R3: REQUIRED RETAIL READING

March 15, 2011

RESEARCH ANECDOTES

- According to the Japanese Tourism Marketing Company, more than one-third of all Japanese tourist that visit the U.S. annually do so via Hawaii. While few retailers are ‘over-indexed’ to Ala Moana, the contribution from one of the more productive U.S. malls will certainly have to be tempered near-term.

- Add online retailer Shopbop to the list of recent entrants into the bridal category behind the likes of Urban Outfitters, Net-a-Porter and The Aisle New York. With dresses ranging from $200 to $2,500, the e-tailer is selling at a similar level to Costco’s latest bridal collaboration at $700-$1,400 with the primary difference the inability to actually try the dress on first.

- According to the latest Millward Brown “Value-D” study which ranks global brands on how consumers perceive value vs. the associated costs, Amazon.com ranks number one. Amazon is the only retailer to rank in the top ten on the global list, while Wal-Mart shows up at number six on the US list.

OUR TAKE ON OVERNIGHT NEWS

JJB Sports Unveils Recovery Strategy - The 250-store chain also confirmed it would seek a further £65m from shareholders to fund the restructuring. JJB, which had been in merger talks with rival JD Sports, said the new-look operation would be based around the success of six trial stores.These stores were refocused to appeal to keen amateurs and sporting families. Sales at these stores have been running at about 16% above the company average, JJB said in a statement. The company also said that it had reached agreement in principle with its major shareholders - Harris Associates, Crystal Amber, Invesco Asset Management and the Bill & Melinda Gates Foundation Trust - to support a £65m fundraising. <BBC>

Hedgeye Retail’s Take: Very rarely, if ever, does a new prototype save the day for a retailer that has been under pressure for at least the past five years. We’d be surprised to see this turnaround succeed based on a complete transformation of the store format.

Gucci With Al Tayer Insignia - As part of a strategy to directly control its stores, Gucci said Monday it has signed a memorandum of understanding to form a joint venture with luxury retailer Al Tayer Insignia. The agreement, which is expected to be finalized over the next few months, will allow Gucci to directly enter the United Arab Emirates. Gucci declined to provide details of the partnership, but said the joint venture will be headquartered in Dubai. Al Tayer has been Gucci’s franchisee in the region for more than a decade. The luxury brand currently counts six points of sale in the UAE. One store is located in Abu Dhabi, at Marina Mall, and three boutiques are at the Mall of the Emirates, at The Boulevard at Jumeirah Emirates Towers and at The Dubai Mall in Dubai. Gucci is also present at Dubai’s Harvey Nichols and Bloomingdale’s with corners in the two department stores. <WWD>

Hedgeye Retail’s Take: Not surprisingly, luxury brands continue to chip away at the small but growing opportunities in the Middle East. We wonder if at some point recent political unrest puts a damper on near term growth plans given the costs associated with opening boutiques in the region.

Jack Rogers Opens in Manhattan - For six decades, the Navajo sandal has been the mark of Jack Rogers footwear. Now a casual chic collection inspired by the singular look is emerging, and the progress is most visible on Madison Avenue here between 87th and 88th Streets, where the first Jack Rogers store gets christened with a party tonight. “We want to become a lifestyle brand,” said William Smith, chairman of Jack Rogers and managing partner of Global Reach Capital, during a visit to the 1,240-square-foot space. The classic sandal has been interpreted into a full line of footwear with more than 100 stockkeeping units, including closed-toe shoes, ballet flats, moccasins, high-wedged espadrilles, pumps, heels, shoes with Swarovski Elements micro beads, with monograms, in glazed suede or distressed leather, and even a rain boot for fall with a side zipper. <WWD>

Hedgeye Retail’s Take: A niche product for sure, but one that has a very loyal customer base. We wonder how successful the iconic sandal company will be with its efforts moving into more traditional closed toe footwear. Clearly a little private equity infusion is helping to push the brand beyond its 60 year sandal history.

Uptick in M&A activity - The thrift that companies exercised during the recession by building up their balance sheets is coming back to haunt them in the form of pressure to buy, and it’s lifting the mergers-and-acquisitions market to levels that could approach historic highs. Global M&A activity bounced back in 2010, rising 22.7 percent to $2.09 trillion over 2009 as U.S. M&A rose a less robust 2.8 percent to $714.3 billion, according to The Mergermarket Group. Still, both volume figures were well below the levels of 2008, when global activity hit $2.5 trillion despite a near freeze in fourth-quarter activity following the year’s financial crisis, and the progressively higher levels of M&A from 2005 to 2007. <WWD>

Hedgeye Retail’s Take: Nothing like a banker bonanza as we head into more uncertain times from a macro perspective. From a retail standpoint, we note that there are still numerous rumored deals that remain on the table.

Earthquake Hits Luxury Companies - The stars have aligned for the luxury industry since the global recovery began. But the earthquake in Japan is a reminder of how quickly tragedy can change the industry's prospects. Japanese investors dumped stocks Monday in response to Friday's earthquake, with the Nikkei 225 tumbling 6%. While the U.S. stock market fell just a fraction of that amount, luxury highfliers came under fire. Tiffany, which trades at 18 times this year's consensus earnings, fell 5%. Coach and Burberry Group of the U.K. fell by similar amounts. Luxury investors have learned to pay less attention to Japan in recent years. Once vital, Japan accounted for 19% of Tiffany's sales in 2009, compared with 28% in 2000. <WallstreetJournal>

Hedgeye Retail’s Take: It’s likely that beyond the physical recovery, the psychology of luxury buying will take even longer to rebound.

Smartphone Owners like to Scan and Save - Smartphone owners are realizing the power of the mobile app to both gather information about products and services and save, a new poll from Chadwick Martin Bailey and iModerate Research Technologies finds. A poll of 1,491 U.S. adults finds of those who have used a smartphone app or mobile browser while shopping, 44% have used a bar code scanning app such as RedLaser or ShopSavvy that lets them compare prices and learn more about products and services in stores. 38% have used a discount or deal app such as those from Groupon or LivingSocial that offer deep discounts, typically on local goods. Location-based shopping apps such as foursquare and shopkick came in last among the shopping-related apps mobile shoppers employed, with 13% reporting using them. <InternetRetailer>

Hedgeye Retail’s Take: Not surprisingly, the democratization of retail pricing is being empowered by the smartphone and its ability to act as a personal bar code scanner. It will not be long before self checkout also occurs via the smartphone, thus eliminating the need to wait in lines.

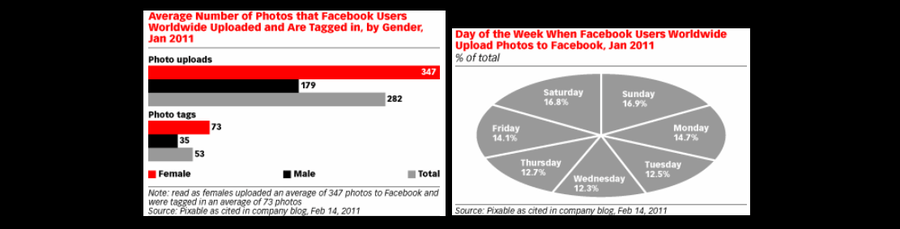

Photo-Sharing Trends Encourage Marketers - Consumers are increasingly sharing photos via social networks and mobile apps, and marketers are looking to capitalize on this trend. For most marketers, photo-sharing can help build brand awareness and encourage consumers to interact with the company. LIPTON Brisk iced tea partnered with mobile photo-sharing app Instagram for a campaign prior to the 2011 South By Southwest (SXSW) Conferences and Festivals. Fans were encouraged to take pictures through Instagram and tag them with #briskpic to be entered in a photo contest. The winning photos were included on a limited-edition can of the drink during SXSW. <eMarketer>

Hedgeye Retail’s Take: Product placement is certainly not a novel concept, but if LIPTON is any indication, brands’ ability to integrate with mobile/social networking far exceeds the adoption rate compared to sitcoms of the 90s.