This note was originally published at 8am on January 07, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Man’s life is brief and transitory, literature endures forever.”

-Persian poet

I’m in the middle of reading Rory Stewart’s The Places In Between where he tells the risk management story of walking alone across Afghanistan. He ends one of his chapters with that quote. It got my attention.

It should have. Every morning, day, and night, we market people walk alone with our P&L. We can’t drop our track record on someone else’s lap. We can’t pretend it’s not there either. No matter where we go, there it is…

That’s not life, but it’s certainly a big part of mine. Within that part, there certainly are a lot of places in between. All the while, I suppose I’m challenged with building bridges in a lot of those places between market prices and Transitory Expectations.

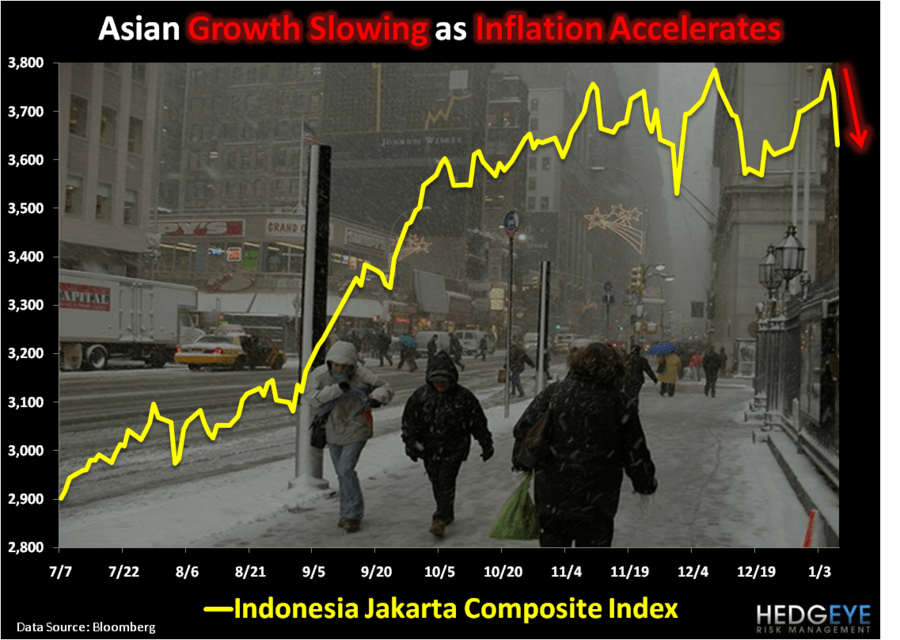

From a US-centric stock market investor’s perspective, expectations for this morning’s US Employment Report are extremely elevated. From a Global Macro investor’s perspective, from Indonesia getting tagged for a -2.8% loss overnight on inflation concerns to Gold testing 5-week lows, there’s a lot more going on.

That’s not to say that a Transitory Expectation for a US-centric economic data point doesn’t matter to Global Macro Risk Managers. It does this morning. Big time. But what exactly are those expectations and how can we proactively prepare to profit from them?

In an intraday note yesterday titled “Government Whispering”, this is how we framed it up:

- A Whisper of 580,000 US payroll adds has been going around all week

- Every market rally (from Wednesday’s pre-market futures lows) has been followed up with people reminding me of the whisper

- Government Whispering is turning into the casino that Big Government Intervention built into our markets – get used to it

Where are we at on estimates versus expectations:

- First, always remember that governments, to a degree, manipulates these numbers

- In our most bullish scenario, the payroll number could be at least 3x consensus (it started the wk at 125,000 which is a bit of a joke)

- The question now is can it be 2x that (or better than the whisper of 580,000)?

In terms of what an improving (in the very short term) US jobs picture actually means for the interconnected macro markets:

- BONDS: are definitely baking this in (collapsing UST’s have been since NOV and UST yields are bullish TRADE, TREND, and TAIL in our model)

- CURRENCY: definitely (maybe overly) baking this in (USD had a monster week, up +2.3% for the week-to-date ahead of the print)

- STOCKS: are trying their best to bake this in, but I think they’re going to look late – too late because they usually are

That’s the thing about Transitory Expectations in markets – by the time consensus realizes what they are, they’ve moved onto the next.

The key, in both Global Macro risk management and in life, may very well be to live in the moment. I’m not Buddhist, but I do respect the thought process behind the principle of playing the game that’s in front of you. After this morning’s US Employment Report is printed, that game is gone.

Post the 830AM EST report, I think US-centric investors will be forced to face the fiddle on the Expectations Mismatch between what they think the US Consumer is doing now versus what the US Consumer did in November to early December.

While everybody was pumping up Transitory Expectations of tax cuts and QG2 into their year-end Consumer Discretionary portfolios, evidently there was this little critter called reality toiling in the night.

At first, the Consumer Discretionary bulls said Best Buy’s (BBY) collapse was “secular” to their business. Then they said that McDonald’s (MCD) breaking down was due to some hedgies rotating into Best Buy because, I guess, Ackman was going to charge 2 and 20 to buy that one low. Now they’re saying that a broad based selloff in the Consumer Discretionary sector yesterday was due to the snow?

Here’s what some major US-centric Consumer Discretionary names (I mean names with market cap) did yesterday:

- Target (TGT) = -7.4%

- Gap (GPS) = -6.9%

- Macy’s (M) = -4.0%

I guess, with the Consumer Discretionary sector being the top US Sector performer in 2010 at +25.7%, bullish Transitory Expectations were a little off…

Back to the Global Macro risk management picture of Global Growth Slowing as Global Inflation Accelerates, most Asian and European stock markets have been sufficiently adjusting their bullish expectations to the downside all week. Last night, in addition to Indonesia trading down a ton, India was down -2.4%, Thailand lost -1.4%, and Taiwan was down -1.1%. After closing down -17.4% in 2010, Spain is already down -2.7% for 2011 to-date.

If the US stock market perma-bulls want to tell me that all of Asia and parts of Europe are slowing because US growth is strengthening, they can go do that. But they may very well have to adjust their Transitory Expectations after the last lagging bullish economic data point from Q4 is out of the way.

My immediate term support and resistance levels for the SP500 are now 1264 and 1280, respectively. Yesterday, I raised 3% cash, taking our allocation to US Cash back up to 52% in the Hedgeye Asset Allocation Model by selling our 3% position in Healthcare (XLV) on strength. We remain long the US Dollar via the UUP and short Gold (GLD).

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer