Positions in Europe: Short Italy (EWI); Short Spain (EWP)

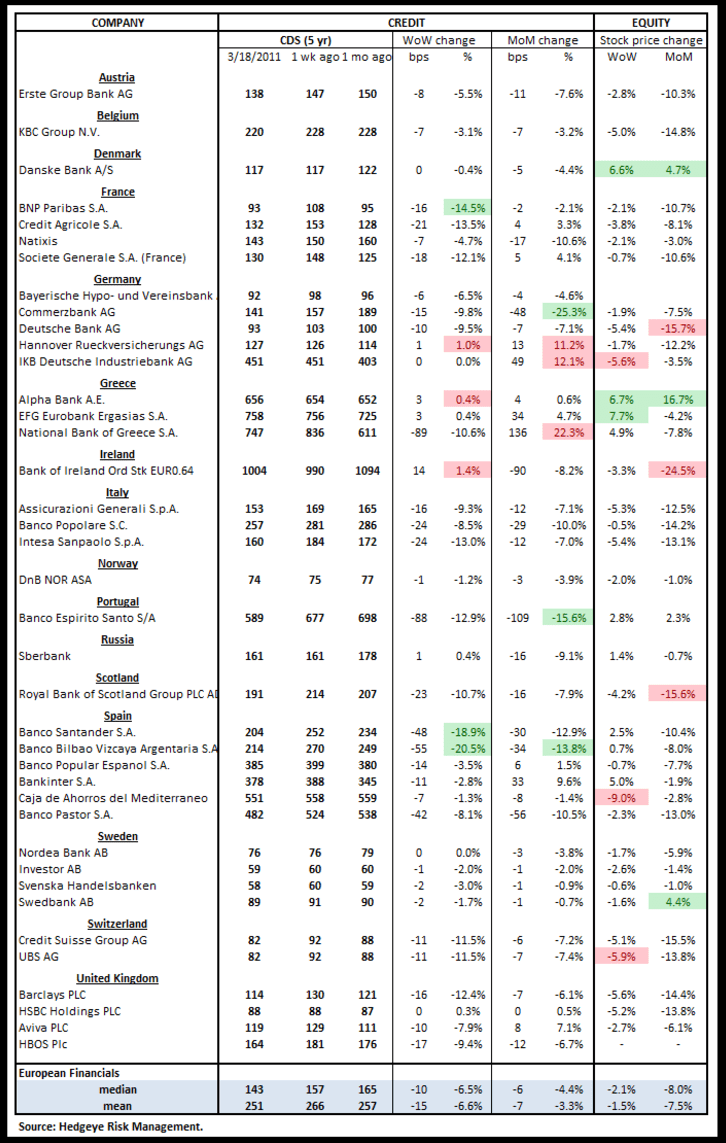

Below we include our weekly Risk Monitor for European bank CDS. Banks swaps in Europe were mostly tighter week-over-week, tightening for 32 of the 39 reference entities and widening for 7.

European capital markets continue to be volatile given existing global concerns (in particular the results of the earthquake and tsunami in Japan and unrest in MENA) and domestic issues (existing sovereign debt imbalances across states; indecision from the BoE and ECB on adjusting monetary policy to reflect inflation pressures; the second round of Bank Stress Tests; and the likely consummation of dovish agreements at the comprehensive EU Summit this week (March 24-25) – in short, a larger and more generous social net to bailout/protect ailing member states).

To the last point, European equity markets could likely trade with a positive bias anticipating that the EU Summit will calm near-term bailout/default fears. In particular we’ve highlighted Portugal as one country on watch as it goes up against a hefty schedule of bonds coming due over the next 4 months (see our portal: Portugal Shakes on Debt Dues on 3/16).

In the Hedgeye Virtual Portfolio we’re short Italy via the etf EWI and Spain via EWP. Our position remains that despite initial attempts at austerity, these two countries should break longer term under their bloated sovereign debt and deficit imbalances. In both cases, we tactically shorted the etfs on a bounce last week. We view the EUR-USD currently overbought, with immediate term TRADE levels of $1.39 - $1.41.

Matthew Hedrick

Analyst