Heading into CMG’s earnings after the market closes the stock is near an all time high and up 10% over the last 5 days and 15% over the past month. Consensus expectations are for CMG to have a good quarter - revenue is estimated to be $462.0M and EPS is expected to come in at $1.31. Same-store sales and restaurant level margins are expected to be +9.9% and 25.3%, respectively.

Guidance going forward is likely to be very different that what the company talked about last quarter. Last quarter, CMG was looking for 3% food inflation and since them food prices have surged. In addition, they now have a potential labor problem with the ongoing probe into the hiring of illegal immigrants by Chipotle restaurants. It will be interesting to see how they forecast what incremental costs will be in 2011.

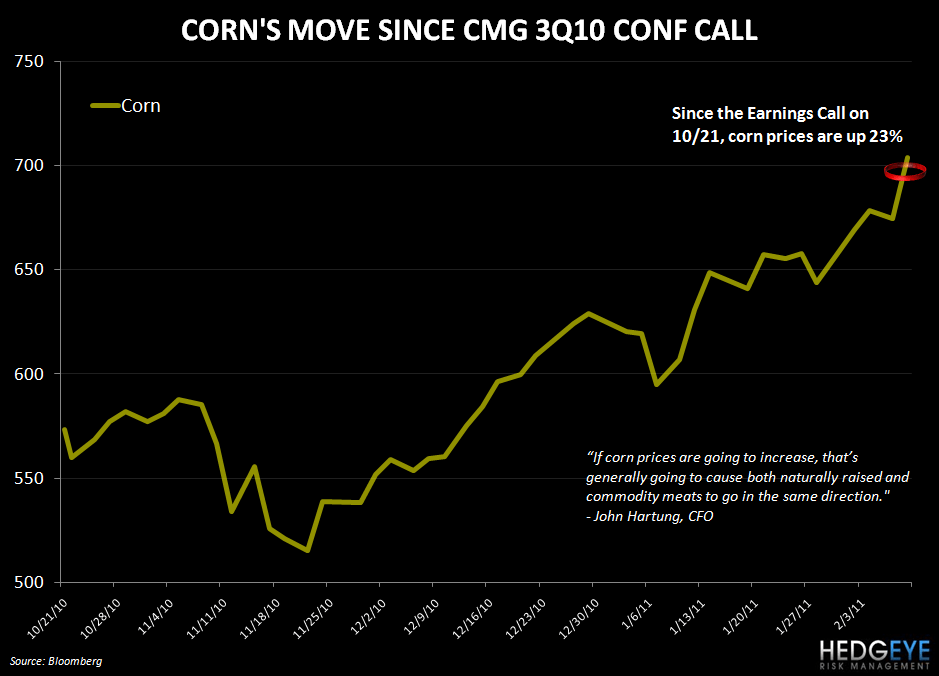

Here is a look at CMG’s commentary on some forward-looking commentary during their most recent earnings call on October 21st, 2010.

FOOD COSTS/INFLATION

“Food costs were 30.6% for the quarter, which is down 20 basis points from last year. Prices for avocados, corn, rice and chicken were slightly lower in the quarter, which were partially offset by increases in barbacoa and steak due to the continued rollout of naturally raised beef. We continue to expect modest increases in our food costs for the fourth quarter as we continue to invest in increasing our supply of naturally raised chicken and as prices for avocados increase due to a Chilean freeze…As we look to 2011, we will continue to invest in our Food With Integrity initiative and we expect inflationary pressure on many of our ingredients, especially chicken, beef, pork and avocados. As a result, we anticipate overall food cost inflation in the low- to mid-single digit range for 2011.”

“If we had 3% inflation, for example, that would be roughly 100 basis points on the food line” [assuming no price increase]

“If corn prices are going to increase, that’s generally going to cause both naturally raised and commodity meats to go in the same direction”

The chart below show the prices of key commodities since the last quarter's call.

PRICING

[In the event of a food price increase] “We would like to leak out smaller price increases than do a big giant increase all at one time.”

“We feel good that we have pricing power, it’s been two years now since we’ve raised prices in most of our markets…but we’re going to be patient about it. I think what we’ll do is watch what happens…see how the consumer responds to price increases of other competitors and if it looks like inflation is going to hold, increases are generally being accepted by consumers, then we’ll be prepared to increase prices if need be.”

“Typically if we’re going to try to offset inflation, and inflation’s 3%, if we’re going to raise prices at all, we would look for something in the same ballpark as inflation would be, so somewhere around 3%.”

LABOR COSTS

“If you have 3% inflation on food, we typically have inflation on our labor line of somewhere between 2% and 2.5% as well, something in that ballpark across many of the other line items”

“In the quarter, labor costs decreased 70 basis points to 24.2% and a 50 basis point decrease to 24.7% for the year. The decrease for the quarter was the result of labor leverage driven by the comp increase, as our restaurant teams did a nice job recapturing some of the labor leverage lost in 2Q, along with the 40 basis point accrual adjustment I mentioned earlier, which we don’t expect to continue in the fourth quarter.”

Howard Penney

Managing Director