Position: Long Germany (EWG); Short Euro (FXE), Short Italy (EWI), Short Spain (EWP)

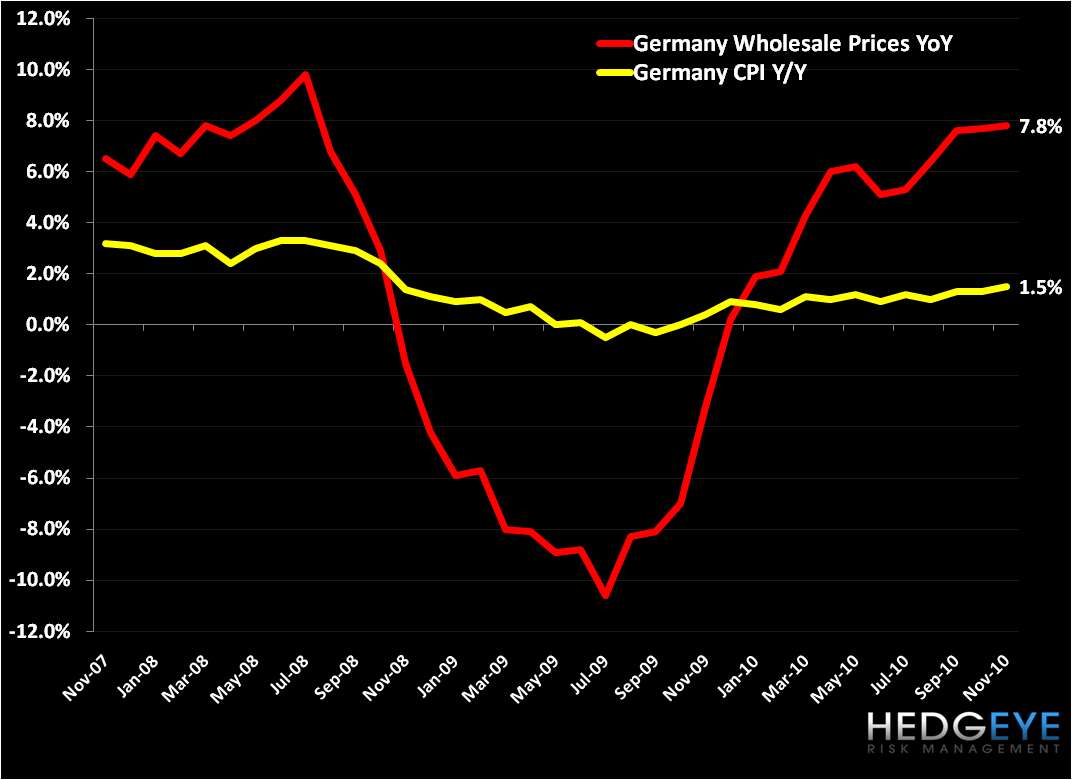

We continue to point out in our macro research that we see global inflation accelerating. Below we show charts of the German Wholesale Prices Index that registered +7.8% in November year-over-year and the UK Producer Price Index that rose +3.9% in November year-over-year (see charts below).

Points to consider:

- We’d expect increases in wholesale and producer prices to be "pushed" to the consumer = bearish for consumer.

- While UK PPI is sequentially lower, the elevated level will put addition pressure on the BOE to address headline inflation that has stood above its target rate for the last 8 months.

- The UK Statistical Report noted that the rise in PPI mainly reflected price rises in petroleum products (including duty), food products and computer, electrical and optical products.

- The German Wholesale Price Index is making higher highs despite more difficult annual comps.

- The weakness in the EUR-USD in Q2 of this year should encourage inflationary pressures on the comp beginning in 2Q11 (see chart below).

As Keith pointed out in the Early Look this morning, the price of everyday consumer goods (commodities) have signaled huge inflationary gains over the last three months, despite the highly politicized and manipulated US CPI figure that stands at a mere +1.2% in October year-over-year. In case you missed it, here’s a look at these price moves.

- Crude Oil = +18.2%

- Natural Gas = +20.8%

- Heating Oil = +18.2%

- Gold = +10.1%

- Silver = +41.2%

- Palladium = +38.3%

- Copper = +17.3%

- Cocoa = +12.3%

- Cotton = +52.4%

- Lumber = +19.8%

- Orange Juice = +16.5%

- Sugar = +35.5%

- Corn = +24.2%

- Oats = +27.9%

- Rice = +20.5%

- Soybeans = +23.6%

- Wheat = +10.3%

Suffice it to say, inflation is showing up in Europe. For the major economies on the continent, we believe the most current “threat” of inflation, which needs to be addressed, is in the UK. That said, Eurozone countries should begin seeing higher inflation, especially if our bullish intermediate term call on oil is correct, and as comps from a weaker EUR show up beginning in 2Q11.

Matthew Hedrick

Analyst