Great quarter. We still like it and have numbers that are 15-20% ahead of the Street. But a legitimate bear case arose from the quarter. We won’t ignore its existence. But rather will monitor it and point to entry/exit points on a high conviction name.

I’ve had one big multi-stage reaction to Nike’s print.

1) Upper. Better than expected print. Nike prints $0.94 vs the Street at $0.88. We were at $0.96, but the differential was largely below the line and SG&A. Clean profit algorithm of 9.9% revenue growth, and levers it to 12% Gross Profit growth, and 24% EPS growth, respectively. North American futures accelerated AGAIN to 16%. Slight weakness in other regions on the margins, but more than made up in the US. Remember what Nike’s stock did 13 weeks ago when US Futures went to 14%?

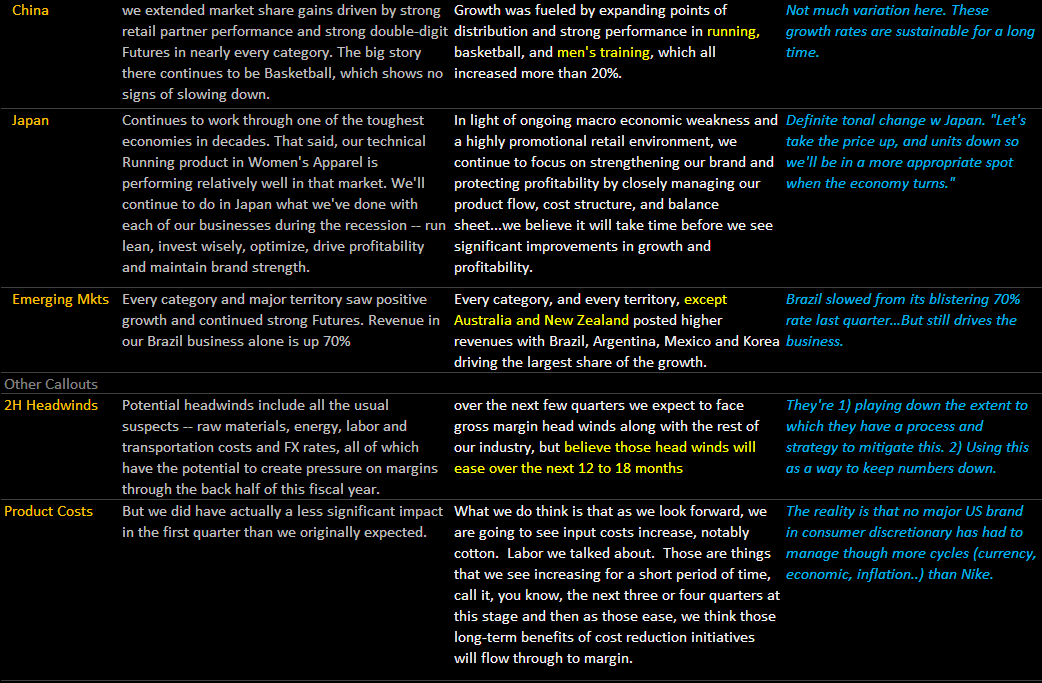

2) Downer: On the flip side, as we outlined in our preview ("NKE: It's All on Nike U.S." posted 12/21) the set-up for Europe and parts of Asia is not a good one heading into ’11. Check out that note to see changes in consumer confidence, retail sales metrics, and GDP trends on the margin. Nike appears to be tracking those broader consumer trends to some degree with Western Europe, Eastern/Central Europe and China all decelerating on the margin by 300-500 basis points. Interestingly, while China decelerated, Japan turned up. Given that Japan has been a disaster for almost everyone in retail for years, this is a bit of good news. But there have been many many head fakes, and given the lack of growth in the economy in Japan, it will take well more than a quarter to establish a trend.

3) Reality. The reality is that this company has proven time and time again that when one part of the portfolio ebbs, another will flow. That’s exactly what we have today. The difference is that in yesteryears, it was always Europe, Asia and The Americas that offset lackluster growth in the US. Today we have the US growing at a blistering pace, and offsetting any weakness in other regions. This throws a powerful ‘what if’ into the equation.

What If???? The risk with where Nike stands today is that the US business needs to stay strong – else any weakness in Europe, Asia and Americas will be more transparent and even perhaps problematic. Remember, we have to start to deal with World Cup hangover in another two quarters. The good news is that the US business is at the very start of a major R&D/product cycle that should last well into 2012. Our confidence level there remains very high, as outlined in our past research. Also Nike has a lot in its back pocket to mitigate gross margin pressure in its business from raw material cost inflation.

But regardless of what we think, a bear call exists, and it sounds something like this…”This company has been a solid global top line and gross margin improvement story, but now key regions have shown weakness on the margin. Inventories have built on the margin. In F3Q (Feb) we will be feeling the effects of the ‘Consumption Cannonball’ where real consumption turns negative. Immediately thereafter Nike – and the whole industry – will have to comp World Cup. Yes, Nike has the balance sheet to buy stock on weakness, and also has recently stepped up acquisition strategy. But a story that morphs from a ‘robust top line and GM% improvement story’ into a ‘top line/acquisition and SG&A leverage story w stock repo as a kicker’ is not enough to keep its multiple in check.

With short interest near historic lows, and the sell-side universally bullish on this name, it is not a major surprise that the stock is down today.

But all that said – we’re coming out at $1.25 for 3Q, and our sense is that the Street ultimately shakes out closer to a buck. Same order of magnitude for the FY11 and FY12.

The bottom line is that we may be entering a period where Nike’s volatility kicks up a couple of notches, which we think will be a potentially good opportunity for those who have been telling us that they ‘missed it.’