We’re going short Weber (WEBR) as we think that you’re currently looking at peak demand, and subsequently peak margins and earnings – which are grossly unsustainable. This stock is egregiously expensive on recovery earnings, which should be about 70-80% lower vs what we see today. This call is quite simple…the company has been private for its entire life, and the PE firm that owned it since 2010 saw a unique window for an exit strategy by capitalizing on both the increase in housing turnover and the surge in demand for eating/cooking from home (particularly outdoors) that drove the category up by 40%+ over the course of COVID. That allowed the company to a) sell meaningfully more units through its wholesale and direct channels, and b) do so with little discounting driving Gross Margin from 45% to ~50%, and c) leveraging its SG&A infrastructure by taking down SG&A margins by another 300-400bps. All in, margins went from 11-12% pre-pandemic to something closer to 18-20% today. That results in about $0.75-$1.00 per share in EPS power this year. But let’s face reality…this company has 24% market share in what is usually a steady 3-5% growth category. Next year we’re likely to see the category shrink by a good 10%, and we don’t think WEBR will make up for that delta with increased market share. Ultimately, as the model quickly de-levers on more normalized top line trends, we think we’re back to 12% margins over a TAIL duration, which gets us to about $0.20 per share in sustainable earnings power (it has a staggering 287mm shares outstanding, plus a billion in debt). Yes, Weber is a great brand with dominant share and category leadership, but it’s not worth more than 20x-30x earnings – which suggests a $4-$6 stock vs its current $16. We’d actually argue a consumer durable-esque 12-15x multiple as being more realistic. There are near-term positive catalysts to watch out for, like the release of the June and Sept quarters (likely at the same time) which should be the end of the topping process for the P&L. There’s also ‘initiation day’ where the bankers are likely to come out and pump the stock in early September (it just IPOd Aug 5th). But don’t be fooled…the earnings power this company is putting up today is a mirage. Completely and utterly unsustainable. We see upside to $20 on the positive catalysts, and downside to the low single digits when economic reality sets in. Once we de-risk the coming earnings reports, this name has Best Idea Short written all over it.

-- McGough

Here’s more depth on WEBR from my man Bradley Jamison…

The company itself was founded in 1893 as Weber Bros. Metal Works, but turned to selling grills in 1951 when an employee of Weber Bros. Metal Works, George Stephen Sr, invented the charcoal grill. Since 1951 the company has rolled out other grill products like gas grills, electric grills and wood pellet grills, accessories and even a mobile cooking app. Grills currently make up 75% of WEBR revenue with the rest in its consumables and accessories categories. The company mainly sells through a network of 4,710 wholesale partners in 31,760 locations as well as through its website, Weber.com, and a group of 170 stores which are 95% independently owned. Its three biggest wholesale partners are Ace, Home Depot and Lowe's where according to the S-1 Weber has 52%, 39% and 32% of the grilling category market share, respectively, in each store. Weber also writes in its S-1 that it owns 23% market share of the U.S. grilling market and 24% of the global grilling market. The international business was over 40% of 2020 revenue as 36% of sales were in EMEA and 7% of sales were in Asia. There is no doubt that this company is one of the premier names when it comes to grilling, but you need more than a name to be a good stock.

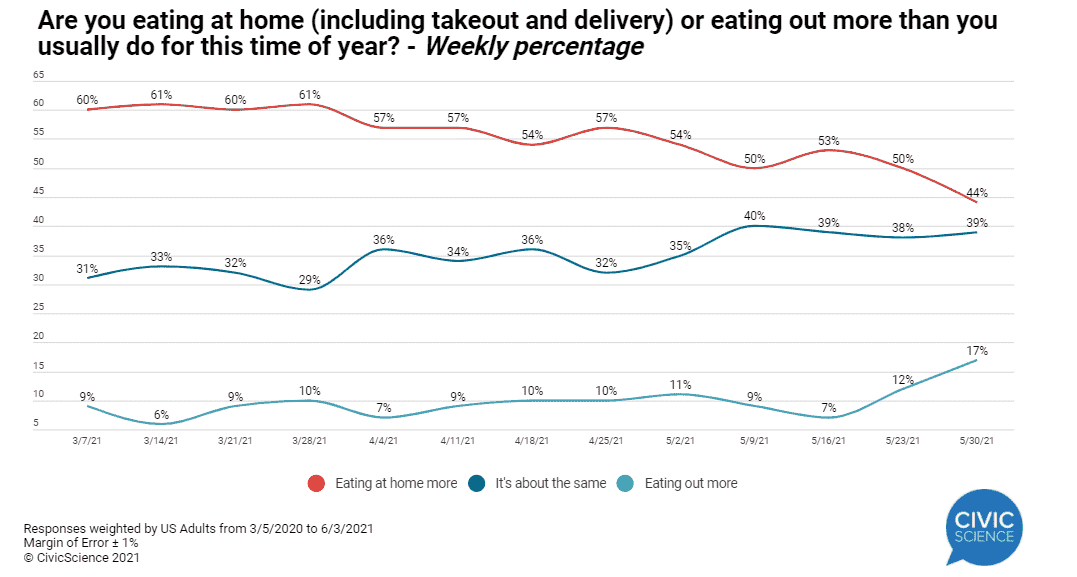

Coronavirus caused a fundamental shift in behavior towards things like outdoor activities, cooking from home, athleisure, work from home, home improvement but we already know this. The chart below shows from March 2020 to June 2020 the % of people that think they are eating out more and eating at home more. It's abundantly clear that in the pandemic people ate at home more, which stimulated sales for items that helped people eat at home, and when looking at results from the home improvement players that people took on tasks to make their home nicer (like set up an outdoor patio with a grill). Additionally, when looking at the (little) financial information that Weber gave in its S-1 you can see the business get a strong boost from COVID sales. The company has yet to report its June quarter, despite going public in August, and our guess is that the company will do a conference call to report joint results of the quarter ending in June (Q3) and the quarter ending in September (Q4) which will look strong in order to stimulate the market and keep people riding high on the company.

Source: Civic Science

So coronavirus created exceptional demand for grills, and that's great for Weber, but the fundamental question is "now what". One could argue that we are seeing an answer to that question already play out with the results of companies like W, AMZN, HD and LOW and how all these companies are slowing down. But the argument for shorting this stock is not that people will fundamentally shift all their behavior from grilling at home, but rather that all those people now have the grills at home to use and have no need to buy a new one. Grills, similar to mattresses, are a long replacement cycle good (average of 5-7 years) and after a serious surge in demand we think WEBR will see a serious deceleration in sales as customers have already purchased the grills that they need. On top of that, the evidence is showing (chart below) that people are feeling more comfortable eating at restaurants so perhaps not only will people not be buying new grills soon, but that replacement cycle could be even longer if dining out continues to increase in popularity and people leave their grills sitting in the back yard. Yes, there are the Delta Variant worries, but again the variant might cause people to eat from home, but those people already have the grills/equipment to do so and are not buying new ones anymore. At the end of the day, we simply believe Weber cannot comp the extraordinary COVID comp that it put up. This company came public at the height of popularity for grilling and outdoor activities, and in our opinion probably should have remained a private company.

Source: Civic Science

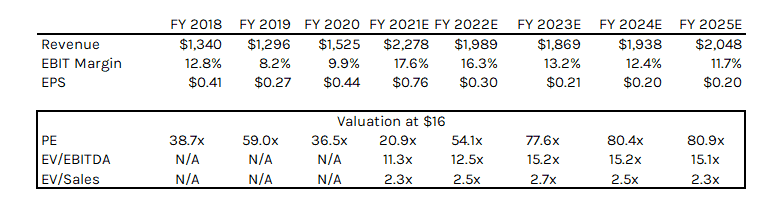

While above is our argument on a macro level, lets dig in to the financials released in the S-1. Pre-Covid this company did $1.3bn in sales at an adjusted operating margin between 11-13%. The grill industry according to industry research grows at a CAGR of 5% per year, and WEBR according to its S-1 grows at a CAGR of 10% year. However, the major qualification to that is the company is including its incredibly robust LTM revenue in that CAGR, if that is excluded the company grows closer to the industry CAGR. The company is also affected by seasonality with the first half of WEBR's fiscal year (Quarter ending December and Quarter ending March) slower than the back half (as seen on google trends graph below). However the company did release the financial results of the 6 months ending March 2021 (slow season) which revealed sales growth of 62% vs the 6 months ending March 2020 and an operating margin of 17%, significantly above the 9.8% operating margin for the 6 months ending March 2020. As mentioned above we think the back half of this year will also show strong results given that those two quarters are the company's strongest quarters and the company has not released any financial information on those quarters yet. On an annual basis the company grew 18% in FY 2020 and we estimate near 50% growth in FY 2021 with peak margins. The point is these growth numbers of 50-60% in a 5% industry with peak margins near 17% for a business that typically does 12% are just unsustainable going forward. We think this company reverts back to historical operating margins with slowing sales from the gains made in COVID leading ultimately to EPS nearly 70% lower than where it will come in this year.

Source: Google Trends

WEBR filed its S-1 in July and officially listed on August 5th. Originally the company planned on selling 46.9mm shares in the range of $15-$17 putting the valuation at a height of $5bn, but instead downsized the offering to selling 18mm shares at a price of $14/share putting the valuation under $4bn. The company has been majority owned since 2010 by BDT Capital Partners which is the firm of Warren Buffet's longtime banker Byron Trott with other owners being the Stephen Family (using an entity called WSP Investment LLC) and executive management. According to Factset BDT owns 34% of the company. The company, since it was a normal IPO, is subject to a traditional 180-day lockup period after which the executives, directors and pre-IPO LLC members can dispose of any shares.

We are short WEBR at $16.18.