“Demographics is destiny.”

-Arthur Kemp

Undoubtedly, there is a lot I disagree with Arthur Kemp on. He is the Foreign Affairs Spokesperson for the British National Party, and is a self-avowed white separatist and critic of miscegenation. Yup, definitely not that kind of cat I would spend much time socializing with or supporting. Despite this, his quote above regarding demographics rang very true with me.

We employ demographics across many of our research verticals, and in fact use it from a macro perspective when analyzing countries and demand patterns. The inevitability of demographic trends is difficult to deny. In some instances, it may merely be getting old, which is what my mother likes to tell me I’m doing as a 37-year old bachelor. In other situations, demographics, and the related outcomes, relate more to youth and birthrates.

In an intraday note yesterday titled, “Could the Kingdom Fall?”, I highlighted the importance of age to social unrest in the Middle East and North Africa. Simply put, MENA has a young population that is severely under-employed. If there is an elixir for social unrest, this is it - young people with too much time on their hands, and not enough money in their pockets.

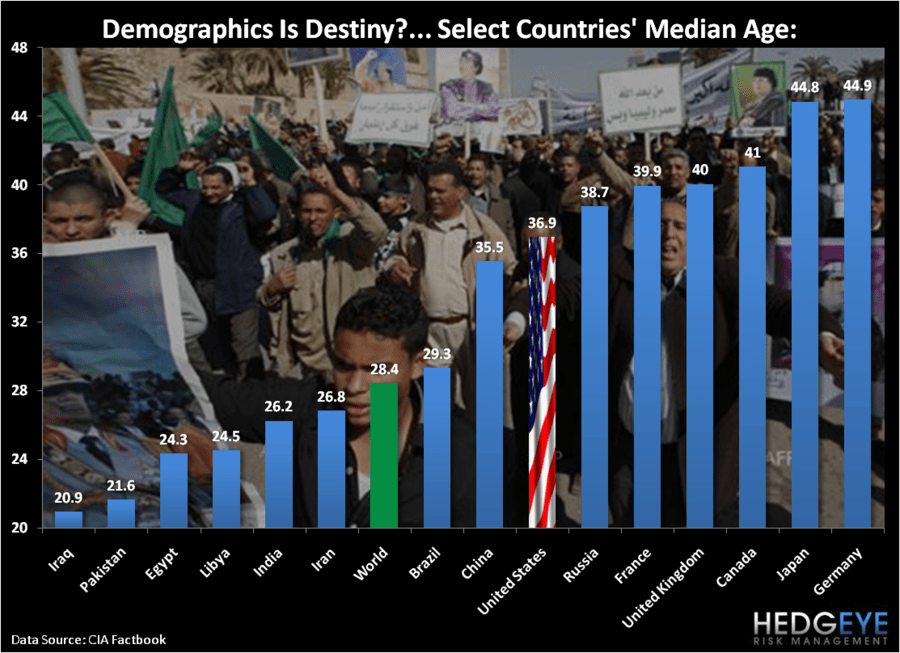

As a frame of reference, the median age in the United States is 36.9 years. Globally, the median age is 28.4 years. So, the population of the United States is meaningfully older than the rest of the world. The global median age is driven down by the Middle East and North Africa. In the Chart of the Day, we’ve highlighted this global discrepancy broadly, but the median age in Iran is 26.8, in Iraq 20.9, in Egypt 24.3, in Libya 24.5, and in Pakistan 21.6. The lower average and median ages in MENA have been driven by vastly improving health care over the last decade, which have driven up birthrates.

In Japan, the key demographic trend is the exact opposite. In contrast to many MENA countries, and really the world, Japan is old. Not getting old, but already there. In fact, the median age in Japan is 44.8 years. According to the CIA World Fact Book, this makes Japan the second oldest nation based on median age after Germany, whose median age is 44.9. Not surprisingly then, demographics is one the key tenets in our bearish thesis on Japan’s equity and currency; or as we like to call it: Japan’s Jugular.

While Japan’s median age is slightly lower than Germany’s, it has by far the world’s most elderly population. Currently, as of 2009, 22.7% of Japan’s population is above 65 years of age. The Japanese government has modeled this ratio to grow to 29.2% by 2020 and to 39.6% thirty years after that. The implications are that in ten years the ratio of retirees to working age will be ~48% in Japan.

The aging Japanese population has dire implications related to the future fiscal and monetary health of the country. The Japanese Government Pension Investment Fund, the world’s largest pension fund with ~$1.4 trillion in assets, has consistently been one of the largest buyers of Japanese government debt. This fiscal year, ending March 2011, the fund will be for the first time a net seller of Japanese government bonds. According to Takahiro Mitani, the President of GPIF, “We certainly have to come up with an adequate amount” to pay pensions. With these bond sales, the impact of demographic headwinds has likely reached an inflection point in the Japanese economy. These sales will only accelerate in the coming decades and with them the associated risks to the Japanese economy (higher interests rates as one) will also accelerate.

In the United States, there is some clear destiny embedded in demographic trends as well, specifically related to healthcare and healthcare investors. The Baby Boomer wave, which Healthcare investors commonly, and mistakenly, place as the core driver of a long-term Healthcare growth thesis, remains the most consequential domestic demographic trend.

Boomer Employment (45-64 yr olds) reached its crescendo in the 1 timeframe with peak earnings and peak disposable income occurring alongside historic lows in unemployment. Now, with this segment of the working population in deceleration mode, the U.S. workforce nearing a peak in average age, and the echo boomers (30-39 yr. olds) years away from peak consumption growth, the healthcare and broader economy face significant longer-term demographic headwinds.

This last point is also embedded in long-term projections for healthcare and social security entitlements in the United States. In the Congressional Budget Office’s long-term baseline scenario, due to these aging demographic trends, social security spending accelerates from 4.8% of GDP in 2010 to 6.2% in 2035 and healthcare spending accelerates from 5.5% of GDP to 9.7% over the same time period, which will lead to a huge ramp in mandatory government spending over the coming decades with no reform.

While there is inevitability embedded in many of the demographic trends outlined above, from a risk manager’s perspective we just have to manage the tail and headwinds accordingly. And as Chuck Jones, the inventor of Wile E. Coyote, said about inevitability:

“There is absolutely no inevitability as long as there is a willingness to think.”

Indeed.

Keep your head up and stick on the ice,

Daryl G. Jones