For now, if the stock market is your gauge, Bernanke is seeing some success. There are many other real time markets (commodities, global growth) that show a disconnect from U.S. equities. The most recent consumer data point indicates that the consumer is feeling better. I’m less-than-convinced that this will be sustainable or that Ben Bernanke has discovered any lasting solution to the problems facing the U.S. economy.

The following are some current positives in consumerland:

1. Income growth is getting better

2. Job growth is still stagnating but trends are better that they were in January

3. Retail sales are hanging in

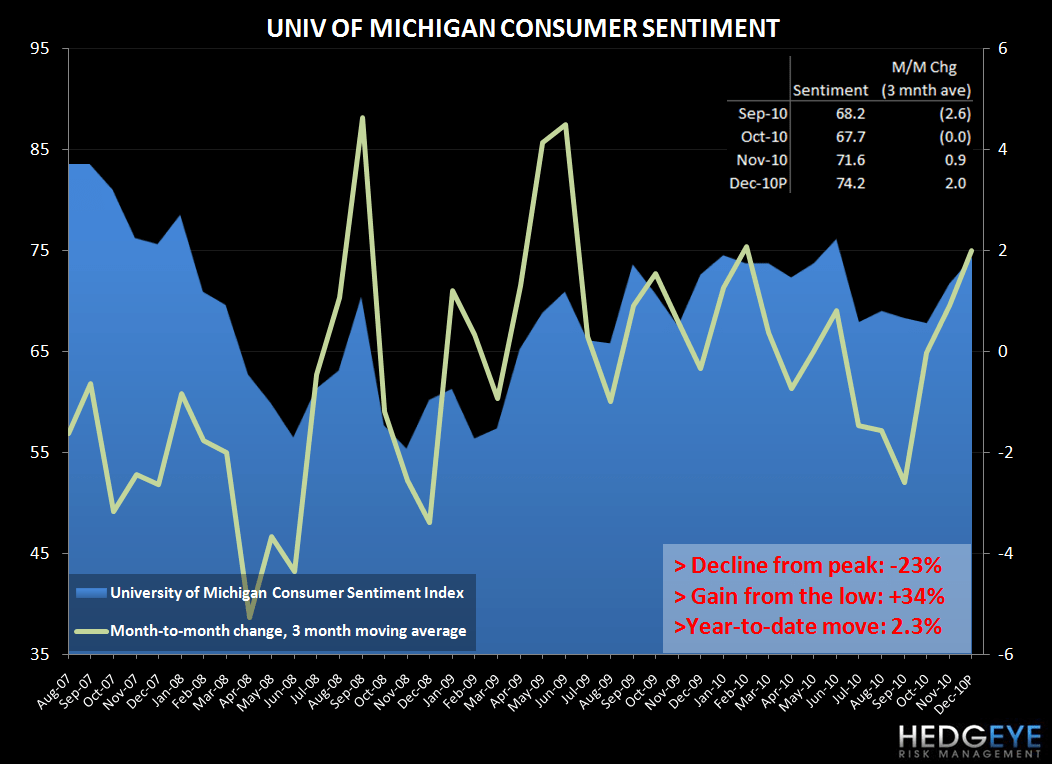

4. Consumer sentiment improved 5.7% and 3.6% sequentially in November and December, respectively.

5. The Consumer discretionary index (XLY) is up 25% YTD

6. The S&P 500 up 8.76% and 3.69% September and October, respectively and is up 4.4% so far in December.

The University of Michigan consumer confidence reading rose to the highest level in six months, but is still registering a lower high; index of consumer sentiment rose to 74.2 from 71.6 at the end of November. The Bloomberg consensus was for a reading of 72.5.

The bullish consumer sentiment is not being confirmed by the more weekly ABC consumer comfort index which is at a -45, up from the low of -54 set on 12/01/08. Year-to-date the consumer sentiment index is only up 2.3%, with the expectations component down 3%, while the current conditions is up 10%.

The consumer is clearly responding to diminishing levels of uncertainty as corporate profits have improved to the best level since 2007. We are reminded that not every this is turning up roses and part of the improvement increased profits is due to better efficiencies thru lower labor costs. Just today TJX closing down the A.J. Wright division and cutting 4,400 jobs; other notable companies recently announcing layoffs in the past 30 days are the Washington Post, Express Scripts, State Street VF Corp and Apollo Group Inc.

The current trends in consumer sentiment as measured by the University Michigan are critical and continued improvements are needed to sustain the bullish sentiment running thru the market.

1. The Bullish to Bearish spread for the AAII sentiment index is approaching the danger zone again at 30.5.

2. The VIX is down 48.9% over the past six months and is now down 20.99% year-to-date; another shoe dropping could see the VIX busting a serious move to the upside.

If the politicians in Washington come to some sort of compromise from the expiring Bush income tax cuts, it’s net neutral for the economy and will not likely benefit consumption. At some time austerity will need to become a part of the conversation and a cursory glance at the television and how that is going down in Europe shows you what the consumer is going to think about that. The continuation of the unemployment benefits helps buttress consumption. I have described this before in the context of extended and emergency benefits. Allowing them to expire would essentially sweep the legs from under a large portion of consumers and, whether or not one believes that this is good policy, it would initially be a negative for consumer spending and the broader U.S. economy.

On the plus-side for consumers, the one year's elimination of two percentage points in the Social Security withholding tax will directly boost disposable income of individuals currently paying those taxes. As a result, there should be some consumption pick-up, but it is “one time” in nature and, just like the stimulus package, the impact will only be short lived.

As the facts change, we can adapt to the new trends. For now we are sticking to our Consumer Cannonball theme (albeit on a different duration), as some of the major pillars of that thesis have not changed; primarily the outlook for housing and the labor market in 2011. I will expound upon this point in a post next week.

Howard Penney

Managing Director