Hedgeye Position: Long Germany (EWG)

Positions Covered today: We covered the EUR-USD via the etf FXE for a gain following its sizable move since we shorted it on 11/4.

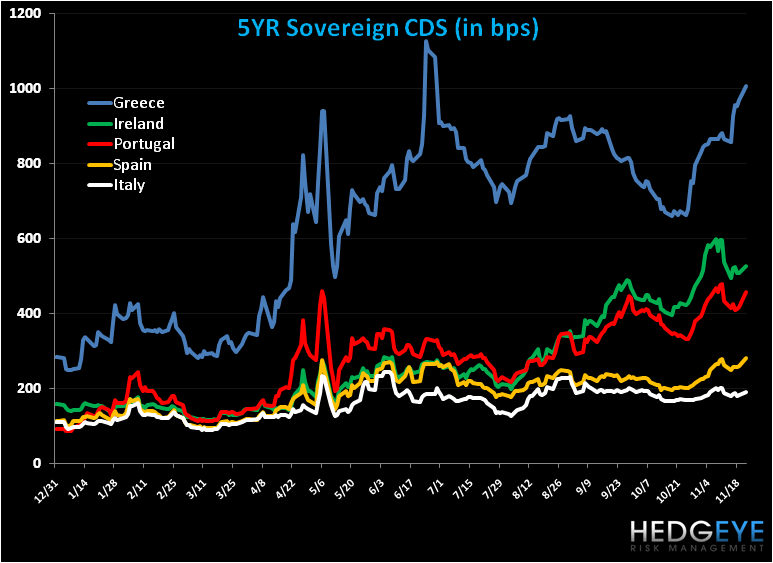

After an appropriate re-pricing of sovereign debt risk in the last week, we booked an immediate term gain on the short side of Italy (EWI). We remain bearish on Italy for the intermediate term TREND.

News out yesterday afternoon was icing on the cake in support of our conviction: don’t trust politicians, trust the markets. In a clear about-face statement from Ireland’s PM Brian Cowen late yesterday, who days before said he wasn’t going to be the scapegoat for the country’s fiscal state, he announced:

"It is my intention at the conclusion of the budgetary process, with the enactment of the necessary legislation in the new year, to then seek the dissolution of parliament.”

However, the dissolution of parliament could come far sooner than sometime next year. Here’s the political scene that’s playing out:

Having accepted an undefined bailout from the EU and IMF on Sunday (11/21) – projected at €80-95 Billion—Cowen and his party, Fianna Fáil, continue to wrestle against severe opposition to step down, especially as his narrow 3-seat parliamentary majority with his junior coalition partners, the Green Party, threatens to vote against him.

Cowen, however, continues to stress to the opposition parties of Fine Gael and Labour, as well as to defectors from his own party, that it is in the interest of the country (and markets) to first pass the scheduled 2011 budget package on December 7th, which is expected to shave €6 billion from the budget through spending cuts (~€4.5 Billion) and tax hikes of ~€1.5 Billion, to ensure a funding (bailout) agreement from the EU and IMF before a new election is called.

Yet standing in the way of his already paper-thin credibility, are calls from the opposition for a snap election and the uncertainty of a critical by-election vote this Thursday for one of the Green Party seats in parliament that could further turn sentiment against Cowen. The Green Party maintains support of the passage of the 2011 budget before elections are called. However, they appear resolute in their wish to see elections held by mid-January.

Finally, the government is due to publish a four-year economic recovery plan on Wednesday aimed at “bringing stability to the economy”, according to Cowen. Suffice it to say, we’re expecting a lot of pin action from Ireland over the coming weeks, and the Eurozone at large.

Below we show the familiar charts of the 5YR Sovereign CDS and 10YR government bonds yields as a proxy for the risk trade we see developing in Europe, especially from its peripheral countries. As you can see, despite Ireland’s bailout, yields continue to rise for the PIIGS; if Greece is any example, and we think in this instance it is a good one, the risk premium to own peripheral debt should remain elevated at least over the intermediate term, which in and of itself will pose significant challenges as government still require debt servicing to meet their fiscal imbalances.

And today was a great example of this: Spain issued €2.09 Billion of 3-month paper at 1.743%, almost double the 0.951% commanded for a similar issue on Oct. 26th.

As we’ve made clear in our research, we see a long road ahead for Europe’s Sovereign debt “crisis”. Ireland is but one piece of the puzzle.

Matthew Hedrick

Analyst