|

Long: AMN, PLBY, PSA, FWONK, ROK, AMH, RH, VLVLY, BYD, PENN, CUBE, TOST, BROS, DUFRY Short: PLUG, RRGB, SJM, SFIX, SFM, KR |

Below are updates on our twenty current high-conviction long and short ideas. We will send a separate email with Hedgeye CEO Keith McCullough's refreshed levels for each ticker.

AMN

|

Long Thesis Overview: We expect prolonged wage inflation across the US Medical Economy as a result of widespread provider burnout and medical consumption pent-up demand remains significant for many types of care. We expect these trends to continue to benefit hospital staffing company AMN Healthcare (AMN). |

Earlier this week, AMN Healthcare (AMN) saw a sell-off after reaching an all-time high of $123.41 per share. Despite the negative price action, we have not seen any fundamental reasoning for the selloff but will point out that the most recent MicroQuad update has placed AMN in MicroQuad4, which is often an indication to sell or short the name. With this landscape in mind, as well as the considerable success AMN has experienced, we are not making a change in our positioning this week.

Additionally, the trend of strikes over pay and working conditions for health care workers hit Kaiser Permanente earlier this week as 24,000 workers in California and Oregon endorsed the work stoppage by an overwhelming margin in the weekend vote. With this in mind, AMN and other temporary/contingent staffing companies remain well positioned to capitalize on persistent labor market trends should they not find themselves in a shortage situation as well.

As the most recent wave of COVID-19 caused by the Delta Variant fades, we believe AMN will continue to be successful providing staffing across the country where needed. The company often experiences a boost during the flu season and should again experience this trend.

Nonetheless, we will continue monitoring our proprietary Job Postings Trackers and update subscribers on any future changes in positioning. We remain Long AMN Healthcare on the Hedgeye Healthcare Position Monitor.

PLBY

|

Long Thesis Overview: We think that the upside here is simply massive. 10-bagger over TAIL duration. Ideas like this come along once every few years. I know that it’s too thinly traded now for a lot of institutions to get involved, but that dynamic should change dramatically over the next 1-3 years while the P&L, Cash Flow, Balance Sheet and float characteristics catapult themselves worlds head of the consensus. |

While Playboy has many avenues for strong and accelerated growth, one specific avenue is the company’s presence in India. PLBY has very directly called out India as an important international growth market for the company and has already signed a JV to bring PLBY branded apparel to the market, but now is expanding its I-Gaming footprint in the country.

PLBY has partnered with software platform provider Gaming Technologies, owner of Mexico based online casino brand Vale, for a partnership to bring a real-money mobile Rummy game to the Indian market which is expected to launch later in 2021.

On top of that Playboy is also bringing a hospitality venture to India with its first venue expected to open in December. This company just has so many ways to win.

PSA

|

Long Thesis Overview: We can keep this short - all that really matters for Best Idea Long PSA is that the company inaugurated FY21 FFO guidance with full ranges for all the key drivers (SSRev, SSExp, SSNOI, Development, Acquisitions, etc). Not only does this bring PSA up to par with the other four peers in the space, but it signals management's ongoing commitment to address long-time shareholder gripes regarding engagement with the street, governance, capital deployment, balance sheet efficiency, etc. All of these items are core to the long thesis for accelerating earnings growth and a positive re-rating of the stock. |

There are several rumors making the rounds that PSA could be a player on one of several large self-storage portfolios currently on the market, including potentially Manhattan Mini Storage although we find that one relatively unlikely.

Participating in any of these transactions would fit with our long thesis, as PSA has the balance sheet capacity to opportunistically take up leverage and improve its external growth profile. For 3Q21 results, we will be watching for the degree of seasonal same store occupancy contraction/normalization, and whether that could work to inflect the RoC looking ahead to FY22.

FWONK

|

Long Thesis Overview: In 2020, F1 reached a new Concorde agreement for the 2021-2025 seasons that will meaningfully improve the economics of a race. Liberty has also focused on entering more attractive, long-term race deals like the Vietnam and Miami Grand Prix agreements. We believe there is more grease on the wheels. Liberty can maximize its efforts to increase interest in the sport, continue to go after underpenetrated markets, and use its SVOD service to capitalize on its content more efficiently. The most significant area of improvement for F1 is their sponsorship and partner agreements. We believe there is ample opportunity in sponsorship with only 17 races out of the record-breaking 23 race calendar having a title sponsor and F1 lacking many low-hanging partnerships such as fuel and hospitality providers. |

The Turkish G.P. was a rather dreary affair, with on and off rain throughout Qualifying and the Race. Qualifying saw all teams using the intermediate tire, as the conditions were borderline between full wets and slicks. The result would be a Mercedes one-two with Hamilton taking pole and Bottas claiming second, Red Bull's Max Verstappen rounded off the top three. However, an engine swap for Hamilton, and the ten-place grid penalty that accompanies it, would see the starting grid for the race be Bottas, Verstappen, and Ferrari's Charles Leclerc claiming third position for the race start.

The race saw all teams using intermediate tires, as the drizzly conditions persisted throughout the race. This created a strategic problem for many teams as they had to decide whether or not new tires would provide an on-track advantage. Delayed switches to fresh tires late in the race saw both Hamilton and Leclerc lose the opportunity for top-three finishes. However, mid-race tire swaps worked for some drivers, with Mercedes's Bottas taking the win and Red Bull's Verstappen and Perez claiming second and third. The battle for first place in the Driver's Championship now stands at eight points, with Verstappen leading Hamilton into next week's U.S. G.P. in Austin, Texas.

U.S. viewership for the Turkish G.P. came in at 716k (up 63% YoY), the average viewership for the season now stands at 883k, up 54% YoY. We expect the next two races, U.S. (October 24th) and Mexico G.P. (November 7th), to be highly watched as they are typically the most viewed races behind Monaco.

ROK

|

Long Thesis Overview: We expect this to be an unusually good cycle for ROK as developed market automation investment benefits from less ‘offshoring’ of production amid higher emerging market labor costs and other considerations. The capabilities for automation technologies, from machine vision to software to 5G and the like, broaden the market opportunity substantially. Despite being one of the best businesses in our coverage, shares of ROK don’t yet sport the premium valuation we’d expect them to receive as organic growth accelerates through 2H21. |

The shift of production to China has been a key headwind to factory automation spending in more developed markets. But now tensions with China, scarce labor, supply chain bottlenecks, cost input pressures, and rising wages favor have increased automation investment by manufacturers.

Record capital raises in this cycle have been unusually focused on several capital-intensive niches, like electric vehicles, often going to build ROK outfitted factories. In a few years, we suspect it will have been obvious that Rockwell – the company that builds the machines that make the machines – was well positioned to increase revenues and margins.

AMH

|

Long Thesis Overview: On balance, we see the data as very supportive of the long-term SFR long thesis in general, but in particular AMH with its captive "bank" of lot inventory and unique development program set against an extremely tight supply environment. As the space matures and grows more competitive given the outsized yield opportunities, operators with pre-sourced inventory to control, build and deliver have a massive advantage. |

Best Idea Long AMH will be reporting its 3Q21 results after the market closes on November 4th. We are actually in-line with consensus on Core FFO of $0.34/share for the quarter, but think there is potential bias to the upside on those numbers.

We expect average realized rental rate growth to accelerate to +6% in 3Q from +4.1% in 2Q, followed by further acceleration to over +7% in 4Q driven by blended leasing spreads approaching the double-digit range. AMH will provide its FY21 outlook early next year, and it is highly likely that there is further acceleration in SSNOI growth from the mid-to-high +7% range in FY21.

RH

|

Long Thesis Overview: as the company is going to have to show success in opening up new countries to prove the top line consistency and momentum, and that will take 2-3 years. But we’re been here for the ride since $28 – and this ride is far from over. There’s no better ‘buy the dips’ name I can find in retail than RH. This team’s strategy is going to make long-term shareholders a lot of money. |

Listening to RH’s last earnings call, the thing that we were not expecting was commentary that 3Q-to-date is accelerating off 2Q levels. Clearly demand in this segment of the market is far from cooling.

People are finally starting to ‘get’ the story over a shorter-term basis, but on the other hand few – if any – are correct in modeling what this company cranks out in years 3-5. How we’re doing the math, by year 5 of the model we’re at between $7.5bn and $8bn in revenue at a 25% EBIT margin. That gets us to $50 per share in earnings. The Street is at $32 in Year 5. We could easily argue that this is worth 40x-50x earnings given the characteristics noted above. That suggests a $2,000-$2,500 stock in five years.

VLVLY

|

Long Thesis Overview: Shares of Volvo Group (VLVLY) have lagged other machinery-oriented names despite favorable industry and company specific factors. Trucking conditions in Volvo’s key markets remain extremely tight, while labor conditions may ease in coming months. Construction equipment demand in developed markets should remain reasonably robust, a view supported by fleet demographics, COVID recovery stimulus, elevated commodity prices, and aging infrastructure. We see greater than 50% relative upside for shares of Volvo as robust demand intersects with stronger 2022 pricing. |

Volvo, which makes commercial trucks, buses, and construction equipment, has several similar tailwinds as PCAR. However, we continue to expect robust demand for construction equipment in coming years amid aging fleet…at least outside of China.

Volvo has a greater exposure to Europe, a region with a favorable macro set-up into than most regions. Volvo likely offers attractive upside, with shares trading near the lowest valuation relative to public peers in recent years.

BYD

|

Long Thesis Overview: BYD looks like one of the most undervalued stocks in our universe, when measured vs its true potential. We get it, stock is up vs pre-Covid, but the numbers have justified most of the move higher. And yet, they continue to go even higher. There’s also a case to be made that BYD is deserving of structurally higher multiples given the inherent organic growth in its markets (especially LV Locals), and higher flow through, but also for the fact that the negative secular theses have pretty much been dispelled. Do we need to make the case for higher multiples right now? No, with the stock off its highs and numbers way too low, we have plenty of valuation support in our SOTP analysis. |

Similar to PENN, BYD is benefiting from strong growth in the regional markets. LA is the biggest wild card on September GGR (and a big market for BYD) given the disruption from Hurricane Ida, but on a per day basis, we think trends should look decent and help investors look past the near-term disruption.

In addition to the traditional “regional markets”, we remain bullish on the Las Vegas locals’ market with BYD benefiting from the market’s robust fundamentals and holding a ~30% exposure there. BYD remains a Best Idea Long at Hedgeye.

PENN

|

Long Thesis Overview: (per Hedgeye GLL analyst Todd Jordan) "I would own Penn National (PENN). It’s had a great management team historically, which is critical for a buy & hold play. The Barstool move was very astute on their part. I have a pretty good idea what Barstool would be worth as a standalone company, and we know what Penn’s option to buy it at is; there’s a huge divergence, they can buy Barstool for far cheaper than it’s truly worth. The initial chunk they bought was at a very low price too.” |

PENN remains at the top of our Best Idea Long list as regional gaming trends continue to inflect positively so far in our data aggregation process for September.

In a week or so the focus will naturally shift forward to October’s performance, Q4 and beyond, but as analysts and investors update their models, we think September is setting up to be a nice boost to sentiment and Q3 numbers.

Thus far, virtually every state has put up accelerating revenue growth vs August growth rate, and that’s excluding the positive impacts of Sports Betting, iGaming, and new properties on the total pie. We remain bullish on the regional casino stocks as PENN remains a Best Idea Long.

CUBE

|

Long Thesis Overview: This is a "keep it simple and straightforward" type of call: (1) the subsector is highly correlated internally given the submarket overlap and works well in an inflationary environment, (2) CUBE backtests well in each of Quads 2-4, (3) upward earnings revisions are extremely likely and a positive catalyst, and (4) CUBE's balance sheet is a huge strategic and style factor advantage. |

We actually like Best Idea Long CUBE more here than peer PSA for two reasons: (1) on the quarter we expect Core FFO to come in a penny or two above the high-end of the $0.51 to $0.53 range which would be a larger order of magnitude beat, and (2) there is more of a delta between our model and consensus numbers on a tail duration (>5%).

In addition, CUBE serves as more of a Quad 2 in 4Q reopening play given its smaller size and larger exposure to the New York market.

TOST

|

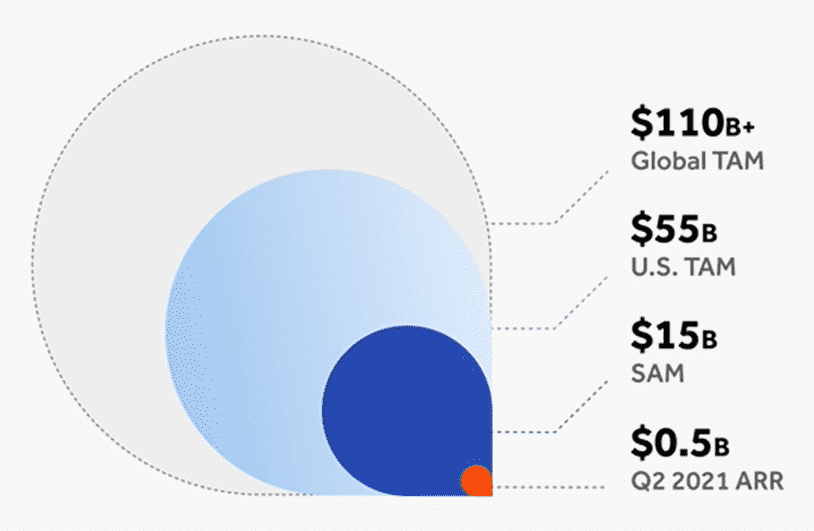

Long Thesis Overview: Toast (TOST) shares opened above the price range we highlighted in our pre-IPO Black Book. Comparing to publicly traded peers we thought the shares could trade up significantly. Not only did Toast have a larger TAM in the restaurant sector, but it also is set up to have a more dominant competitive position. |

Toast’s 2021 Annualized run-rate is $500 Million. According to Toast, the total addressable market in just the United States is $55 Billion and $15 Billion of this $55 Billion fall under Toast’s target customer. With such a small amount of the market tapped, there is significant room for growth.

Toast has just begun unleashing its salesforce on the thousands of restaurants in America. When adoption of their industry leading technology ramps up, their recurring revenue stream will as well. Technology is an inevitable component that is going to enter the restaurant industry. Restaurants which do not adapt to the times will struggle to compete with others.

BROS

|

Long Thesis Overview: The Dutch Bros concept looks strong and is an interesting competitor to SBUX. BROS is an owner-operator and franchisor of drive-thru shops that focus on serving quality, hand-crafted beverages with substantial average unit volumes. Founded in 1992 by Dane and Travis Boersma, Dutch Bros began with an espresso machine and a pushcart in Grants Pass, Oregon. Once public, BROS will be one of the fastest-growing restaurant companies by new store growth at 20% annually. |

Dutch Bros continues its expansion into the South opening a new location in El Paso Texas. The company said it is eyeing two more locations in the city to open in the next year. The AUV for the average Dutch Bros location is about $1.7 Million, which is tremendous for how small each location is.

For new openings in 2020 and 2021 however, the AUV for these locations is an astounding $2.1 Million. Dutch Bros has been selectively expanding into new regions. These new locations have shown to be even more successful than their west coast base. Both franchised and company owned locations are growing at a rapid pace.

dufry

|

Long Thesis Overview: Despite management teasing a 2023 recovery, we think the Street (and the current price) is still too conservative in not expecting a full recovery for another 5-years – particularly the European investment community. We think we’ll see a full recovery by 2023, on an EBIT margin double pre-pandemic rates. There’s your first paycheck. Then you get your second paycheck on the Hainan JV with Alibaba, which we think is running ahead of schedule (management is keeping people grounded here with expectations). That gets you paid by another CHf165mm, (1.50 per share) once the JV kicks into high gear in 2023. With the meaningfully higher margin profile comes the cash…and we think that the company will take out 15-20% of its share count over a TAIL duration – that is, unless it continues to consolidate the 88% of the industry it does not control. |

This stock is the mother of all reopening plays and as travel restrictions have gotten more relaxed globally, our conviction in the name has only gone higher. As a reminder this stock is a two-pronged thesis, the first is Dufry’s business coming back as the world reopens to global travel. Leisure travel is the big meal ticket here and is where travel industry datapoints suggest that there's major pent up demand.

That's what gets consumers into the stores where they're landlocked into an increasingly luxury experience -- often for hours at a time -- operating as a monopolist in each market with ZERO Amazon competition. The consensus does not have travel rebounding for another five years, and we think that they're being far too conservative. The second part of the thesis is the Alibaba partnership, which we think people for the most part are mismodeling because the company is being particularly vague about the progress there.

What we know is that it is a $5bn duty-free market today and should be more than $40bn by 2025. China Duty Free will get the lion's share of the business, but we think that DUFRY is already clocking in at 8%-10% share.

That's little today as the market is still in a nascent stage. But as the market grows, share grows, and scale leads to higher margins. Overall, we see this name getting to CHF 14-15 in EPS by year 5 of the model, which is meaningfully ahead of the consensus.

PLUG

|

Short Thesis Overview: Plug Power PLUG seems to be in the business of issuing shares of stock, even giving warrants to facilitate product sales at valuations that ended up being absurdly low. The behavior around the most recent equity offering looks dubious. Forklift fuel cells are a difficult business, likely entering a post COVID downswing. Reputational damage could become a broader issue, and we see ~80% relative downside. |

The enthusiasm for shares of PLUG, after a couple decades of consistent losses and equity issuance, is just stunning. No one on calls even asks for the efficiency of their fuel cells and electrolyzers – feel free to push your friendly neighborhood sell side Q&A participant to ask. Imagine not being able to resell hydrogen profitably, the being unable to buy at a reasonable price from Air Products, incurring cost to switch to Linde, all when the bull case for your stock is to become a producer and distributor of hydrogen.

PLUG’s installed base and most of the customers it is supplying relate to materials handling equipment – forklifts, a business that is losing out to Lithium Ion powered equipment. That doesn’t come up much on these earnings calls.

RRGB

|

Short Thesis Overview: Restaurants that we could operate at total capacity saw comparable restaurant revenue increase 7.0% from the pre-pandemic comparable quarter. In addition, margins at these restaurants reached 19.5%, a 180 bps increase. However, overall comparable restaurant sales are still down 2.4% compared to 2019. Nothing exciting to see with Red Robin Gourmet Burgers (RRGB). |

Restaurant sales and traffic growth for the week ending October 3rd were the weakest since mid-June. Sales growth for all segments except for fine dining deteriorated during the last two weeks in September compared with the first three weeks of the month.

The slowdown in sales growth was driven primarily by family dining and quick service. Dine-in sales growth is negative for all industry segments except fine dining. However, quick service, fast-casual and fine dining improved in their dine-in sales growth during the last two weeks of the month.

A decline in off-premise contributed to the slowdown in sales for limited-service brands over the last three weeks. For full-service restaurants, off-premise sales growth has been slowing from very high levels. The best performing regions were the Southeast, Florida, California, and Texas. The worst performing regions were New York-New Jersey, New England, the Midwest, and Mid-Atlantic.

SJM

|

Short Thesis Overview: Management lowered EPS guidance a quarter after raising it due to higher than expected inflationary headwinds. J.M. Smucker (SJM) reported FQ1 EPS of $1.90, down 20% YOY, but a penny above consensus expectations. Sales decreased 6%, but in constant currencies excluding divestitures, sales increased 1%. |

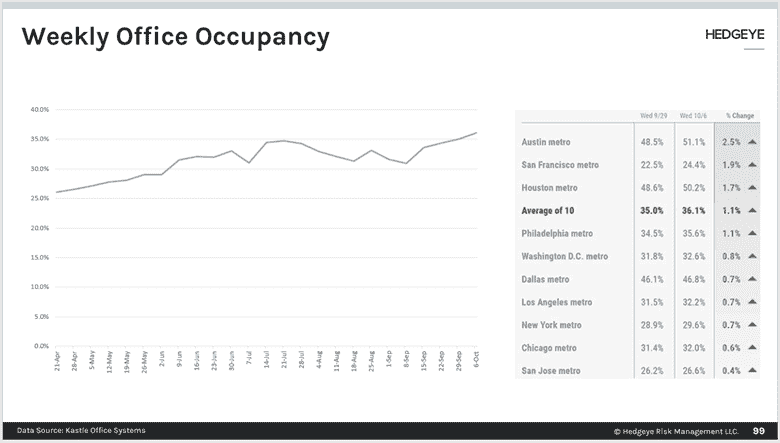

Kastle Systems' ten city occupancy average increased to 36.1% for the week of October 6 from 35.0% in the prior week. Kastle's occupancy barometer reflects access swipes to the office; it provides control systems to 2,600 buildings in 138 cities. Occupancy levels have steadily improved since the Delta variant in August, surpassing the highs of the summer. All ten cities had a sequential increase in occupancy rates.

The largest improvement came from one of the cities with the highest occupancies and the lowest occupancy. Austin had a 2.5% improvement over the prior week to 51.1%, and San Francisco had a 1.9% improvement to 24.4%.

J.M. Smucker’s coffee business was a key beneficiary of office workers working remotely. As workers return to the office their home coffee consumption will decline.

SFIX

|

Short Thesis Overview: There are clear negative implications there for sales predictability, gross margins, inventory turns and capital intensity. We don't think management is planning for having to compete like we think it will be forced to. This company was something special in its early pre-IPO days. Now it’s become just what the tech investors don’t want to admit – a retailer. Retailers trade on earnings and cash flow. A $40 stock definitely doesn’t respect that reality. |

The biggest issue with SFIX now is that it’s cannibalizing its core with a more capital-intensive business, Direct Buy aka Freestyle. It ran out of TAM – which is a curated and customized stylist/AI-driven assortment tailored to affluent women. That was a profitable business, which tapped out at about 800k-1mm customers.

Then it went to men, then kids, then Europe…all of which have been margin dilutive. The company should have stopped once it fully penetrated its core customer and churned out cash flow and bought back stock. But it didn’t. It’s new Freestyle program sidesteps the core competency of curating product for customers and allows people to pick their own threads. To be clear, that’s what Nordstrom and Macy’s do.

Good luck competing with those names at those companies’ core competency.

SFM

|

Short Thesis Overview: With growing concerns about their plans, We are adding Sprouts Farmers Market (SFM) to our shortlist. Sprouts' two-year stacked comp was negative in Q2. Management now expects the full-year comp to decline 5-7% from -LSD% to -MSD%. Guidance implies an acceleration in comps that seems aggressive. |

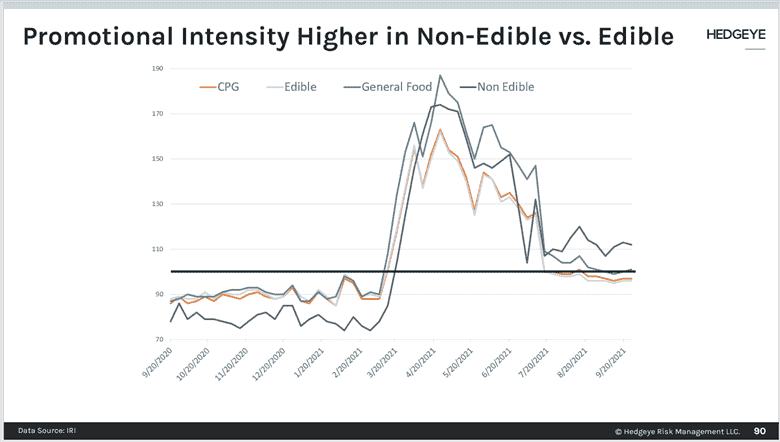

The promotional intensity in the grocery channel has pulled back with the Delta variant, as seen in the following chart. According to IRI, the percentage of CPG items purchased on promotional was 3% lower YOY in the week ended September 26.

For edible items, the promotional intensity was 4% lower YOY, flat compared to the prior week. For non-edible items, the promotional intensity was much higher, +12% YOY, down 1% from the prior week.

The most promotional sub-categories were general merchandise and home care, while beauty was 1% less than the prior year. Among edible sub-categories, beverages were the least promotional down 12% YOY, while general food was 1% higher and beverage alcohol was 2% higher. Thus, the level of promotions appears to rise and fall with COVID-19 concerns.

kr

|

Short Thesis Overview: Management raised EPS guidance from $2.95-3.10 to $3.25-3.35. Guidance for ID sales was raised from -4% to -2.5% to -1.5% to -1.0%, with the 2H expected to be flat to slightly positive. That implies a ~300bps deceleration in the 2H on a two-year stack basis. Management now assumes inflation to be 2-3% in the 2H. As they return to the office has been postponed, and indoor masking rules have been reinstalled in certain areas, food at home has benefited. A long investment in the grocers is also a bet on life not resuming to pre-pandemic behavior. |

This week Schnuck Markets, a grocer based in the Midwest, increased hourly wages for store employees. Employees earning below $12.10 per hour will be raised to that amount, while employees in specific departments earning below $12.75 per hour will be raised to that amount.

The size of the increase will depend upon the state. Union employees will receive the scheduled pay increase for January become effective in November.

In addition, Schnuck Markets announced two weeks ago that it would award a one-time performance and retention bonus of up to $600 to be paid out in January. The bonus will be the fourth the company has paid out since the pandemic. In a very competitive labor market, competitors' actions tend to be matched by others.