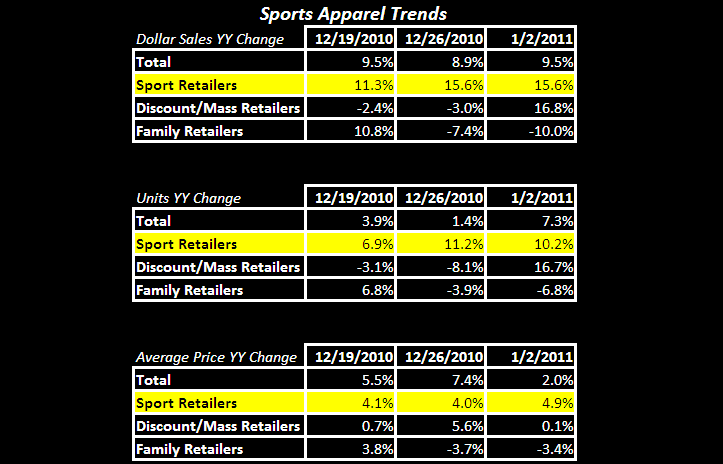

This morning’s athletic apparel data provides the latest read-through of how the end of December played out and just how significant the impact was from the blizzard at month’s end – the bottom-line, it was more of a snowball than a snow bank.

With this week’s numbers in, we have our first look at the impact of the storm in aggregate at least through the lens of sports apparel sales, which were up sequentially over the past 2-weeks both on a YY and Trailing 3-week basis. Recall that last week’s athletic apparel data included sales through Saturday, while the footwear data did not – Saturday through Tuesday’s sales will be released later this morning.

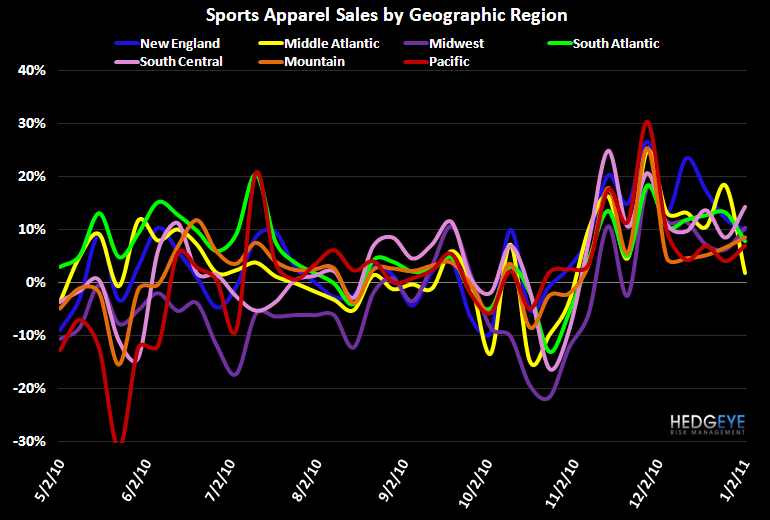

Looked at on a regional basis, it’s no surprise to see sales down sequentially in both New England and the Mid Atlantic, but importantly neither turned negative on a year-over-year basis. In fact New England was up 9.9%. An update on brand performance and footwear sales to follow…

Casey Flavin

Director