TODAY’S S&P 500 SET-UP – February 25, 2011

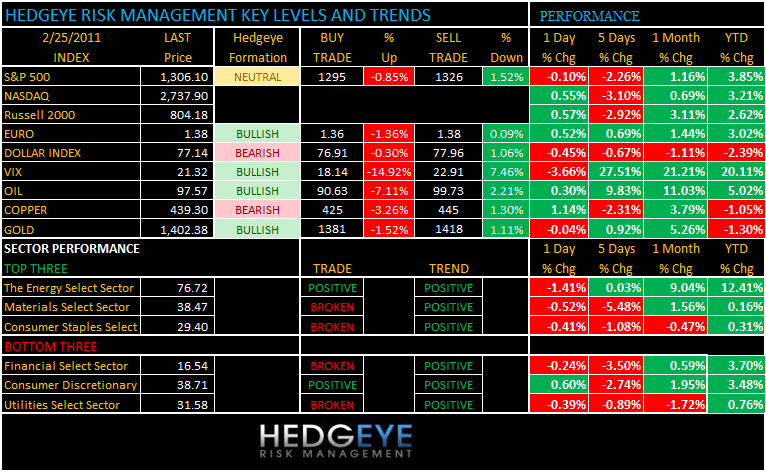

Oil was, once again, a key driver of equity prices yesterday. The rise in oil reversed yesterday intraday and equities, on cue, finished strongly into the close in New York. Speculation that the U.S. recovery will be further confirmed by data to be released today also helped stocks as the concerns surrounding oil prices abated. As we look at today’s set up for the S&P 500, the range is 31 points or -0.85% downside to 1306 and 1.52% upside to 1330.

MACRO DATA POINTS

- 08:30 a.m.: GDP QoQ, 4Q, Est. 3.3%, prior 3.2%

- 08:30 a.m.: Personal Consumption, 4Q, Est. 4.2%, prior 4.4%

- 08:30 a.m.: GDP Price Index, 4Q, Est. 0.3%, prior 0.3%

- 08:30 a.m.: Core PCE QoQ, 4Q, Est. 0.4%, prior 0.4%

- 09:55 a.m.: U. of Michigan Confidence, February (final), Est. 75.4, prior 75.1

PERFORMANCE:

Two of the nine S&P 500 sectors are positive from a TRADE perspective while all nine are positive from a TREND perspective.

- One day: Dow (0.31%), S&P (0.10%), Nasdaq +0.55%, Russell +0.57%

- Month-to-date: Dow +1.48%, S&P +1.55%, Nasdaq +1.40%, Russell +2.94%

- Quarter-to-date: Dow +4.24%, S&P +3.85%, Nasdaq +3.21%, Russell +2.62%

- Sector Performance - (6 sectors up and 3 down): - Consumer Discretionary +0.60%, Industrials +0.58%, Technology +0.35%, Healthcare +0.34%, Financials -0.24%, Utilities -0.39%, Consumer Staples -0.41%, Materials -0.52%, Energy -1.41%

EQUITY SENTIMENT

- ADVANCE/DECLINE LINE: +143 (+1052)

- VOLUME: 1221.30 (-8.20%)

- VIX: 21.32 (-3.62%)

- SPX PUT/CALL RATIO: 2.22 from 1.34 (+65.67%)

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 18.47 from 18.88

- 3-MONTH T-BILL YIELD: 0.13% from 0.12%

- 10-YEAR: 3.46% from 3.45%

COMMODITY/GROWTH EXPECTATIONS:

- CRB: 346.3 -0.63%; YTD: +3.90%

- Oil: 97.61 +0.34%; YTD: +5.84%

- Copper: 440.2 +1.35%; YTD: -0.84%

- Gold: 1404.72 +0.13%; YTD: -1.13%

CURRENCIES

- USD: 77.149 +0.12%

- Euro: 1.378 -0.07%

EUROPEAN MARKETS

- FTSE 100: +0.83%; DAX: +0.43%; CAC 40: +1.31%

- Russian Central Bank Unexpectedly Raises Main Rates, Reserve Requirements

- Lloyds Tumbles as Rising Funding Costs Threaten 2011 Profit

- Sentance Says BOE Must Tighten Now to Prevent Tough Moves Later

ASIAN MARKETS

- Nikkei +0.71%; Hang Seng +1.82%; Shanghai Composite +0.00%

- Asian Stocks Climb for First Time This Week on Oil Price; Hynix Advances

- India Says Economy May Grow as Much as 9.25% Next Year Amid Inflation Risk

- World’s Biggest Pension Fund ‘Will Likely’ Sell Japan Bonds

Howard Penney

Managing Director