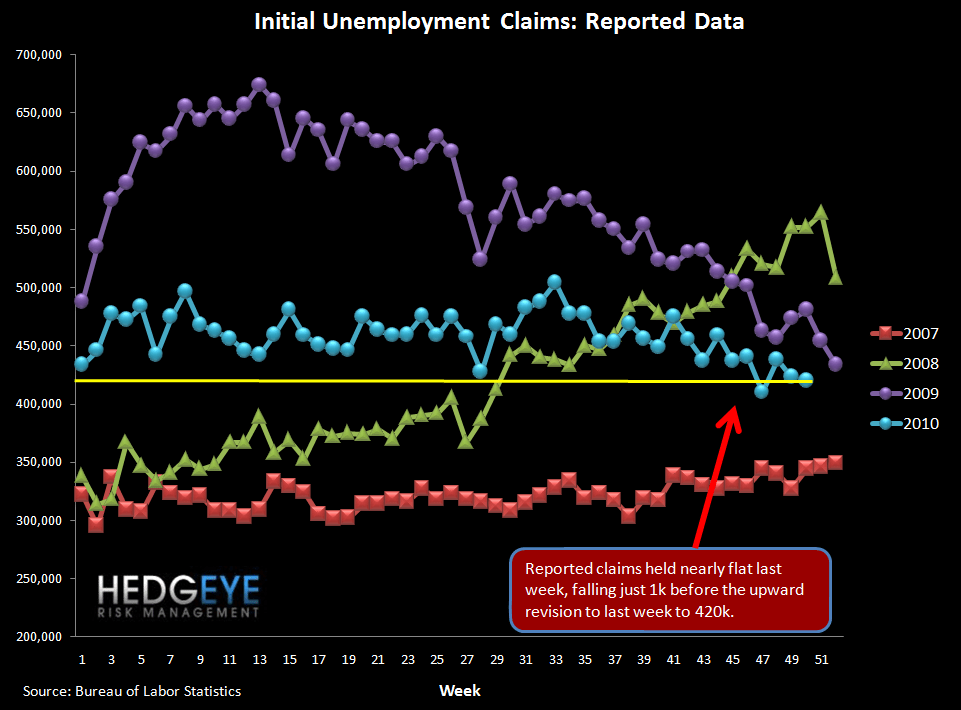

Initial Claims Fall 1k Before Revision

The headline initial claims number fell 1k (3k after the revision) this week to 420k. Rolling claims fell to 422.75k, 5.25k lower than the previous week and a new YTD low. We continue to remind investors that the unemployment rate won't improve until we see claims move into the 375-400k range - this is based on our analysis of past cycles. That said, it is worth highlighting an important caveat. This recession has been different in that it has pushed the labor force participation rate down by ~200 bps, which has had a correspondingly positive improvement on the unemployment rate. In other words, the unemployment rate isn't really 9.8%, it's 11.8%. So when we say that claims of 375-400k will start to bring down the unemployment rate, we are actually referring to the 11.8% actual rate as opposed to the 9.8% reported rate. Today's data is a tiny step in the right direction.

Yield Curve Continues to Widen Rapidly

We chart the 2-10 spread as a proxy for NIM. The 2-10 spread has recently expanded sharply, expanding 44 bps in the last two weeks alone and 78 bps since the beginning of the quarter. Yesterday’s closing value of 287 bps is up from 262 bps last week.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur