Today, the BLS released its monthly jobs report showing that the U.S. economy added only 103,000 jobs this December, compared with the median forecast of 150,000 according to Bloomberg Estimates.

November payrolls showed a revised 71,000 increase (previously 39,000) with October payrolls up a phony 210,000 in revision (previously 172,000). The October revision would have been reported as a gain of 190,000, if the BLS consistently reported its monthly recasting of seasonal factors.

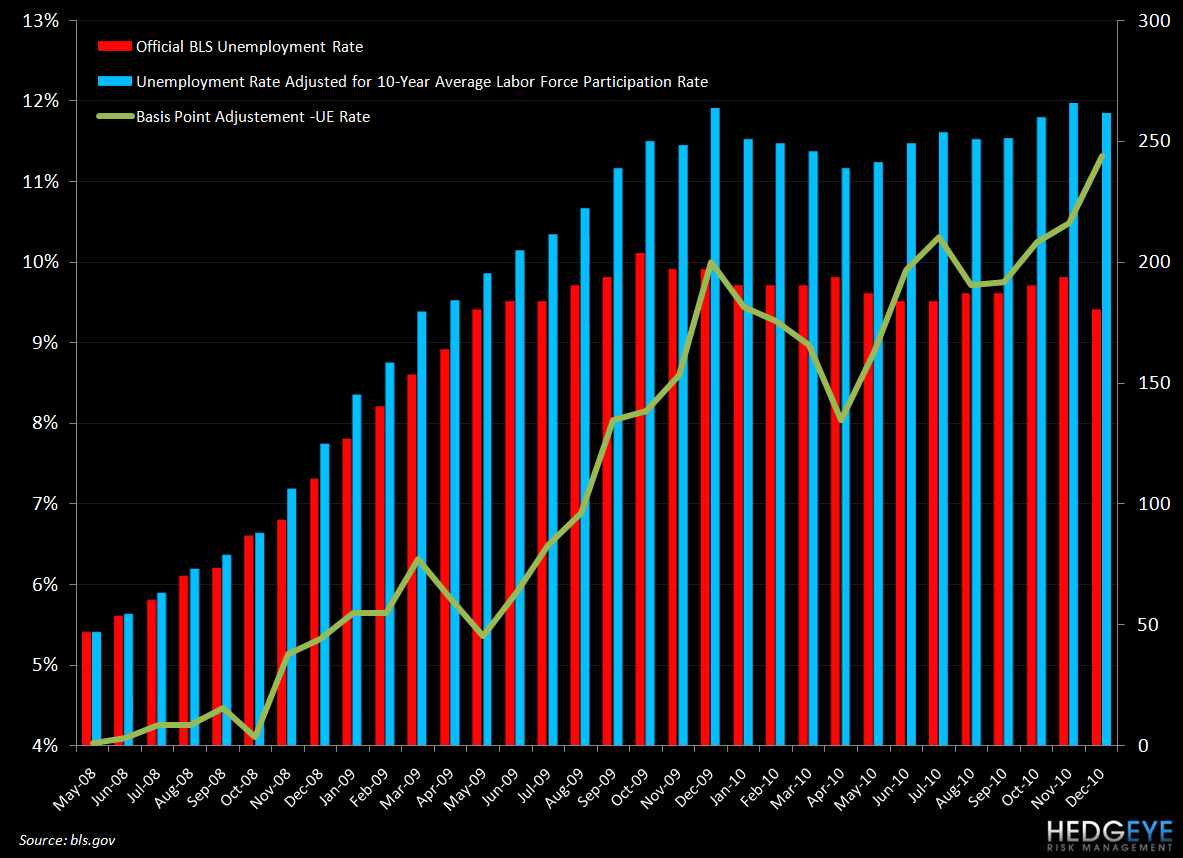

While the unemployment rate released today, 9.4%, came in well below expectations, the primary reason for this is that the labor force in America has plunged (decreased by 434,000) to a fresh 25 year low. Where is the unemployed population going? More importantly 260,000 Americans dropped out of the labor force entirely. This means that the Obama economy is now driving Americans out of the labor force faster than it is bringing them in.

This is akin to governments with net emigration (Ireland, for instance) publishing unemployment rate figures that do not accurately reflect the true extent of the decline in employment opportunities for their citizens. The chart below indicates how unemployment rate would look if the labor force participation rate were maintained at the average from January 2000 through December 2010. Clearly the declining participation rate is having a dramatic impact on the numbers.

Cronyism is alive and well in Washington. The remaking of the Obama administration and his investments is interesting to say the least. How do the following three nuggets augur for the promise of “change”:

- Peter Orszag has gone to Citibank (Obama owned bank)

- Obama named Gene Sperling as NEC Director (formally of Goldman Sachs, another institution that benefited from government handouts)

- Named Bill Daley as President Barack Obama’s Chief of Staff (JPM superstar and beneficiary of the government funds)

The dependence on close relationships between business people and government officials is a tight as ever, but our economy can’t generate any jobs and consumers are facing a severe squeeze on their wallets as inflation goes higher.

Keith provides ample volume on the topic of inflation each day via The Early Look. Today, however, we have heard Ben Bernanke on inflation and other matters as he testifies with the Senate Budget Committee in Washington. On the subject of inflation, Bernanke once again downplayed concerns, stating plainly that, “inflation is 1% including food and fuel”. When you decide what the weightings are to comprise a number, you can make that number whatever you want it to be. Keith has had several thoughts on inflation during the testimony that he communicated over his @keithmccullough twitter account that I think are worth sharing:

- Here comes Bernanke justifying his #inflation view w/ a completely compromised and conflicted US govt calculation - rest of world be damned

- Do you think The Ber-nank knows what twitter is? its his Waterloo

- you won't hear The Ber-nank disclose that his #inflation calc has 41.96% weight on "owners’ equivalent rent"; this is embarrassing America

- I'm not being disrespectful about that Ber-nank pt either; no Global Macro risk manager worth his/her shirt would hire Bernanke to trade P&L

- Bernanke is either incompetent on global macro matters or lying

- there's no conspiracy theory in govt calculations, they are simply conflicted and designed to obfuscate

- and on growth - he uses the "blue chip" sell side estimates - nice

Rounding out the government’s TV campaign today was President Obama, commenting on the job growth trend being “clear” and to some extent he is correct given the gains in private sector jobs over the past twelve months. However, the rate of growth is still indicating fragility in the economy and hesitancy on the part of corporations to accelerate hiring further. Retail sales results for December and ABC consumer confidence have both lent credence to this hesitancy. Whispers of 580k may abound, but those running P&L’s, not Bernanke or even Obama, will decide whether or not to accelerate hiring in the broader economy.

Howard Penney

Managing Director