Initial Claims Fall 15k ... Consistent with late-2009 trends

The headline initial claims number fell 15k (17k after the revision) last week to 421k. Rolling claims fell to 427.5k, 4k lower than the previous week and a new YTD low, but the reported series moved off of the lows significantly. We continue to remind investors that the unemployment rate won't improve until we see claims move into the 375-400k range - this is based on our analysis of past cycles. That said, it is worth highlighting an important caveat. This recession has been different in that it has pushed the labor force participation rate down by ~200 bps, which has had a correspondingly positive improvement on the unemployment rate. In other words, the unemployment rate isn't really 9.5%, it's 11.5%. So when we say that claims of 375-400k will start to bring down the unemployment rate, we are actually referring to the 11.5% actual rate as opposed to the 9.5% reported rate. Regardless, today's data is positive.

Another Positive for Financials .... the Yield Curve Steepens

We track the 2-10 spread as a proxy for industry NIM. The 2-10 spread has expanded sharply in the last few weeks, expanding 19 bps in the last week alone. Yesterday’s closing value of 262 bps is up from 243 bps last week. More to the point, the sequential change from 3Q10 to 4Q10 is now up 11 bps to 2.25% from 2.14%.

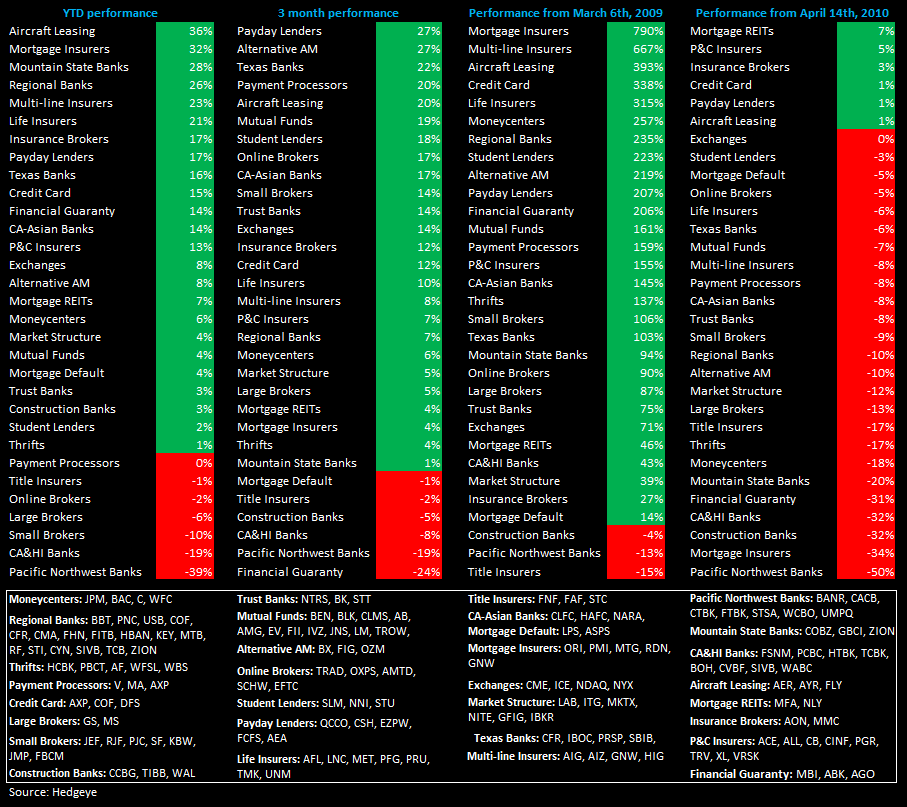

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur