Overview

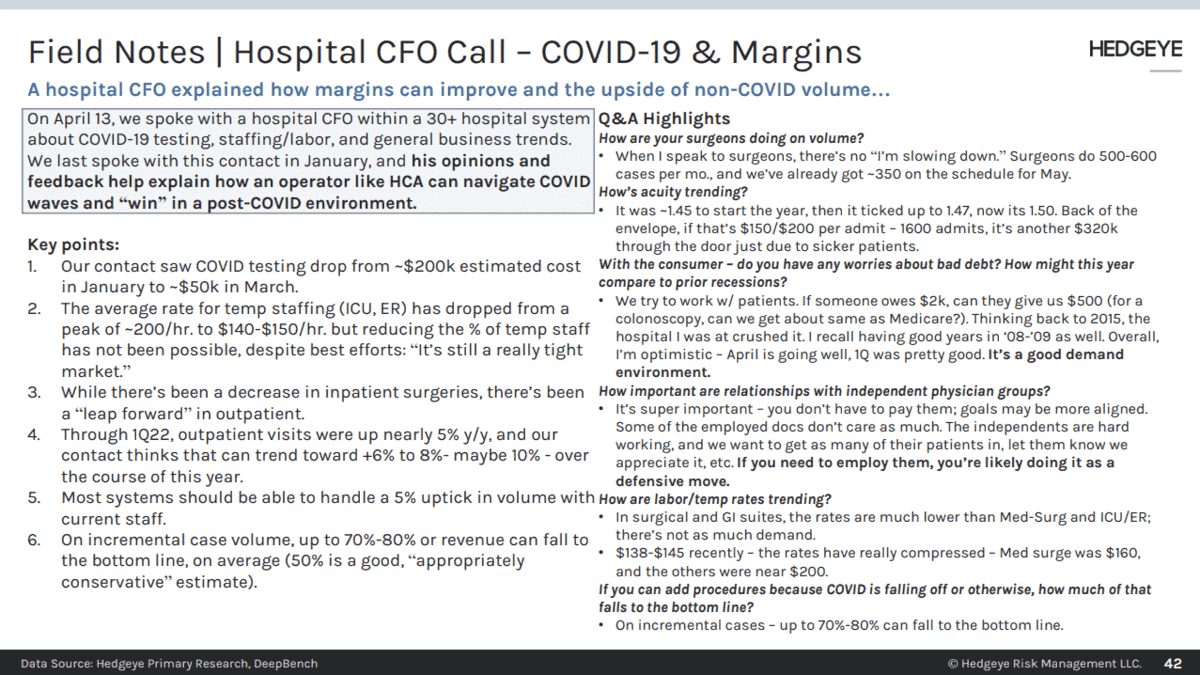

We spoke with one of our hospital CFO contacts in the Southwest within a 30+ hospital system on April 13th, 2022 and then again the week of 4/25 to check some of the assumptions around our HCA thesis following earnings. We came away from the discussions thinking that we had a good handle on the setup to start 2Q22 and how the reopen could look for HCA; however, the impact on margins in 1Q and exit velocity commentary didn't match our expectations. That said, we realized that an update to the AMN tracker was necessary as we were hearing that rates for temp staffing were dropping, and we think 2Q22 could be better than people think for HCA. We've seen non-COVID occupancy continue to climb post-Omicron and contract labor rates continue to drop from peak levels. What's good for HCA is likely bad for AMN, but it was clear that this executive has yet to find a way to reduce the overall percentage of agency staff due to a consistent supply/demand imbalance that's expected to persist into 2023.

Highlights

- The puts and takes of the 20% bonus for COVID patients and COVID testing payments seem to shake out in favor of hospitals if "normal" procedure volume replaces what's likely to be lost as Omicron recedes.

- Up to 60%-80% of the reimbursement for an incremental procedure can fall to the bottom line.

- Rates for ER/ICU nurses through agencies have been coming down but remain elevated: rates reached ~$195/hr. for our contact during the Omicron, were at ~$170/hr. as of late January '22, and were at $145-$150/hr. as of the end of March.

- Acuity remains elevated: our contact's case mix index started the year at ~1.45 (vs. 1.48 at the end of 2021) and is presently ~1.50.

- Deliveries are trending up to start 2022.

We highlighted the initial discussion during our HCA Black Book presentation and think the full, clean call notes are interesting given HCA's rising occupancy (69.84% as of our latest update) and our recent shift in sentiment on AMN's stock (from Long -> Short).

CALL NOTES

Edited lightly for length and clarity.

Background: Our contact has been CFO of hospitals across Southern states for the past 7-8 years. His current facility is a specialty hospital that "takes all comers" and has an "incredibly busy robot-assisted surgery program." Stats: ~27k annual ER visits, >7k admissions, ~3k deliveries, and >600 NICU admits annually (~$300MM in net patient revenue).

-

While there was enhanced revenue from the Feds and testing requirements varied by state – well, in January I think we paid about $200k for testing (~$100/test), but I didn't get $200k to cover that. If we had a lab, we might have been able to "make" that, but we outsource it, so what helps us now might hurt a hospital with a lab.

-

Overall, I would say there’s a little bit of an uptick in revenue from Feds, at least with all the facilities I'm familiar with; however, that's all been gobbled up by a significant need for contract labor at a significant cost.

- Medical DRG = lower reimbursement, but if it's $6k, yes, you'd get $1,200; however, it didn't meaningfully increase margins. There was an increased cost for either drugs, supply spend, or contract labor to offset that.

-

We were taking care of patients, [CMS] knew it was tough and more expensive, so IMO they did something for "us" - not all COVID patients are equal. If you put one on ECMO, it's incredibly time consuming, labor intensive, vs. someone with a simpler case.

-

Not in that case; no, I don't believe so. There was no kicker. It was for care of COVID patients, not if COVID were secondary.

-

For March it was ~$50k and April is trending about the same. Everyone coming in the door was getting a test - everyone in surgery, inpatient, ER... if a patient were admitted for a couple of days, another test might be ordered because it could change how the patient is treated or the phase of care.

-

When I speak to surgeons, there’s no “I’m slowing down.” Surgeons do 500-600 cases per mo., and we’ve already got ~350 on the schedule for May.

-

In surgical and GI suites, the rates are much lower than Med-Surg and ICU/ER; there’s not as much demand.

-

$138-$145 recently – the rates have really compressed – Med surge was $160, and the others were near $200.

-

We haven’t been able to replace the temp staff - we still have ~10% temp (~45 people).

-

Are you trying to move back to full-time? We are pulling any lever to do it, the challenge is, as I think I mentioned last time we spoke, we need 200k nurses per year, but we're only producing 150k. With traveling, if people were smart, they’ve put themselves in a good position financially – do it for couple of years, paid off debt, housing, etc. If not smart, they may have to come back and work as a FTE.

-

It's still a really tight market. I've had open positioned posted for up to 4 months with less than 5 applicants.

-

There's a willingness to hire LPNs vs. BSNs and/or take people from the field and train them up to fill gaps.

-

It was ~1.45 to start the year, then it ticked up to 1.47, now its 1.50. Back of the envelope, if that’s $150/$200 per admit – 1600 admits, it’s another $320k through the door just due to sicker patients.

-

We try to work w/ patients. If someone owes $2k, can they give us $500 (for a colonoscopy, can we get about same as Medicare?).

-

Thinking back to 2015, the hospital I was at crushed it, and I recall having good years in ‘08-’09 as well. Overall, I’m optimistic – April is going well, 1Q was pretty good. It’s a good demand environment.

-

Super important – you don’t have to pay them; goals may be more aligned. Some of the employed docs don’t care as much. The independents are hard working, and we want to get as many of their patients in, let them know we appreciate it, etc. If you need to employ them, you’re likely doing it as a defensive move.

-

On incremental cases – up to 70%-80% can fall to the bottom line.

-

Outpatient imaging is the lowest, up 1% y/y, on avg outpatient is up 10% y/y - outpatient GI is up 19%.

-

We've seen a decrease in inpatient surgeries vs. a leap forward in outpatient surgeries.

-

Up through 1Q, +4.7% on all outpatient visits – all outpatient across the board. I think that can even trend higher – people start hitting deductibles.

-

If I could see a 6% increase in outpatient, or 10% would be even better y/y - I think that's possible this year.

-

Do you have the staff for that?

-

Yes. CT or colonoscopies - a doctor doing 20 colonoscopies, if we add 1 or 2 at the end of the day, we're not bringing in new staff - the incremental expense is low. That's why we can see 70-80% drop to the bottom line.

-

May not see it this year, but we’ll start to see more pain because of deferrals - bladder cancer, lumps that = cancer, Stage 3 vs/ earlier detection of colon cancer. People thought they were just tired but it's something worse.

-

On your earlier question - on staff. We all have ratios to abide by – if you do 600 admits a month, now doing 630 (one more per day) that shouldn’t change staffing matrix. Even if 2, shouldn’t change it.

-

Starting to feel some of it, but haven’t noticed it in finance, yet. The big question – take Baxter, when will they stop putting factories in PR (hurricanes) or China – or in Mississippi which is prone to tornadoes… companies must stop doing that. Oklahoma is open for business – some of the other Red states are too. Move there.

-

You can run 50% to 120% - that’s the range. Licensed for 100 beds, care for 100 pts. We're running at around 60-65% right now.

-

Deliveries have been down across the board for a while, but we’ve actually seen an uptick this year – we're +5% on deliveries thus far in 2022 (y/y).

Please reach out to with feedback or inquiries.

Thomas Tobin

Managing Director

Twitter

LinkedIn