The Golden Arches are still infallible in the eyes of the sell-side.

Whenever you find yourself on the side of the majority, it’s time to pause and reflect.

-Mark Twain

A week ago, I held a conference call on MCD and the lofty expectations that I feel the company is unlikely to meet in 2011. The Black Book I published that day detailing my thesis kicked off with a Mark Twain quote. I think another of his quotes, above, would have worked equally well. The Street adores MCD and is not keen to attach any real conditions to that affection.

In the days following my bearish conference call with clients I have heard plenty of push-back. Having had time over the past week to think through my thesis further, my confidence in my thesis is high. Several positive sell-side notes have helped bolster the price this week; to be clear, my call is for MCD to miss investor expectations from a sales and margins perspective for the year 2011. I would like to take a few of the key points the bulls have made and address them.

In no particular order:

Bull case: MCD can pull the trigger on price increases in 2011, giving significant resilience to comparable restaurant sales growth.

Hedgeye Thought: MCD has held back on price increases during 2010 and the value proposition that the chain offers is a large part of its success. Given the outlook for the U.S. consumer in 2011, I would be less-than-confident in MCD’s ability to take pricing without significantly impacting traffic given the fragile nature of the U.S. economy’s “recovery”. In addition, increased prices will only drive more consumers to the $1 menu, which is an unprofitable proposition. Housing headwinds and anemic job growth, coupled with rising costs, will pressure the consumer this year.

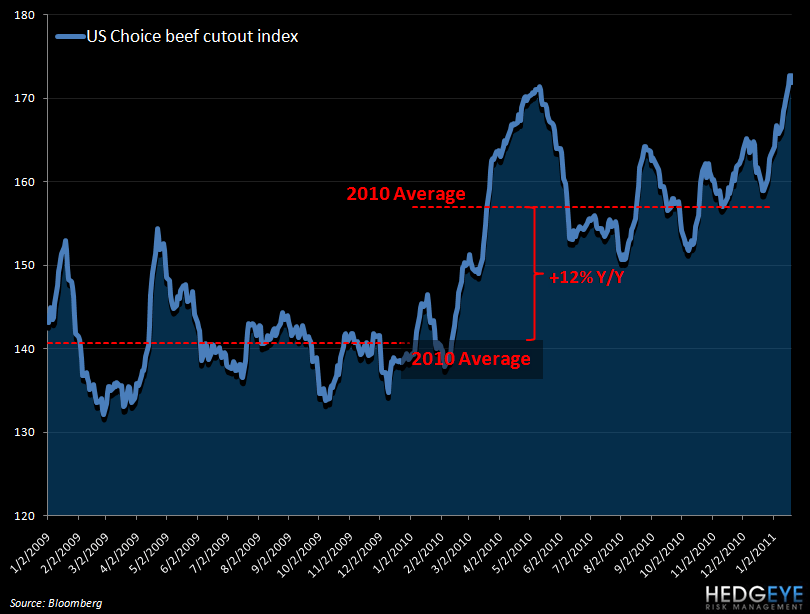

Bull case: MCD benefits in times of rising food costs. There is a 0.45 correlation between at-home inflation and fast food traffic.

Hedgeye Thought: First of all, I would be hesitant to wager too much on a correlation of 0.45. Rising costs are a problem for the MCD system. I am including a chart of beef, below, and one can clearly see the parabolic year-over-year move that QSR chains are enduring at the moment. Without a doubt, the franchise model insulates shareholders somewhat from this risk but ultimately, with franchisees competing with other restaurants for value-seeking customers, the cost will have to be passed on to customers – many of whom are feeling a similar squeeze in terms of inflation (gas, education, food, clothing). The reality is top line trends and input costs cannot be considered in isolation of the other. I am not sure the MCD customer is ready for a price hike at this point.

Bull case: New menu items will continue to drive sales at MCD and they will easily gain leverage and offset cost increases.

Hedgeye Thought: In the Hedgeye MCD Black Book, published last week, I discuss the over-complication of MCD’s menu and the knock-on impact on operations. This morning, a note published by Janney Montgomery, albeit with a “Buy” rating, detailed a survey of franchisees with some interesting commentary pertaining to the menu. One question was “Is the menu overly complicated?” While some of the answers cited expressed no desire to reduce or simplify the menu, the vast majority expressed an emphatic view that the menu was not only confusing customers, but also confusing employees and compounding operational difficulties. The development that franchisees are facing increasing costs and conflict with Oak Brook is not positive for MCD.

Bull case: Inflation may be an issue, but it’s a sum zero game and competitors will likely take price before MCD, allowing them to take more price and drive same-store sales.

Hedgeye Thought: That may be true conceptually but, absent any magic tricks; MCD cannot persuade consumers to keep paying for smoothies, frappes and lattes at higher prices. As I illustrated in my Black Book published last week, frappes and smoothies accounted for more than 100% of same-store sales growth in 2Q and 3Q, respectively. As prices are increased, consumers will purchase less of these discretionary items. In 2011, this would mean pressure on margins year-over-year given that beverages are higher margin products than more staple products such as burgers. With a complicated menu creating operational inefficiency, an increase in customer focus on low average check items will not help franchisees’ profitability. Other “margin enhancing” initiatives being touted by many on the sell-side are also unproven at best. 24 hour restaurant openings, in particular, is not a new initiative and an idea I am less-than-convinced about. BKC did not find this initiative accretive to their earnings.

Howard Penney

Managing Director