“I work all the time. I sometimes take the liberty of looking at a beautiful woman’s face. It’s better to be passionate about beautiful women than gay men.”

-Silvio Berlusconi, 11/2/2010

If the quote above didn’t get your attention this morning, we’re not sure what will. What has been getting our attention over the last few weeks is heightening risk across Europe, especially in the region’s peripheral countries of Portugal, Ireland, Italy, Greece, and Spain, affectionately named the ‘PIIGS’. This inflection in risk, which we’re measuring via government bond yields and CDS spreads, has re-emerged following a reduction in risk in the month of September and most of October.

We believe that this rise in risk is a reflection of the Crisis in Confidence, namely the continued inability of Europe’s peripheral governments to instill investor and public confidence that they can cut bloated fiscal imbalances and resolve internal political disunity.

Currently, Italy’s PM Berlusconi is the region’s poster child for this renewed Crisis in Confidence, including his latest scandal surrounding an 18-year-old belly dancer that he allegedly gave €7K to and helped free from a theft charge. Elsewhere, poor leadership in Europe, from Greece, Portugal, Ireland to Hungary and Romania, continues to propel market risk upward. Interestingly, economic indicators reveal that current levels of risk, in particular in Ireland and Portugal, resemble levels last seen shortly before Eurozone finance ministers were forced to issue a €110 Billion bailout for Greece on May 2, 2010 and days later, along with the IMF and World Bank, a €750 Billion package to rescue troubled European nations.

Given this risk inflection in Europe, we took the explicit tact to short the EUR-USD via the etf FXE in the Hedgeye Virtual Portfolio on 11/3/2010 with the currency pair trading at our immediate term TRADE resistance level of $1.42. (From here we see TRADE support at $1.39 and intermediate term TREND support at $1.33). While we’re cautious on the region as a whole, we are positioned long Germany via EWG (bought on 11/8/10) and remain short Italy (EWI) as a way to play the developing Sovereign Debt Dichotomy. Below we highlight the risks we see mounting and elaborate more on our positioning given the region’s outlook.

Risk is ON!

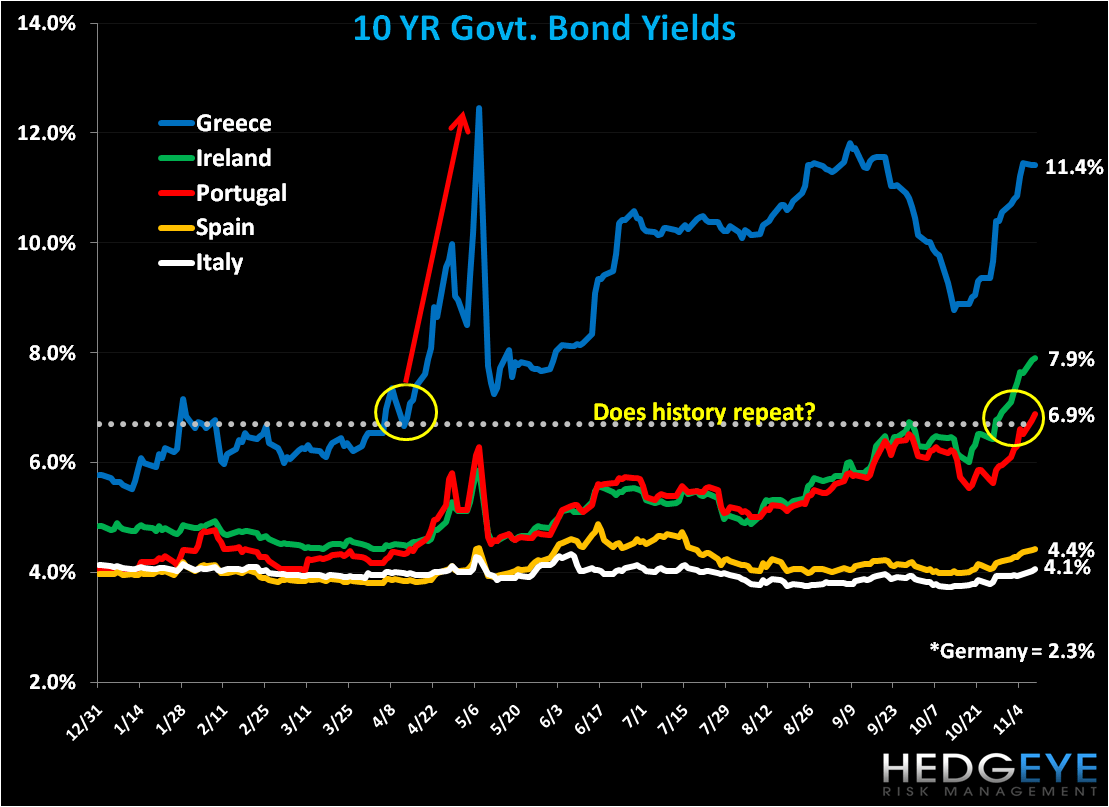

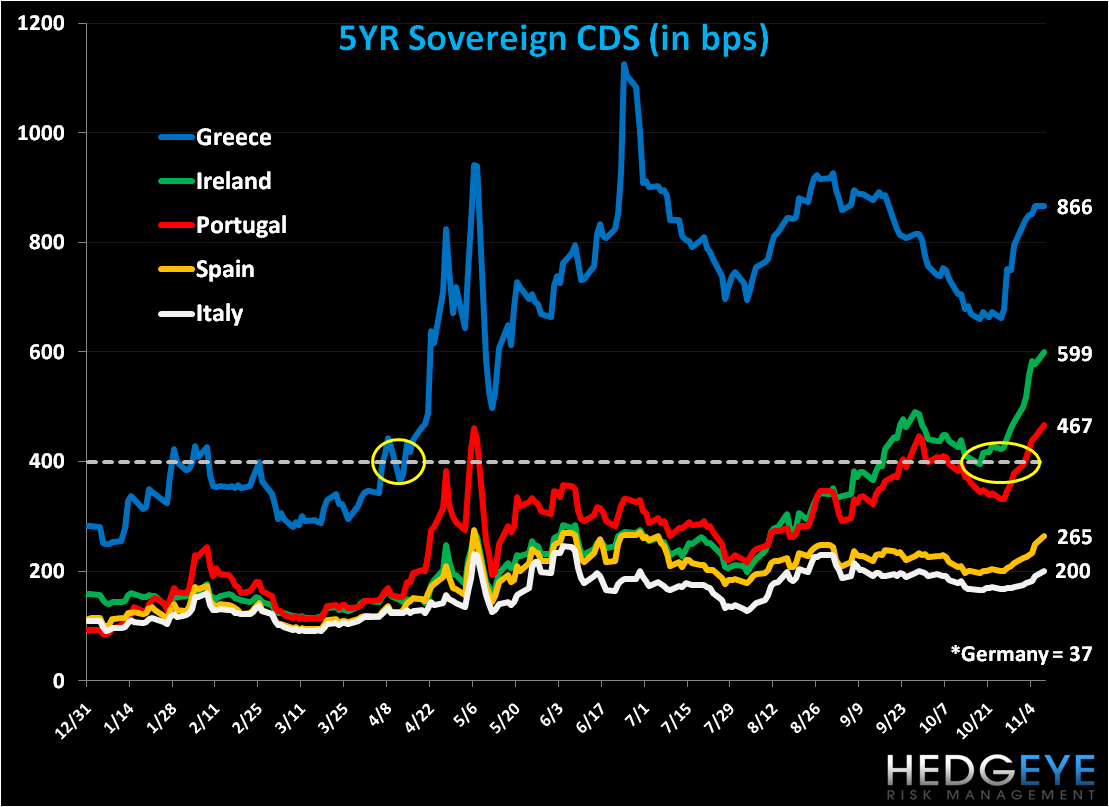

While the excessive public deficit and debts of the PIIGS are well understood by the capital markets, we believe that the recent heightening in the risk trade is a reflection of the perceived threat that these countries will NOT be able to meet their targeted debt and deficit reduction plans via austerity alone. While Greece was the first to report that its 2009 deficit must be revised up to 15.1% of GDP from 13.8% and debt to 127% of GDP versus a previous calculation of 115.1%, we don’t think it will be the last country with upward revisions. But if you don’t want to take our word for it, the hockey stick curves in the charts of both government 10YR bond yields and sovereign CDS spreads (see chart below), might convince you that the market is pricing increased risk ahead.

It’s worth noting that the slight decline in Greece’s 10YR yield over the last days is a reflection of the support PM Papandreou’s socialist Pasok party got over the weekend in local elections. Despite the victory, we still believe there is a void of confidence in Greek leadership from a domestic and international perspective. Also, we’d note in the CDS chart that the 400bps line has been an important indicator for us as a breakout line. Clearly, Ireland and Portugal are treading dangerously above this level.

As we’ve shown in our research since 4Q09 when we started to track Greece’s rising risk premium, Europe’s periphery has wholly “earned” its reputation: after pigging out on low interest rates for nearly a decade, many countries (and in particular Spain and Ireland) continue to deal with the flip side of that leverage coin in the form of ongoing housing price declines, high unemployment and slack growth. Now with these governments overextended deficits-- and we’ll use Ireland as an example with a deficit/GDP ratio forecast to balloon to 32% this year--it’s increasingly clear that despite all efforts by the country to implement another €6 Billion in spending cuts and tax relief, investors aren’t buying a smooth recovery ahead, and rightfully so! As yields push up so too does the cost of capital which further handcuffs a country’s ability to refinance and raise debt, which in turn snowballs the perceived sovereign default risk.

Finally, as the chart below drives home, the PIIGS are truly running up against a wall of debt, especially next year, compared to their more fiscally conservative neighbors. These are headwinds to keep front and center.

Pants Down versus Pants On: Short Berlusconi versus Long Merkel

While we applaud countries focusing on trimming fiscal fat now to benefit long-term “health”, there’s clearly near- to longer term downside risk to growth across the region from austerity measures. In particular, we expect to see spending and confidence slow across much of Europe as such austere measures as increases in VAT, wage and benefit freezes, and job destruction impact these economies over the next 1- 4 years. To position ourselves in an environment of Sovereign Debt Dichotomy we’re long Germany (EWG) and short Italy (EWI) in the Hedgeye Virtual Portfolio. Again, here it’s worth considering the leadership differences that weigh on economic performance.

While it’s worth a laugh, and certainly worthy of Page 6 in the NY Post, the scandalous actions of Italy’s PM Berlusconi, including photos of him literally with his pants down at a vacation villa last year, have severe political and economic implications for country. While we’ll spare you the intricate political dealings, Berlusconi’s rule is in checkmate since he expelled his speaker of the Parliament, Gianfranco Fini, back in July. Now Fini, who has enough backers in the legislature to deny Berlusconi a majority and bring down the government, faces his own political impasse. Even if he were to bring a defeat to Berlusconi he would likely be forced into further political gridlock for competing coalition rule. So even in the best case, if there is one, we expect further prolonging of the “paralysis” that is Italian politics.

With authoritarianism, inefficiency, and back-handedness hallmarks of Berlusconi’s rule, we also worry about the risks associated with the country’s public debt levels. In 2009, public debt equaled 115% of GDP, the second highest in Europe behind Greece, and the country is rolling up against €500 Billion of government debt maturities (principal +interest) over the next three years--a level equivalent to Germany’s obligations, yet from an economy 1.6x larger than Italy’s. Equally, strong foot power (strikes) against the government’s proposed €30 Billion in austerity cuts remain and the country’s aging population is a longer term headwind worth considering. Statistics show that Italy will have the oldest population by 2015 and 2020 in the Eurozone, with a population >65 at 21.9% and 23.2%, respectively. So, as Italy’s population ages its government will face increased outlays and reduced receipts, which will add additional economic headwinds.

On the other hand, while the Germans will also have to deal with an aging population, we continue to like the country’s intermediate term set-up. Germany’s growth profile of 3.3% this year and 2.0% next year outperform many of its peer countries, with inflation expected to be around the 2% level, a budget deficit projected around -3.5% of GDP in 2010, and strong export demand from Asia. Of note is the latest export data that shows a monthly increase of 3.0% in September, with sales to Asia 2x that to America.

From a policy standpoint, be it from Chancellor Angela Merkel to Finance Minister Wolfgang Schaeuble or Bundesbank President Axel Weber, the Germans continue to tout fiscal conservatism, most recently running a position to mandate that European states trim deficits to -3% of GDP or better and public debt to less than 60% (the current position of the EU’s Stability and Growth Pact) or else bear a tax (as a % of GDP) for the violation. We think longer term this could be a viable strategy.

Putting fundamentals aside, there’s a clear divergence between Europe’s fiscally conservative and fiscally bloated counties on an equity basis. Year-to-date equity markets in Denmark and Sweden are up +27.7% and +17.2%, with the German DAX up +14.0%, while the PIIGS are some of the worst performers across all global indices: Greece’s ASE -31.0%; Spain’s IBEX -13.0%; Italy’s FTSE -7.3%; and Ireland’s ISEQ -7.1%.

This Time Is NOT Different

We continue to note the seminal work of Reinhart and Rogoff, who in their book “This Time is Different”, show historically (across 800+ years) that countries reach a crisis zone of fiscal imbalance when their debt ratio is north of 90% and deficit ratio is greater than 10%. With the PIIGS largely in violation on both measures, the threat of sovereign default remains one to keep front and center.

While the case could be made that countries like Ireland, Portugal and Greece make up too little a share of Eurozone GDP (roughly 6.3%) to drag down the region’s outlook, two points are worth considering:

- Greece’s sovereign debt “crisis” in the 1H10 led to a 20% deterioration in the EUR-USD, so small economies can indeed have a significant impact, and

- Should Spain and Italy, economies representing ~ 28.7% of Eurozone GDP, run up further against a Sovereign Slide, we could see far greater repercussions for the region as a whole.

Keep your risk management pants on.

Matthew Hedrick

Analyst