Position: Long Germany (EWG); Short Euro (FXE), Short Italy (EWI), Short Spain (EWP)

Italians are calling tomorrow B-Day, where ‘B’ is for Berlusconi, when Prime Minister Silvio Berlusconi faces a no-confidence vote that could swing on just one or two votes. In remarks today Berlusconi seemed to issue an ultimatum: either vote for him or else the country will be sent spiraling into the Eurozone debt crisis.

The 74-year old Berlusconi, whose center-right People of Freedom party is expected to win a vote of confidence in the upper house, but is more vulnerable in the lower house, has stood in a perilous state since July when followers of his former deputy, Gianfranco Fini, left the governing majority to set up a parliamentary group of their own.

We’ve had the opportunity to write about Berlusconi this year due to his numerous “scandals” and the risky state of Italian finances with the Eurozone’s largest public debt, at ~120% of GDP. We’ve presented Italy’s Crisis in Confidence as one not unique to Italy alone, but many EU states such as Greece, Ireland, Portugal, Spain, and Hungary that have mismanaged and overextended their public balance sheets.

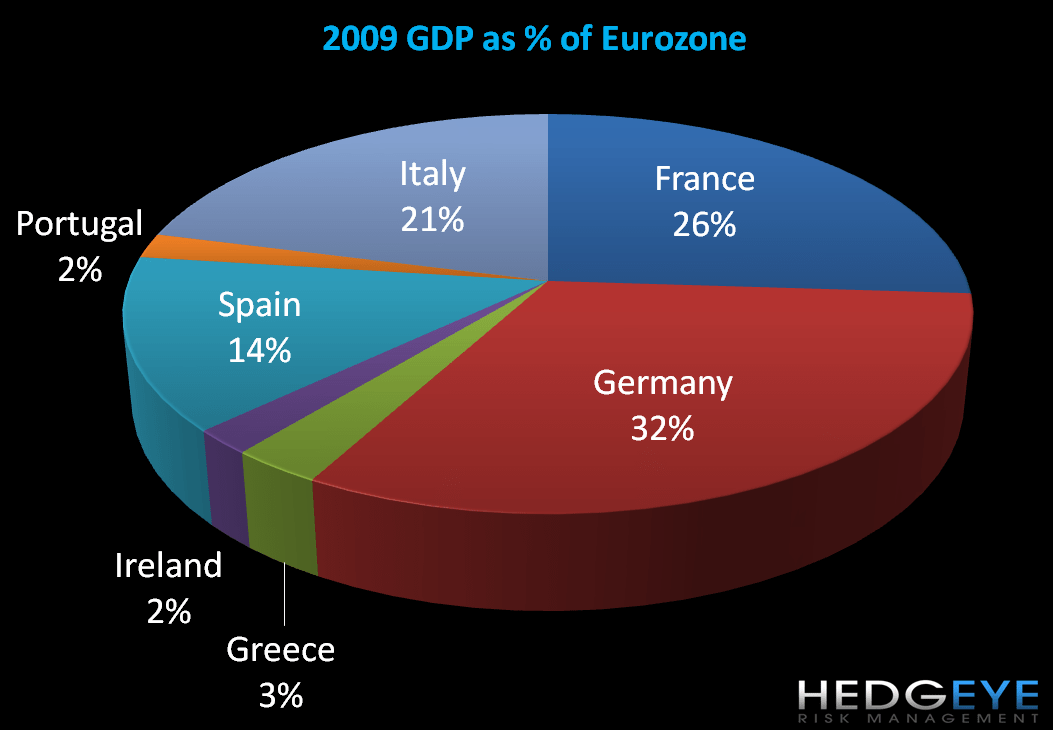

However, here we must stress that Italy is a much larger “fish” than its European peers who have already been forced to receive bailouts from the EU/IMF, both in terms of size of the economy and debt outstanding (see chart). We’ll be managing risk around a scenario in 2011 in which Italy may too need funding assistance to prevent a default. Both a rising yield premium (see chart below) to own Italy’s debt and underperformance of its equity market this year have been signaling a heightening risk trade.

Investment risk in Italy revolves around the confluence of these macro factors:

1.) Public Debt – the country is rolling up against €500 Billion of government debt maturities (principal +interest) over the next three years--a level equivalent to Germany’s obligations, yet from an economy 1.6x larger than Italy’s. As the chart below shows, a major headwind comes in 2011, ~ €350 Billion.

2.) Political Uncertainty – government instability begets investor uncertainty and unleashes the snowball of investor fear that runs government yields higher. We’ve already seen this film in Greece and Ireland this year.

3.) Austerity’s Blues – We continue to see strong foot power (strikes) against the government’s proposed €30 Billion in austerity cuts.

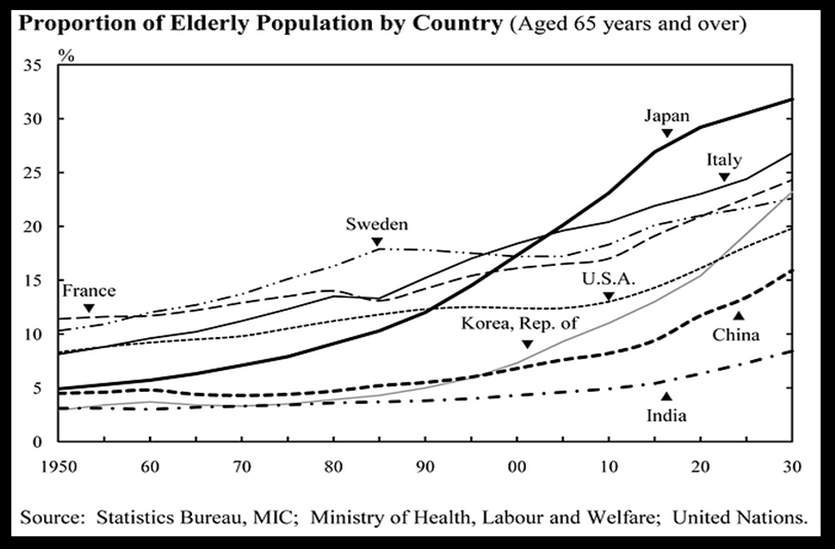

4.) Aging Population – Italy will have the oldest population by 2015 and 2020 in the Eurozone, with a population >65 at 21.9% and 23.2%, respectively (see chart).

In remarks today Berlusconi noted that he is seeking to form a new government supported by “all moderates” if he wins the confidence vote. Unfortunately, should Berlusconi win, his majority may still be so small that he simply prolongs Italy’s Crisis in Confidence.

Suffice it to say, we’re forecasting rocky waters for Italy in 2011. Look to meetings this Thursday and Friday at the European Summit in which discussions will include new mechanisms to deal with Europe’s sovereign debt problems.

Matthew Hedrick

Analyst