The person paying the bills typically has a unique perspective on things and this came through loud and clear in the most recent survey of Small Business Optimism.

The Index of Small Business Optimism gained 1.5 points in January, rising to 94.1 (the best reading since the economy peaked in 2Q 2007); the index has moved sequentially higher 5 out of the last 6 months. The average reading before the recession started was 100.

Given the nearly almost 100% move in the S&P 500 since the bottom on March 9th, 2009, it is interesting to note that since its low of March 31st, the Small business optimism index is only up 16.2%. There are some interesting trends that emerge from the most recent report as it relates to how small business plans the move ahead in trying times.

CREDIT MARKETS

The most amazing statistic in the survey was that 92% of respondents reported that all their credit needs were met or that they were not interested in borrowing; 52% said they did not want a loan, up two points (12 percent did not answer the question) and only 3% claim that financing is their top business problem. Washington remains obsessed with the notion that small banks will not lend money to “creditworthy” firms and that this is holding back employment and economic growth. In this vein, the bureaucracy of D.C. persists in creating new programs to spur lending to small businesses, ignoring the fact that small business owners, for the most part, do not want a loan.

Hedgeye thought - Interventionist government policy is unwanted by the very parties it is touted to be aiding.

LABOR MARKETS WEAKNESS

According to the survey, the average employment change per firm was -4 down from a -1 in December. The December reading was the best reading since January of 2008 when it hit 0. The decline in small business hiring is consistent with the most recent number from the BLS, which showed the change in nonfarm payrolls of 36,000, significantly below the consensus expectation of 146,000.

Referring back to my post from 2/3/11, “HIGHLIGHTING THE RISKS TO GDP GROWTH IN 2011”, 4Q10 GDP growth was a robust 3.2%. However, this was accomplished with very little job hiring and can be completely explained by the by the fact that manufacturing and trade are leading the recovery, industries and activities that are not labor intensive.

Hedgeye thought - The labor intensive construction industry remains in a recession. We continue to believe that housing will remain depressed for the balance of 2011.

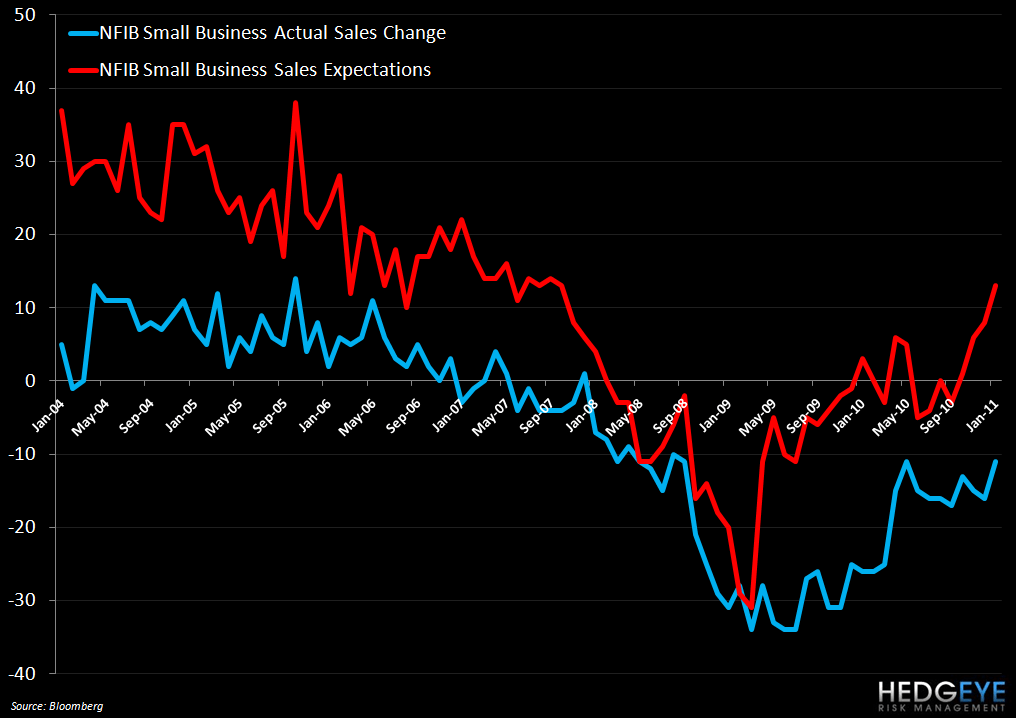

SALES

The net percent of all owners, seasonally adjusted, reporting higher nominal sales over the past three months improved by five points to a net -11%, 23 points better than March 2009 (near the recession bottom) but still indicative of weak consumer activity.

Hedgeye thought - Despite what we see from the conflicted government data, the main street consumer remains challenged.

INFLATION

The big deflationary pressure seen in 2009 and for most of 2010 has subsided. Seasonally adjusted, the net percent of owners raising prices was a -4, which improved from -5 in December and consistent with the 4Q readings. Importantly, plans to raise prices rose four points to a net seasonally adjusted 19% of owners, the highest reading in 27 months. As the theory goes, an improving economy (including rising stock prices), is likely to have more and more price hikes stick. The intention to raise prices moved up significantly from 15% in December to 19% in January; the highest reading since 2008.

Hedgeye thought - The tipping point for the consumer will come when companies stat to raise prices to protect margins.

EARNINGS

The need to raise prices is evident in the earnings trends. Reports of positive earnings trends improved points in January, registering a net negative 28%. More owners report that earnings are deteriorating quarter to quarter than rising. Part of this is due to price cutting and inflationary trends, but the overall environment is not supportive of employment growth.

Hedgeye thought - There is little incentive to add incremental labor in a weak demand environment.

CAPITAL SPENDING

The frequency of reported capital outlays over the past six months rose four points to 51% of all firms, higher than previous months, but historically low and far less than what is needed coming out of the Great Recession. Small business remain in “maintenance mode”, unwilling to put new capital to work. The percent of owners planning capital outlays in the future rose one point to 22%, but is still historically quite low. The demand environment continues to keep the small business owner on the sidelines.

Hedgeye thought - This speaks to the lack of confidence among business owners.

SUMMARY

Small business owners don’t need the free money from the Federal government. Expectations improved, but not spending and hiring plans. Although, Main Street disinflation is dissipating, inventory is lean but the top line continues to be a struggle. Small business need to raise prices despite a weak demand environment and are unwilling to add to their cost structure by hiring new employees.

Howard Penney

Managing Director