Position: Long Sweden (EWD); Short Euro (FXE)

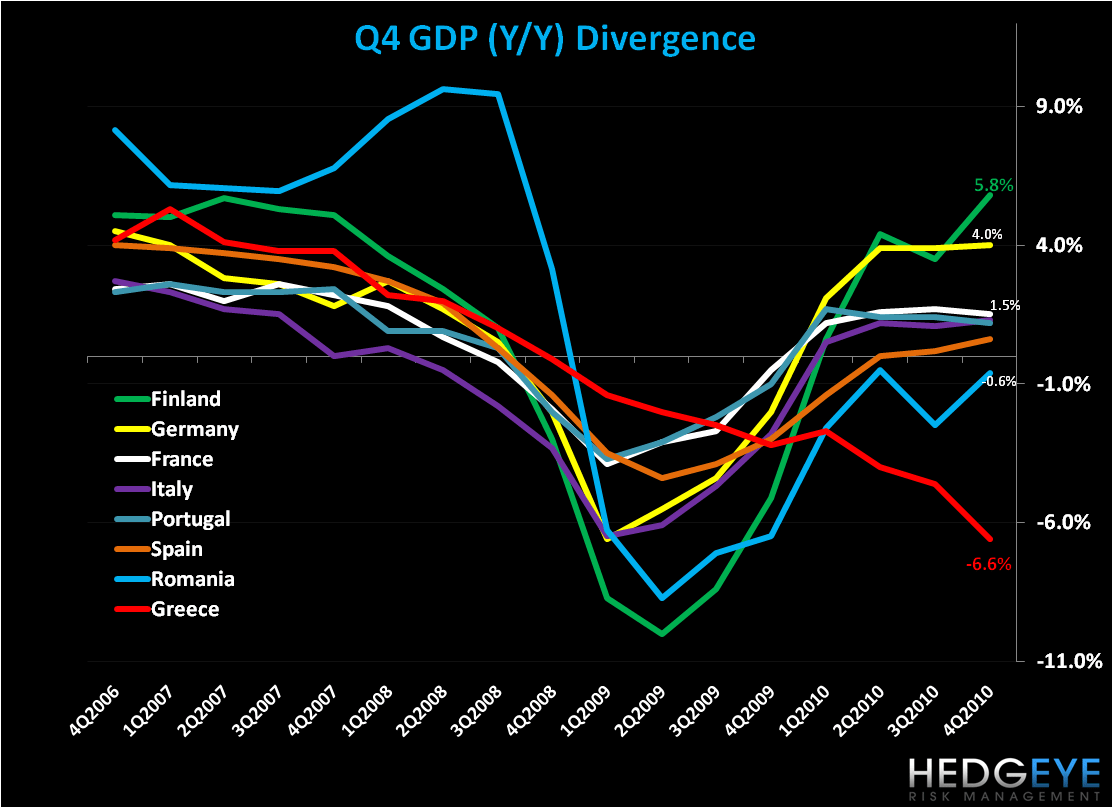

Although a lagging indicator, today Eurostat reported 4Q10 GDP for most European countries. As we’ve flagged over the last 18 months, the Sovereign Debt Dichotomy continues to drive divergence in economic performance across the region. In short, we’re of the belief that excessive levels of sovereign debt structurally impair long-term country growth.

Reinhart and Rogoff have helped defined these “excessive levels” of debt in their book titled “This Time is Different”, which proves with data over the last 8 centuries that the probability of default and significant GDP contraction occur when a country’s public debt exceeds the 90% of GDP level. While we’ll be the first to recognize that the austerity packages issued throughout Europe are an important step to improve debt and deficit imbalances and restore confidence from market participants, the PIIGS (collectively) have a long road ahead of them to pare back their fiscal imbalances that exceed this mark.

Paradoxically, the peripheral European equity indices are some of the best performers across global indices year-to-date, supported by the hope (and initial commitment) of China and Japan to buy European debt issuance, and optimism that a permanent bailout fund and new fiscal policy provisions will be agreed upon by the member states by the time leaders convene at the European Summit on March 24-25.

We’re managing risk around a downside correction in European equity markets; at a price we are comfortable owning countries with stable balance sheets, including Sweden which is in the Hedgeye Portfolio, and Germany.

Matthew Hedrick

Analyst