TODAY’S S&P 500 SET-UP - February 11, 2011

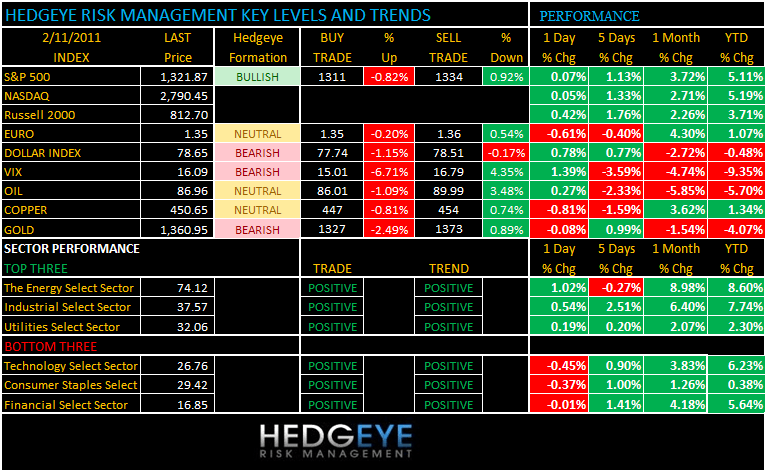

Equity futures are trading below fair value as events in Egypt send investors into defensive mode; safe haven trades are a consequence of the current political uncertainty with dollar assets in demand and the price of oil rising back above $87.00 per barrel. As we look at today’s set up for the S&P 500, the range is 23 points or -0.82% downside to 1311 and +0.92% upside to 1334.

MACRO DATA POINTS:

- 8:30 a.m.: Trade Balance, Dec., est. -$40.5b, prior -$38.3b

- 9:55 a.m.: U-Mich. Confidence, Feb., est. 75.0, prior 74.2

- 1 p.m.: Baker Hughes rig count, Feb. 11

- 9 p.m.: Fed’s Raskin speech in Park City, Utah on mortgage servicing

EARNINGS/WHAT TO WATCH:

- U.S. Treasury Secretary Geithner will present Congress with three options for reducing govt.

- Nokia says it’s forming a partnership with Microsoft and making Windows its primary smart phone platform, a bet that together the two cos. can better challenge Google and Apple. Nokia shares tumbled as much as 12%

- Research in Motion is working on software to allow BlackBerry PlayBook to run applications for Google’s Android, three people familiar with the matter say

- DuPont’s offer for Danisco is ~$320m too low as it doesn’t account for the food-ingredient maker’s market leading position, shareholder Elliott Associates says

- Creditors including billionaire Carl Icahn and Monarch Alternative Capital are targeting Blockbuster in a possible buyout for < $300m, person familiar with the matter says 71

- Blue Nile (NILE) reported 4Q EPS 41c vs est. 43c

- California Pizza Kitchen (CPKI) forecast 1Q EPS 3c-5c vs est. 12c

- Cephalon (CEPH) forecast 2011 adj. EPS $8.70-$9 vs est. $8.16

- Chipotle Mexican Grill (CMG) reported 4Q EPS $1.47 vs. est. $1.30

- DaVita (DVA) reported 4Q adj. EPS $1.13 vs. est. $1.12; sees 4Q oper rev. $1.65b vs. est. $1.66b

- Expedia (EXPE) reported 4Q adj. EPS 32c vs est. 36c

- Ford (F) said it will cut debt by $3b through redemption of trust preferred securities in March

- Kraft (KFT) forecast sees 2011 oper. EPS up 11%-13%, implying $2.24-$2.28 vs est. $2.32

- Leapfrog Enterprises (LF) forecast 2011 EPS 15c-20c vs est. 29c

- MannKind (MNKD) said it is cutting ~41% of its workforce

- Panera Bread (PNRA) forecast 2011 EPS $4.40-$4.45 vs est. $4.35

- TTM Technologies (TTMI) forecast 1Q adj. EPS 35c-44c, vs est. 39c

- Wright Medical Group (WMGI) forecast 2011 adj. EPS 88c-95c, vs est. 88c

- Wynn Resorts (WYNN) reported 4Q adj. EPS 91c vs est. 70c

PERFORMANCE:

As has been the case throughout much of the week, high-profile drivers remained few and far between, particularly with another fairly quiet day on the economic calendar. Nevertheless, we have day 4 of perfect = 9 of 9 sectors positive on TRADE and 9 of 9 sectors positive on TREND.

- One day: Dow (0.09%), S&P +0.07%, Nasdaq +0.05%, Russell 2000 +0.42%

- Month-to-date: Dow +2.84%, S&P +2.78%, Nasdaq +3.35%, Russell +4.03%

- Quarter/Year-to-date: Dow +5.63%, S&P +5.11%, Nasdaq +5.19%, Russell +3.71%

- Sector Performance: - Energy +1.02%, Industrials +0.54%, Materials +0.18%, Consumer Disc +0.13, Utilities +0.19%, Healthcare +0.03%, Financials 0.01%, Consumer Spls (0.37%), Tech (0.45%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 93 (+814)

- VOLUME: NYSE 1026.84 (+8.41%)

- VIX: 16.09 +1.39% YTD PERFORMANCE: -9.35%

- SPX PUT/CALL RATIO: 1.66 from 1.46 (+13.68%)

CREDIT/ECONOMIC MARKET LOOK:

Treasuries were back on the defensive yesterday after snapping a seven-day losing streak on Wednesday.

- TED SPREAD: 20.45 +0.203 (1.003%)

- 3-MONTH T-BILL YIELD: 0.12% -0.02%

- 10-Year: 3.70 from 3.65

- YIELD CURVE: 2.85 from 2.84

COMMODITY/GROWTH EXPECTATION:

- CRB: 339.95 +0.15%; YTD: +2.15%

- Oil: 86.73 +0.02%; YTD: -5.71% (trading +0.20% in the AM)

- COPPER: 454.35 +0.43%; YTD: +1.33% (trading -0.86% in the AM)

- GOLD: 1,362.02 -0.07%; YTD: -4.07% ( trading -0.35% in the AM)

COMMODITY HEADLINES:

- China, the world’s biggest grains consumer, will spend 12.9 billion yuan ($1.96 billion) to bolster grain production and fight drought, China Central Television reported today, citing Premier Wen Jiabao.

- Oil rose for the first time in six days as Egyptian state television said the president would address the nation. Egypt’s top military body is staying in session in response to the “legitimate” demands of the people, according to a statement.

- Australian coal’s premium over Europe is poised to widen as economies in China and India expand after narrowing 57 percent in the past month as floods in Queensland receded and demand for winter heating eased.

- Copper rose for the first time this week on renewed concern that the world’s mining companies will struggle to boost output fast enough to keep pace with rising demand in emerging markets.

- Corn rose to a 30-month high for a second day on signs that global demand is increasing for supplies from the U.S., the world’s largest grower and exporter.

- Wheat futures plunged the most since November on speculation that the highest prices in 29 months will slow demand and encourage farmers to plant more.

- Cotton futures climbed to a record for the second straight day after a report showed strong demand for fiber from the U.S., the biggest exporter.

- Buying interest was encouraged by newspaper reports in the U.S. Thursday morning highlighting tightening supplies of grain, cattle and hogs and projecting higher food costs to consumers.

CURRENCIES:

Australian dollar falls below parity with dollar as Reserve Bank Governor Glenn Stevens says policy makers judged it was “sensible” to keep interest rates on hold.

- EURO: 1.3626 -0.61% (trading -0.72% in the AM)

- DOLLAR: 78.25 +0.78% (trading +0.46% in the AM)

EUROPEAN MARKETS:

- FTSE 100: (0.27%); DAX: (0.18%); CAC 40: (0.90%); IBEX: (-0.86%) (as of 06:45 ET)

- European markets mostly trade lower for the 4th day; a choppy session as investors review the implication of Egypt's President Mubarak not immediately resigning

- Nokia dents Europe down 10%

- Germany Jan final CPI +2.0% y/y consensus +1.9%

- UK Jan PPI core +3.2% y/y vs consensus +3.0%; input +13.4% vs consensus +12.6%; output +4.8% vs consensus +4.4%

- Post the German Finance Minister and French Economy Ministers meeting today, German Finance Minister Schaeuble said he wanted a comprehensive EuroZone crisis package to be delivered in Mar, says Germany and French economic recovery is progressing well.

ASIAN MARKTES:

- Nikkei (closed); Hang Seng +0.53%; Shanghai Composite +0.33%

- Up until this week, the US demand side of Asian markets (South Korea, Taiwan, and Japan) was holding up just fine. In the last 48 hours however, both tech demand (earnings reports) and inflation concerns have infiltrated the KOSPI, registering a breakdown in both our TRADE and TREND durations. This is new.

- Garuda Indonesia plummeted on its trading debut, though the market rose +0.54%.

- Hong Kong reversed a morning decline to finish higher, but a 1% fall in HSBC Holdings limited the index’s gains.

- China turned a morning loss into a slight gain despite fears about the country’s monetary policy when the property sector rallied on a report that house prices rose in January. China Enterprise soared 10%.

- Australia fell -0.68% on concerns about Egypt, with major banks giving back some of their gains from earlier this week. Rio Tinto (RIO.AU) fell 2% on disappointment over the size of its share-buyback plan announced yesterday.

- On fears the shoe is still going to drop, South Korea fell -1.56% even though the country left interest rates unchanged, vs an expected 25 bp increase.

- Taiwan declined -2.57; Taiwan’s dollar had its biggest daily decline this year.

- Japan was closed for Foundation Day.

Howard Penney

Managing Director