This note was originally published at 8am on January 06, 2011. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“For some of them, inflation is not so bad; they even ask for a continuation of it, because they are the first to profit from it.”

-Ludwig von Mises

“For some of them” – that’s a critical preface, to a critical economic statement, during critical global economic times. If you’re reading this right now, consider yourself just like me . We are the fortunate ones. We can make money being long inflation.

If you haven’t read von Mises’ Fourth Lecture titled “Inflation” yet (in Economic Policy, Ludwig von Mises speeches; Argentina 1959), you should. On page 45 he goes on to write that:

“And there are always people who favor inflation because they realize what is going on sooner than other people do. Their special profits are due to the fact that there will necessarily be unevenness in the process of inflation… But of course, the politician in power who proceeds toward inflation does not announce: I am proceeding toward inflation.”

Unlike the Big Government monetization of debt experiments gone bad of Jimmy Carter (and then Bernanke-Lite Fed Head, Arthur Burns), how appropriate the lessons of history are that stand the test of time…

I’m long inflation.

In fact I got longer of inflation on the “buying opportunities” I have seen in commodities and currencies throughout the week. I have taken my asset allocation to Cash down in the Hedgeye Asset Allocation Model from 61% (at the beginning of the week) to 49% as of yesterday’s close.

How does one get long of inflation?

- Buy Commodities (we’re long oil, OIL, corn, CORN, and sugar, SGG)

- Buy Currencies whose countries have inflationary trends and an upward bias to interest rates (we’re long US Dollars, UUP, and Chinese Yuans, CYB)

- Short Bonds (we’re short short-term US Treasuries, SHY)

Of course, you can be long stocks too, which we are in both Germany and the US (admittedly too light in the shoes on the US side as we are long Healthcare and Energy, but short Tech and Consumer Discretionary).

That said, too light on Equities when the rest of the world wakes up to what we are really doing to world populations with trivial things like food inflation is definitely the place that the risk manager in me wants to be.

What are we (“some of them”) doing to most of them?

We’re starving them.

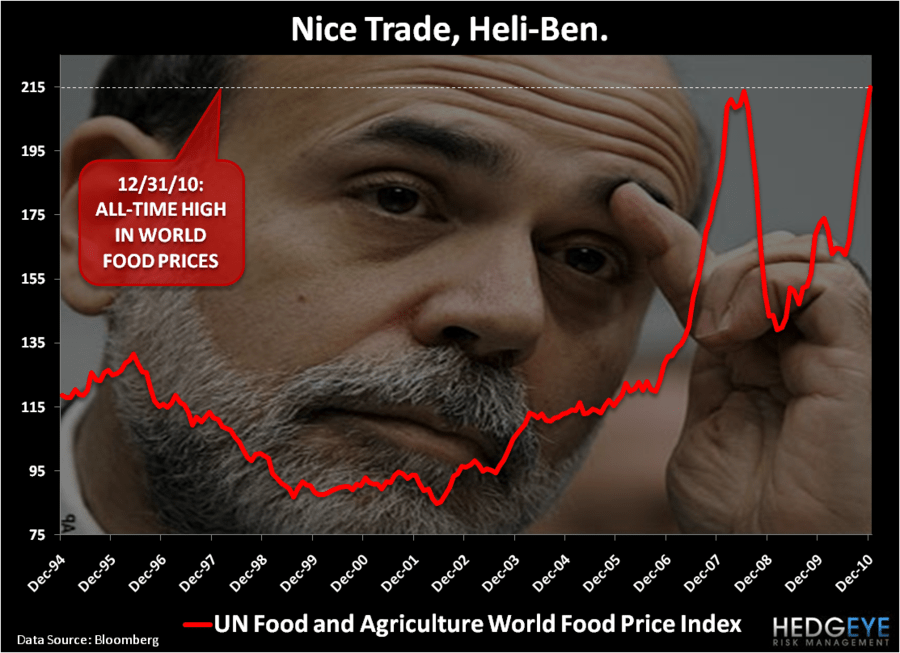

Now maybe Wall Street couldn’t give a damn about this. But I do. Here’s the data on world food prices (per the United Nations, not The Ber-nank):

- World Food Prices hit record ALL-TIME highs in December (on historical matters, ever is a long time).

- The commodities basket (55 commodities in the UN’s calculations to smooth out what’s “core”) has eclipsed the 2008 all-time high.

- Global grain production will have to rise at least 2% in 2011 to meet demand and avoid further depletion of stocks (UN agency).

The wizardry of the US Government’s calculation of inflation (CPI) is in the data as well. Ben Bernanke stares into the 60 Minutes cameras and does God’s work, under oath, saying that he didn’t see 2008 inflation with $150/oil or 2010 inflation with all-time record high world food prices. Charlatanism redefined.

When a professional politician or anyone who gets paid on inflationary terms tells you there is no inflation in the US, this is what they mean:

Top 6 Current US CPI Weighting:

- Housing: 41.96%

- Transportation: 16.69%

- Food and Beverage: 15.76%

- Recreation: 6.44%

- Medical Care: 6.51%

- Education and communication: 6.51%

*they’ve changed the CPI calculation 9x since 1996 (I wonder why)

So, obviously, the takeaway here is that Bernanke doesn’t see inflation because, like Hedgeye, he is bearish on US Housing. Unlike Hedgeye, he must think that the entire world works in NYC or Washington DC, where you don’t cook or drive to work.

Here’s another way to think about Global Inflation Accelerating and its impact on an interconnected global economy:

World Populations:

- China 1.341B people = 19.5%

- India 1.192B people = 17.3%

- USA 310M people = 4.5%

- Indonesia 237M people = 3.5%

- Brazil 190M people = 2.8%

- Pakistan 171M people = 2.5%

And across the world’s populations, here are this morning’s fresh off the Macro Grind global inflation reports for December:

- India food inflation reported at +18.32% year-over-year growth

- Russian inflation (CPI) hitting another new high at +8.7% DEC vs +8.1% NOV

- Kazakhstan inflation (CPI) +7.8% DEC vs +7.7% NOV

- Uruguay inflation (CPI) +6.93% DEC vs +6.87% NOV

I know – who cares about them people in Uruguay and Kazakhstan anyway. Nice trade Heli-Ben.

My immediate term support and resistance lines for the SP500 are now 1262 and 1284, respectively.

Trade inflation and roll the bones out there today,

KM

Keith R. McCullough

Chief Executive Officer