According to reports out this morning from CNBC’s Darren Rovell, Under Amour is adding another high profile endorsement to its portfolio with the signing of Cam Newton just weeks ahead of the NFL draft. The deal would not only secure one of the top players in the draft, but also suggests that UA’s endorsement strategy is the ‘new reality’ with related costs here to stay and most likely to increase at an accelerated rate. Here are a few of our key takeaways from the deal:

1) UA remains aggressive…big time. This is a big deal for them. It shows that they are not afraid of getting in bed with controversial players. Keep in mind that Nike is still reeling from Tiger. If they wanted Cam, they’d have gotten him. They probably played the conservative card here and did not submit an all-out bid – especially given that fact that they’re about to digest the NFL deal.

2) P&L item to watch…front-loaded SG&A associated with this deal. Keep in mind that they just endorsed Tom Brady as well. Could pressure margins in 2H.

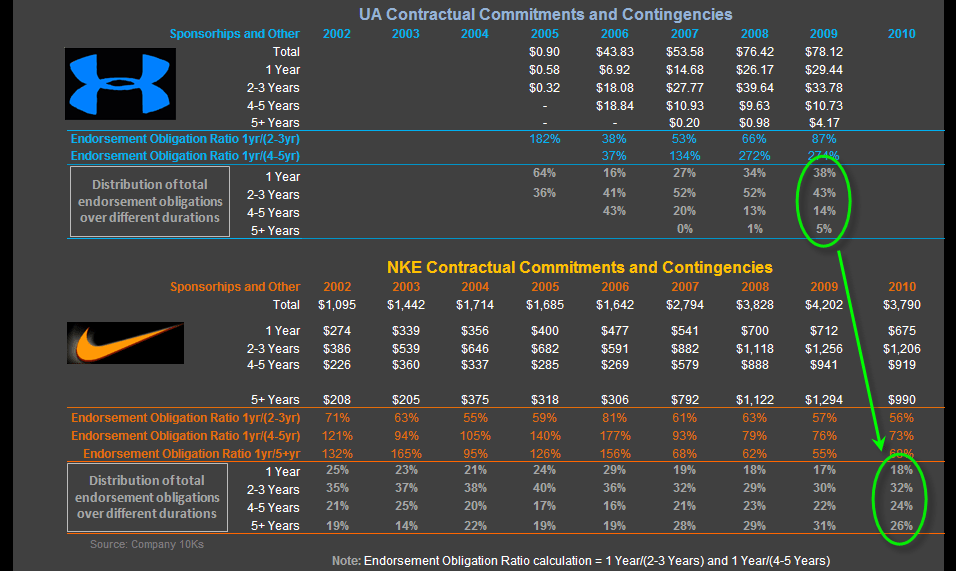

3) We’ve got to consider the implications to the balance sheet. The same way a retailer is required to provide off balance sheet lease obligations, the athletic brands need to show their duration of endorsements, which can be used as a key lever to impact reported earnings. Take a look at our updated analysis of both UA’s and NKE’s commitments below.

Nike’s deals are still spread rather consistently over the next 5-years. Under Armour’s on the other hand are considerably more front-end loaded with 81% of its obligations due in 3-years or less. As suggested when we posted on these schedules nearly a year ago in “Sunny D, Blind Side, and UA” on 3/29/10, this figure shrank over the past 12-months down from 86% reflecting the company’s latest additions (e.g. Michael Phelps et al.). We expect this trend to continue with the addition of Tom Brady and Cam Newton both of which are/will be long-term contracts, which is a change from the usual approach for UA. What’s likely to happen here is UA’s duration will continue to elongate as longer-term deals come on board. While we tend to feel uncomfortable with durations beyond 5-years, let’s consider that the endorsement/sales ratio for UA still only sits at 8%. This compares to Nike’s 21%. UA will definitely close that gap. Our sense is that if this is done at a measured pace, it can actually help the P&L before the balance sheet sheet comes into question. We’re not justifying a more aggressive approach…but this is simply the reality of where things are headed.