger consumer, more discretionary spending, a change in the competitive environment, or a stronger economy. The economic conditions are in place for Perrigo to achieve top-line growth above the long-term plan and to expand margins. Management still has to execute on raising prices, improving manufacturing throughput, and competing. Yesterday's sell-off represents a favorable risk/reward for shares into 2023.