TODAY’S S&P 500 SET-UP - November 23, 2010

As we look at today’s set up for the S&P 500, the range is 51 points or -2.16% downside to 1172 and 2.10% upside to 1223. Equity futures are trading lower as uncertainty prevails over the Irish bailout and following reports of North Korea firing artillery shells on a South Korean island.

In important MACRO data today: Q3 GDP (first revision), Oct Existing Home Sales and Nov FOMC Minutes.

- Brocade Communications Systems (BRCD US) sees 1Q adj. EPS, rev. below est.

- Hewlett-Packard (HPQ) boosted FY adj. EPS forecast above est.

- La-Z-Boy (LZB) 2Q sales missed est.

- Oxford Industries (OXM) prelim. 3Q adj. EPS above est.

- China Xiniya will start trading today on the New York Stock Exchange under the ticker XNY. Zogenix will list on the Nasdaq

- Stock Market under the ticker ZGNX.

PERFORMANCE

- One day: Dow (0.22%), S&P (0.16%), Nasdaq +0.55%, Russell +0.41%

- Month-to-date: Dow +0.54%, S&P +1.23%, Nasdaq +0.98%, Russell +3.41%

- Quarter-to-date: Dow +3.62%, S&P +4.96%, Nasdaq +6.9%, Russell +7.57%

- Year-to-date: Dow +7.2%, S&P +7.42%, Nasdaq +11.58%, Russell +16.3%

- Sector Performance: Tech +0.59%, Consumer Discretionary +0.33%, Utilities +0.24%, Materials +0.16%, Healthcare (0%), Consumer Staples (0.08%), Telecom (0.31%), Industrials (0.33%), Energy (0.39%), and Financials (1.41%)

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: 58 (-476)

- VOLUME: NYSE: 918.82 (-16.60%)

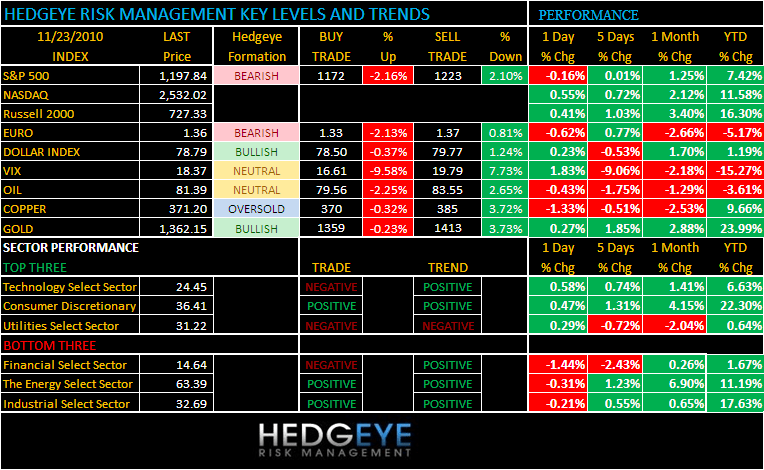

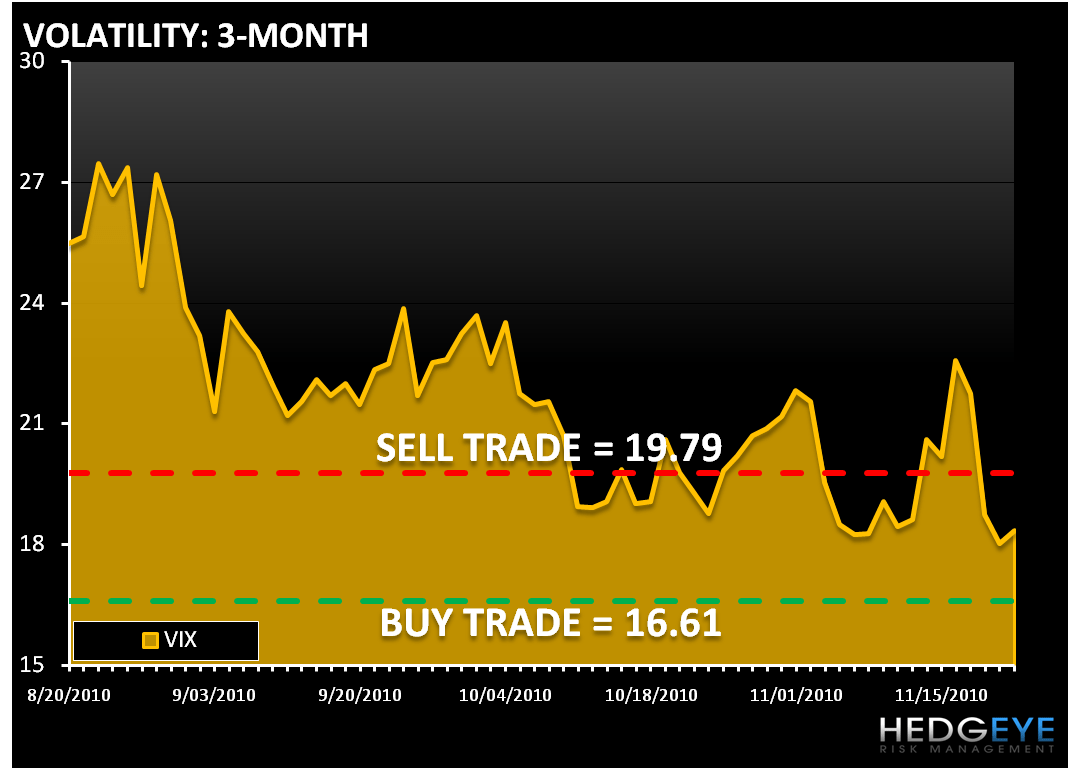

- VIX: 18.37 +1.83% - YTD PERFORMANCE: (-15.27%)

- SPX PUT/CALL RATIO: 2.21 from 1.09 +102.44%

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: 15.56 -0.406 (-2.544%)

- 3-MONTH T-BILL YIELD: 0.15% +0.01%

- YIELD CURVE: 2.31 from 2.36

COMMODITY/GROWTH EXPECTATION:

- CRB: 298.02 -0.29%

- Oil: 81.74 -0.29% - NEUTRAL

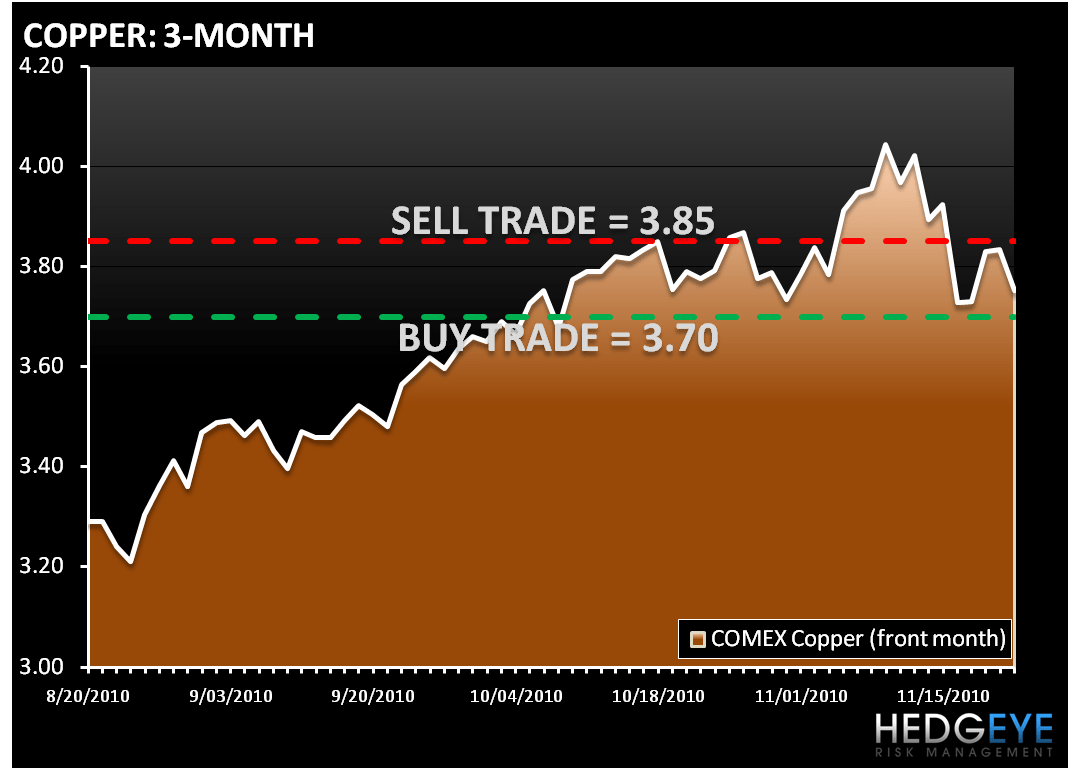

- COPPER: 376.20 -2.09% - BEARISH

- GOLD: 1,358.43 +0.33% - BEARISH

CURRENCIES:

- EURO: 1.3588 -0.62% - NEUTRAL

- DOLLAR: 78.682 +0.23% - BULLISH

OVERSEAS MARKETS:

European markets:

- FTSE 100: (0.62%); DAX (0.19%); CAC 40 (0.95%)

- Indices are trading firmly lower as concerns over the state of the European debt crisis and North Korea shelling South Korean positions triggers risk aversion.

- A stronger dollar keeps Basic Resources shares lower, while banks stay below the gain line reeling from uncertainty amid the economic crisis.

- Eurozone Nov preliminary Manufacturing PMI 55.5 vs consensus 54.4 and prior 54.6

- UK Oct mortgage approvals for home purchases 30,766 vs consensus 31,000 and Sep 31,058

- Germany Nov Flash Manufacturing PMI +58.9 vs consensus +56.8 and prior +56.6

- Germany Nov Flash Services PMI +58.6 vs consensus +56.0 and prior +56.0

- Germany Q3 Final GDP +3.9% y/y vs preliminary +3.9%

- France Nov preliminary Manufacturing PMI 57.5 vs consensus 55 and prior 55.2

- France Nov preliminary Services PMI 55.7 vs consensus 54.8 and prior 54.8.

- France Nov Business Climate +100 vs consensus +102 and prior +102

- Spain sells €2.09B 3-mth t-bills, bid-to-cover ratio 2.3 vs 2.8 in last auction, average yield 1.743% vs 0.951% last auction

Asian markets:

- Nikkei (closed); Hang Seng (2.7%); Shanghai Composite (1.94%)

- Asian markets went down today on worries about European debt. Sentiments were further dampened when news broke of military hostilities on the Korean peninsula just after South Korea closed. The news caused investors to run to the US dollar, adding pressure to commodities prices and resource shares.

- In sluggish trading, South Korea fell. Hyundai fell 3% on worries about labor disputes; Kia Motors declined 2% in sympathy.

- Australia weakened on concerns about European debt and weaker demand for metals from China. Banks and miners fell.

- Commodities stocks were the biggest drag on China, though the market did recover more than a third of its loss in the late afternoon. Energy and mining shares were hit when the National Development and Reform Commission ordered coal miners to stabilize their prices after recent rises.

- Hong Kong Exchanges and Clearing fell 3% despite announcing it will extend its trading hours in March. Li & Fung fell 2% after saying it would buy Oxford Apparel. Large property stocks gave up 2-3%, and CNOOC lost 3%.

- Japan was closed for Labor Thanksgiving Day.

Howard Penney

Managing Director