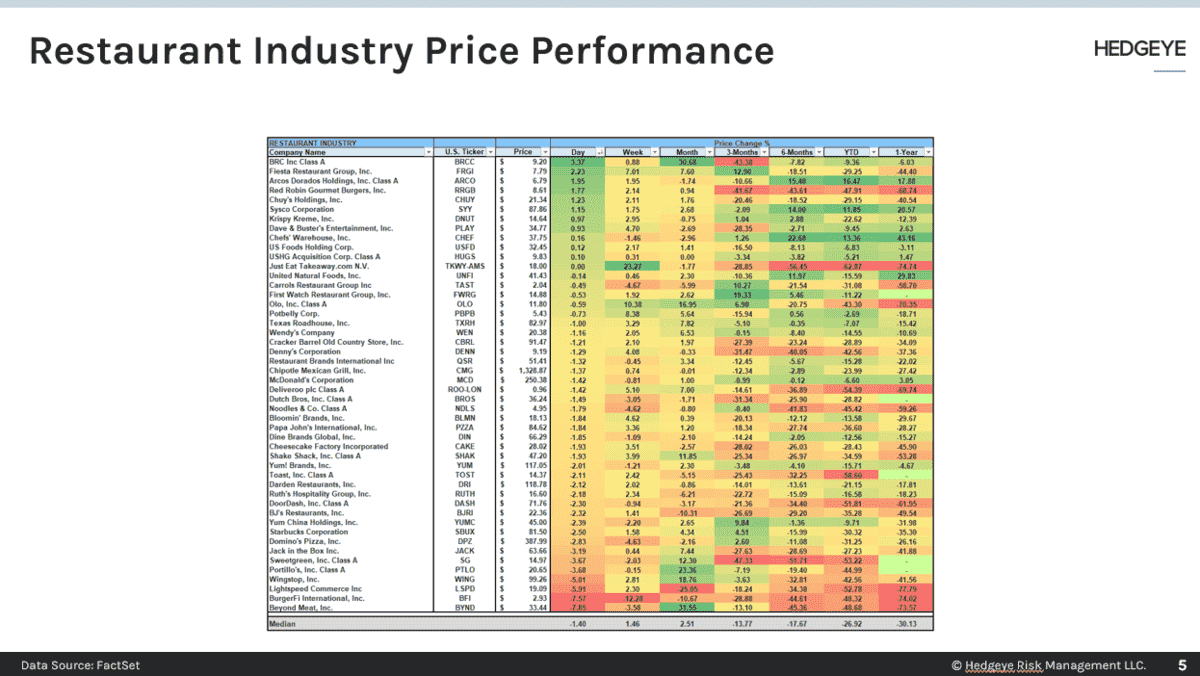

MCD Earings

MCD is a long

MCD 2Q22 Non-GAAP EPS of $2.55 beats by $0.08; Revenue of $5.72B (-2.9% Y/Y) misses by $100M. Global comparable sales increased 9.7%, reflecting positive comparable sales across all segments - U.S. increased 3.7%. Digital Systemwide sales in the top six markets exceeded $6B for the quarter, representing nearly a third of their total Systemwide sales. Margins are impacted by exiting Russia and inflation.

"Our second quarter performance reflects outstanding execution against our Accelerating the Arches strategy. By focusing on our customers and crew, enabled by a rapidly growing digital capability, we delivered global comparable sales growth of nearly 10%. Nonetheless, the operating environment across the competitive landscape remains challenging. While we are planning for a wide range of scenarios, I am confident that our plans and people position McDonald's to weather this environment better than others."

More after the earnings call.

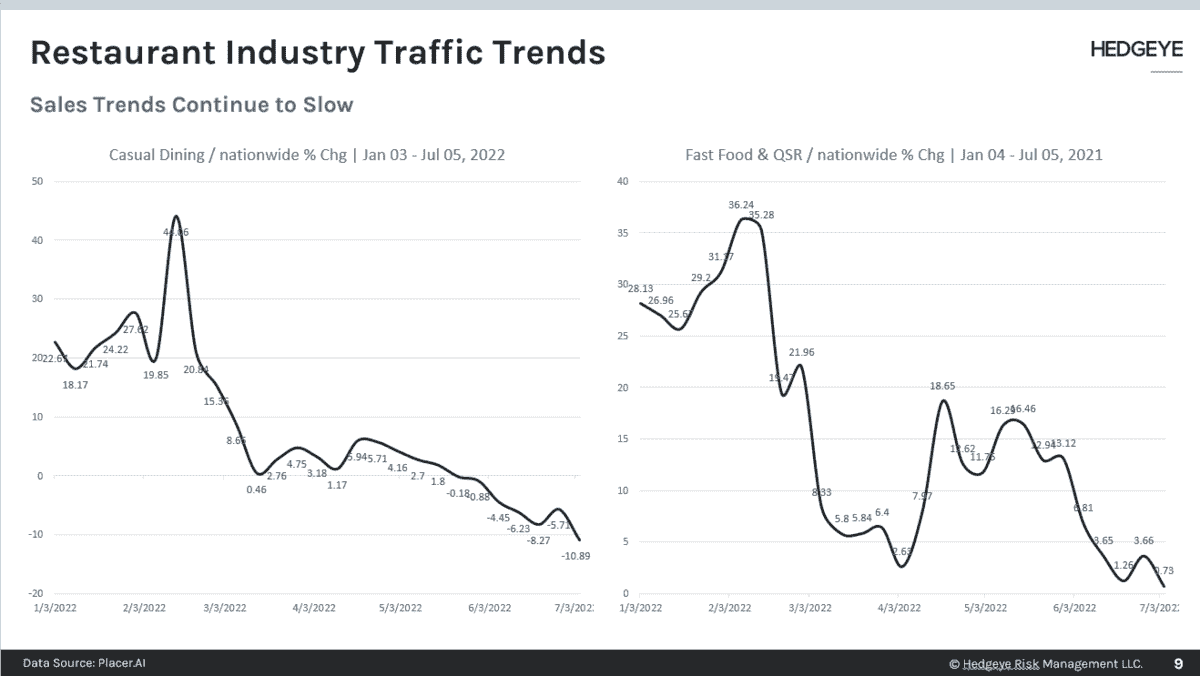

QSR Traffic Turns Negative

For the first time in 2022, the QSR segment of the industry is measuring negative traffic; Casual Dining is down double digits for the second week in a row

CMG Earnings

CMG is a SHORT

CMG is scheduled to announce 2Q22 earnings results AMC. The consensus EPS estimate is $9.04 up +21.2% YoY and the consensus Revenue Estimate is $2.245B up +19.0% YoY and SSS of 10.9% CMG's track record over the past 20 quarters is amazing, only missing EPS twice. We believe the CMG story is getting long in the tooth and the company is not immune from the industry slow down.