This note was originally published at 8am on January 12, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The dogmas of the quiet past are inadequate to the stormy present. The occasion is piled high with difficulty, and we must rise with the occasion. As our case is new, so we must think anew and act anew.”

-Abraham Lincoln

I recently pulled off the shelf Doris Kearns Goodwin’s book "Team of Rivals" which looks at the political genius of Abraham Lincoln. It’s an amazing account of how Lincoln, as president, was able to bring his “disgruntled opponents” together to complete the task of saving the Union. As Lincoln did, Barack Obama must pull together a team of rivals and win the respect of his competitors to help us navigate the stormy seas ahead.

If the United States’ economy were a vessel, it could be said that she has held up quite well over the past couple of years. Through the Great Recession, government bailouts, flash crashes, and the most contentious political climate in some time, the United States keeps cruising.

How much secular damage was sustained in the “economic storm” or was simply deferred by the Fed grabbing its cavernous bucket and bailing water from inside the ship back overboard is unknown.

Consumers don’t know, politicians don’t know, CEO’s don’t know, and you can bet a dollar, I don’t know. What I can tell you with certainty is that at some point the structural problems with the U.S. economy need to be addressed sooner rather than later. Fans of Big Government enjoy preaching the folly of applying long term solutions to short term problems.

While not ideal, clearly long term solutions that ensure economic progress in the long term, notwithstanding short term pain, are preferable to short term solutions that never address the long term, leaving us and our posterity to forever bail buckets of water over the side of the ship while we hope and pray for a miracle.

All the while, the long term problem grows larger, but politicians and policymakers keep their jobs. The mounting of debt upon debt by governments around the globe is leading to inflation on a global basis.

I would be remiss to ignore the various supply-side shocks that have occurred around the world related to weather and other factors. However, simply stated, the inverse correlation between the dollar and commodities denominated in dollars remains high and the U.S. consumer is feeling the effect of that. U.S. consumers are not alone; India, Brazil, China and many other countries around the world have seen inflation break out to the upside recently.

Food inflation, in particular, is causing significant social unrest in some countries which is drawing political attention. India’s government has adjourned to address the problem of rising food costs there and Algeria saw riots yesterday over food costs. For now, consumers’ wallets in the U.S. have been relatively shielded from the impact of food costs increasing over the past 6 months. However, if and when these costs are passed along in addition to the backdrop of high gas prices, it could greatly impair the “recovery” that is now consensus.

Today, Thailand joined the party and raised its benchmark raised interest rates for the fourth time in seven months and signaled it will boost borrowing costs further to contain inflation. And this morning, officials from Mozambique to China are signaling their belief that rates in their respective countries will be raised in the near-term.

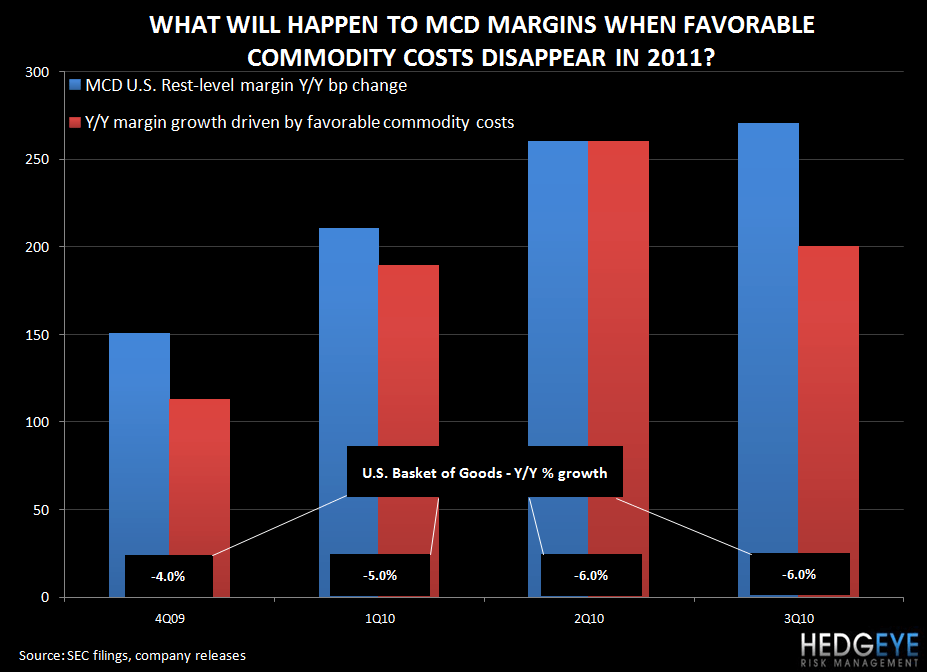

On a more granular note, one company that will begin to feel the pain of higher food inflation in 2011 is McDonald’s and I don’t believe the bullish consensus has fully accounted for this. Last year McDonald’s saw its basket of commodities decline by 5-6% and, accordingly, restaurant level margin rose by over 200bps from lower food costs alone. I have other concerns which are more structural in nature and those will be addressed, in detail, on a conference call with clients on Friday. For qualified prospective institutional subscribers, please email sales@hedgeye.com for more details.

Also on Friday, the Hedgeye Macro team will be discussing its three themes for the first quarter of 2011 and they are:

(1) American Sacrifice - We are bullish on the USD and we will focus on how the Q1 macro calendar of events (Ron Paul auditing Bernanke, midterm election spending cut promises, the debt ceiling debate and debt/deficit commission decisions) are supportive of a strong USD as the country begins to address its long-term fiscal problems.

(2) Trashing Treasuries – We are bearish on US Treasuries. The breakout in global inflation, sovereign, State, and municipal risk and rising global interest rates are a problem for treasuries.

(3) Housing Headwinds Phase II – We remain bearish on housing and continue to believe that a decline in home prices will be a governor on consumer consumption in 2011. We will update our view on how much further home prices have to fall over the next 12-months according to the supply and demand issues facing the industry.

It’s now just under two hours before the market opens and equity futures are trading higher in a continuation of yesterday’s modest gains with the early focus centered on Portugal's bond auction which went better than expected. Also overnight, bullish sentiment increased to 57.3% from 54.5% in the latest Investor's Intelligence poll, while the ABC consumer comfort index improved to -40 from -45; it is now at its highest level since 2008.

While all of this is good news for equity markets, it’s an ominous sign that all of the early dogs of the S&P 500 so far this year (YTD price changes below) are predominately consumer names that have been impacted by either weaker-than-expected consumer spending or inflation pressuring margins or a combination of both. I expect this list to grow as debt mounts, sovereign debt concerns accumulate, and inflation is passed through to the consumer.

SCRIPPS NET: -7.79%

MACY'S: -8.14%

TARGET: -8.22%

GAP: -8.22%

ABERCROMBIE & FITCH: -8.24%

VULCAN MATERIALS: -8.70%

GAMESTOP: -11.76%

FAMILY DOLLAR STORES: -13.02%

CONSTELLATION BRANDS: -13.18%

SUPERVALU INC: -21.18%

I’m not the only one using a “stormy” metaphor today as the snowstorm continues outside and CNBC started Squawk Box today with the Doors classic song “Riders on the Storm.”

“Into this house we're born

Into this world we're thrown

Like a dog without a bone

An actor out alone

Riders on the storm”

Function in disaster; finish in style

Howard Penney