NKE will come through, again. 10% beat likely without futures rolling. Look for a major relaunch of Free. But given interconnected global risk, low short interest, key management stock sales, and the best sell-side sentiment since October ’08 (14 Buys and no Sells) Nike NEEDS the US to lead. The good news is that it is.

On some level, I think that NKE planned its May Fiscal Year just so they could keep shareholders walking on eggshells during holiday weak in addition to 2Q EPS. The eggshells aren’t warranted this time around.

1) We’ve got Nike printing $0.96 in our model, which is 10% greater than the Street at $0.88. Importantly, this EPS algorithm starts with 10% sales growth levering to 28% in EPS growth; showing improvement in both Gross and SG&A simultaneously for the first time since 2Q08.

2) It would be very uncharacteristic of Nike to change guidance at this time of the year. The caveat is that if they smoke the quarter (our estimates count as at least a puff or two) Don Blair has all the ammo he needs to keep forward hurdles low; raw material costs, more air freight to keep up with strong demand, quadrupling in apparel R&D budget, to name a few.

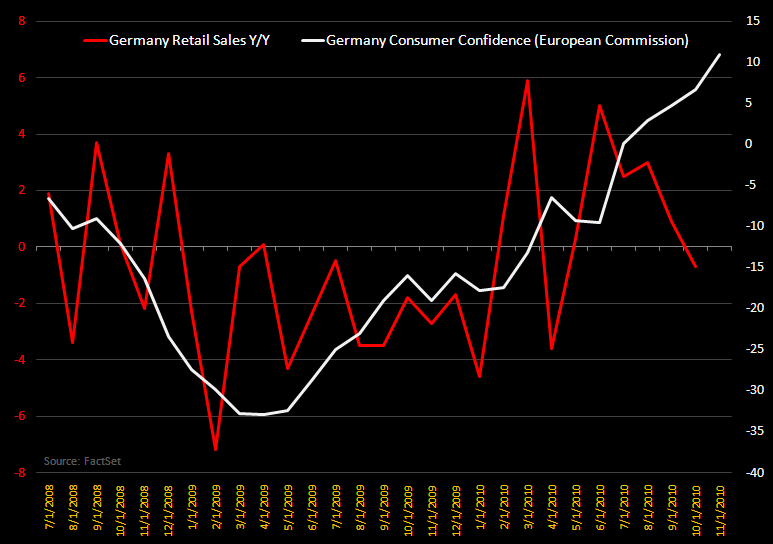

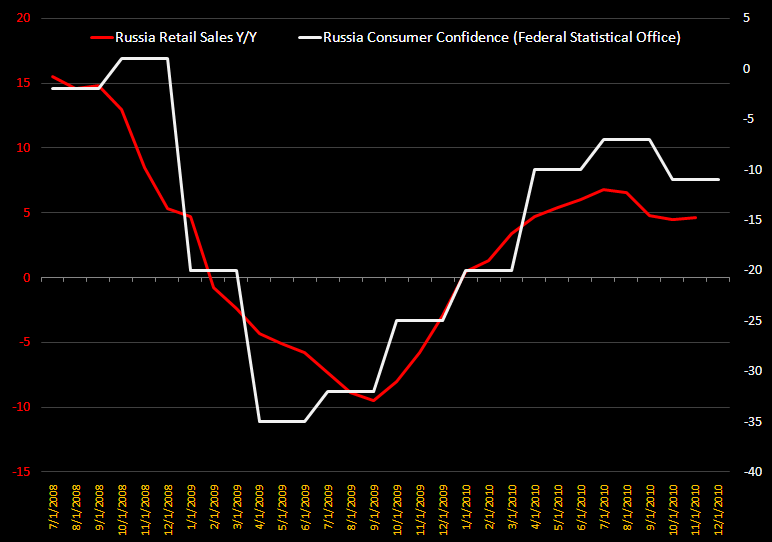

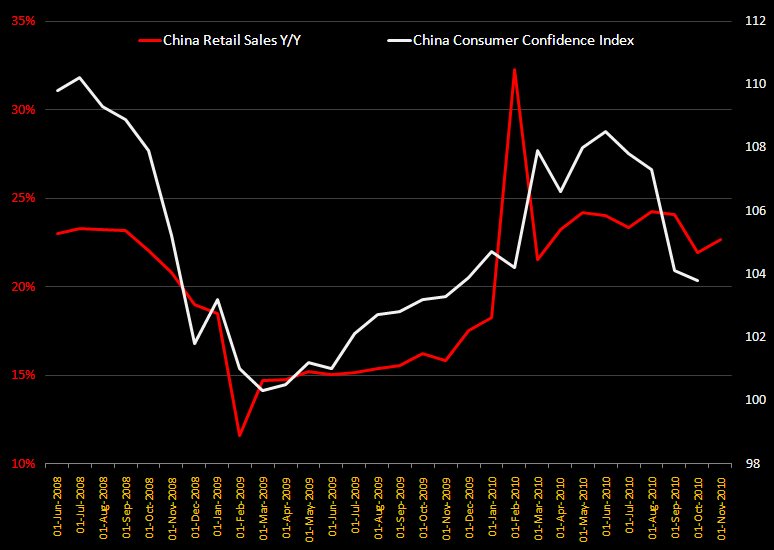

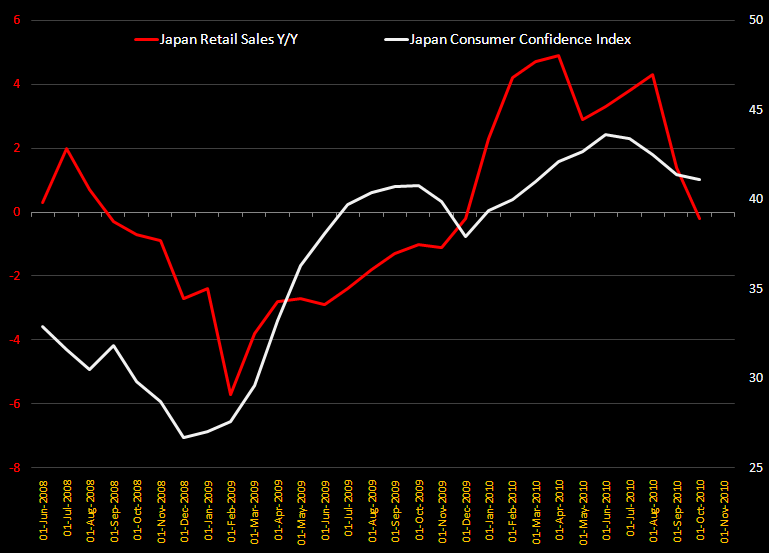

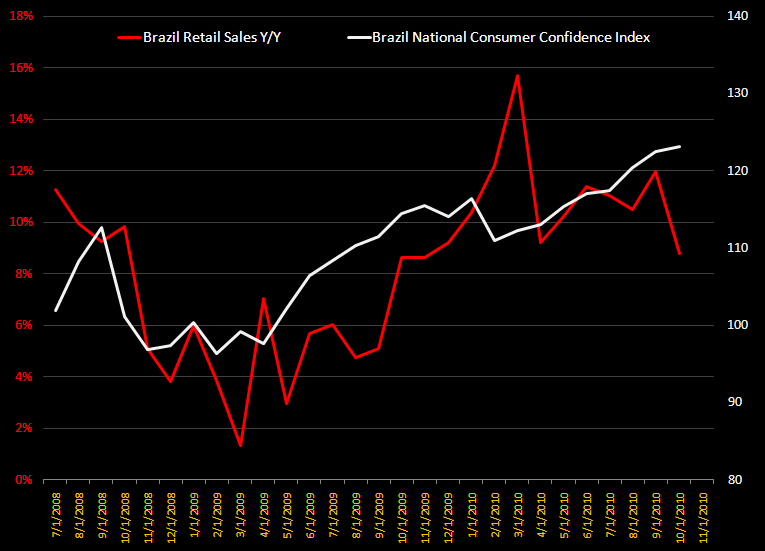

3) Sustainability of Futures. The biggest question for everyone that cares about Nike – or anyone that even grazes some part of Nike’s supply chain – is whether or not Nike can sustain its North American growth. While this is usually not on the top of our list given how broad Nike’s portfolio has become. But let’s face some facts…the setup in Europe and Asia is not setting up to be pretty into 2011. Check out the charts below where you’ll find eroding consumer confidence pretty much everywhere. The US actually looks good by comparison. In other words… for one of the first times in years, Nike ABSOLUTELY needs the US to hold on tight.

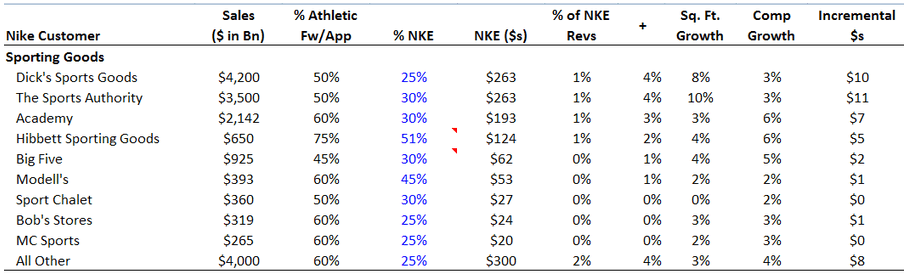

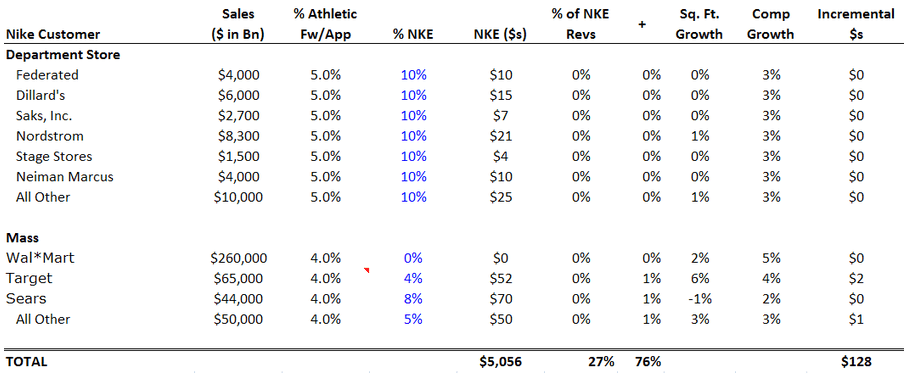

Given the importance of North America, let’s dissect the 14% futures number we saw last quarter. 14% growth over the next 2 quarters is the equivalent of adding $289mm in new business (assuming that 85% of the base is on the Futures program). This number annualized is bigger than the ENTIRE US BUSINESS for over 90% of the footwear brands in the world. The good news is that the number is balanced over footwear and apparel. That definitely makes this number more easily digestible.

Precise quantification of this order number is tough. But here’s our best crack. When we add up comp and square footage growth by customer and by channel, we get to about $128m top line growth for the YEAR – or about 2.5%. Now…this excludes growth in Nike retail and Nike.com – both of which should take the aggregate growth rate on a reported basis for Nike up by another 2-3 points. So what we need is to justify doubling this growth rate again due to market share gains in order to get to 14%.

This is very much realistic. But here are a few considerations.

1) Free: I think that Nike has done an admirable job in hiding from the outside world how bothered they are by missing out on the Toning category. That’s not to say that they want to have been first to market with a ‘tush toner’. But does anyone remember Nike Free? This is a technology that Nike debuted around 2005 – the same time that Adidas bought Reebok and immediately started to seed share to Nike (their combined share went from 17% to 6%).

So what are we left with? The toning category has taken off, the book “Born to Run” was on the NYT best sellers list. (This focused on a group of hardcore runners and Mexican tribes who would run (often barefoot) as a way to minimize injury and maximize speed and safety.) And all the while, Nike is left out in the cold even though they invented the technology to lead this category.

Translation = the tools, molds and other capital equipment to produce these shoes en masse have already been amortized. My sense therein is that we’re going to see a MAJOR re-launch of ‘Free’.

This should be showing up in Futures today. (and we probably saw some last qtr).

2) Endorsements: Yes, we’re in a solid R&D cycle. But with that comes an Athlete Endorsement. We already saw Nike outbid for the NFL contract. It dropped Tom Brady, who was then picked up by UA. It also goes down the curve to athletes like Allyson Felix, who Nike recently took from Adidas. To those that don’t know, Felix is one of the top sprinters in the world and is a solid brand statement (recently had a full billboard in Times Square).

3) Global Interconnected Risk: Not that many people ask me about the Macro side of Nike. But they should. While being the clear leader in a Global Duopoly with a fixed structural forex and sourcing advantage, the company is not immune to global turmoil. They have bucked it in the past – but we cannot give a free pass – even for a company like Nike.

4) Model Shift: We’ve been looking at Nike as a sheer top line growth story with improving Gross Margins. As we anniversary World Cup, the top line will still be there, though margins should be driven more by SG&A and FX hedges. Same result, but different path. The risk is whether Mr. Market will give the stock the same multiple in trading GM for SG&A/FX.

Europe (Western): Largely stronger on a sequential basis

- Most significant consumer confidence ramp with four consecutive months of positive retail sales - the longest such streak in more than 5-years before turning slightly negative in October.

Europe (Eastern/Central):

- Russia rolling over slightly relatively to Q1

Key issues/events across Europe:

- Consumer Pullback from Austerity measures issued or discussed, many enacted for Jan. 1, 2011

- Austerity measures in Ireland, UK, Spain, Portugal, Italy, France, Greece, Hungary, Romania

- World Cup spill over early into the qtr

Euro - GDP:

China: Retail sales growth stable in low 20s while confidence is beginning to roll

Japan: Rolling over hard relative to Q1

- stimulus measures and policy changes helped buoy the Japanese consumer in 3Q10, including a subsidy for energy-efficient cars and a tobacco tax hike scheduled for October 1st. Both programs pulled forward consumer demand to the tune of a 0.7 point contribution to 3Q10 GDP, after having no contribution from private consumption in 2Q10. In addition, Japan’s hottest summer in over a century fueled demand for cooling products. These tailwinds helped boost 3Q10 GDP growth to +3.9% QoQ SAAR and their absence will create a drag on growth in 4Q10 and potentially into 1Q11 – just around the time bearish 4Q10 economic data is being reported in globally. (11/30/10 Macro post )

South America:

- Brazil - retail sales started to slow heading into Nov though relatively flat with Q1

Fx: Nearly 1% drag on top-line in Q2