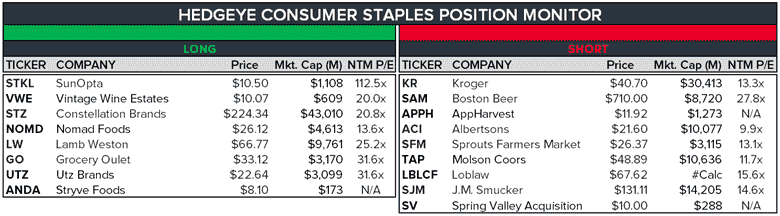

Position Monitor Changes (BUD, NOMD, SFM)

Missed hand-off to international growth (BUD)

We are removing Anheuser Busch InBev (BUD) from our long list. We added the shares as a long last year anticipating a robust on-premise recovery benefiting the international markets, particularly balance sheet deleveraging, and a window of time when hard seltzer share gains and a strong on-premise recovery would offset secular headwinds in premium light beer. However, due to the following concerns, we are removing BUD:

- The pace of the recovery in international markets has been slower than anticipated.

- The company has not been able to offset the negative attention of share losses in the U.S.

- Margin headwinds from higher packaging and distribution costs are extending the timeframe needed to return to 2019 EPS.

- The debt maturities have been extended with no meaningful maturities in the next couple of years, but the leverage limits the strategic options available to management.

- BUD is also a quad-three underperformer.

Better prospects now than before, unappreciated by the market (NOMD)

We are moving Nomad Foods (NOMD) higher on our long list. Shares are attractively valued at 13.5x 2021 run rate EPS. The near-term concern is whether the company can see organic growth accelerate in the 2H to achieve guidance of 1-2% for the year. If the company can meet or exceed EPS guidance (we are in the latter camp), but organic revenue was flat to down, it would seem unlikely shares trade below 12x EPS with organic revenue and total revenue growth accelerating. Our focus is on the company’s organic growth prospects after the pandemic comparisons, whether its competitive position has improved post-pandemic, and the brands’ ability to pass on inflationary pressures. Nomad Foods is coming out of the pandemic with better growth prospects, margin outlook, and competitive position than it did before the pandemic.

Growing concerns about their plans, adding to the Short List (SFM)

We are adding Sprouts Farmers Market (SFM) to our shortlist. Sprouts' two-year stacked comp was negative in Q2. Management now expects the full-year comp to decline 5-7% from -LSD% to -MSD%. Guidance implies an acceleration in comps that seems aggressive. The company has changed its strategy from using promotions in fresh produce to drive traffic to an EDLP strategy. Sprouts Farmers Market does not have its historical traffic drivers - circulars and promotions- without the benefit of store traffic growth from the return to pre-pandemic shopping habits. There is increased risk to the top line and gross margins by winning new grocery shoppers in an environment with elevated digital spending.

The company is also changing its future store format to shrink the size by reducing the backroom. This requires additional distribution centers to implement, but the smaller store size is expected to reduce the capital investment and improve returns. The smaller investment and higher returns are expected to lead to an accelerated store opening plan. However, lower sales would lead to lower returns, jeopardizing the double-digit store growth plan and the company’s multiple.