McDonald’s is scheduled to report its October sales numbers before the market open on Monday, November 8th. October had one less Thursday, and one additional Sunday, than October 2009. Based on this, I would expect a similar impact to that felt in January 2010 (-0.4% to +1.0%), varying by area of the world) which also had one less Thursday and one additional Sunday than the January prior.

In every region of the world, consensus estimates are calling for a significant slowdown in two-year average sales trends from September levels for MCD. On a relative basis, a 5%+ in global same-store sales still suggests that MCD is continuing to take market share.

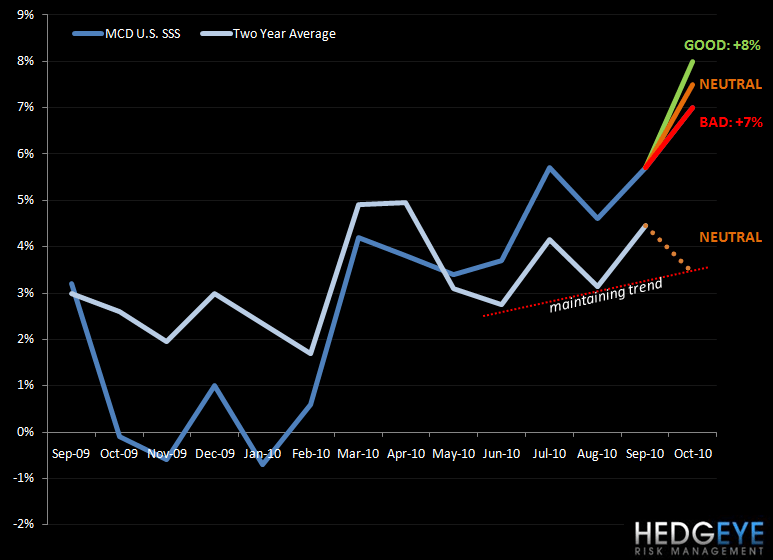

Below I go through my take on what numbers will be received by the street as GOOD, BAD, and NEUTRAL, for MCD comps by region. For comparison purposes, I have adjusted for calendar and trading day impacts. To recall, September same-store sales numbers showed improvement across the board. While Europe and APMEA had been soft in August, they rebounded strongly in September. The U.S. saw more marginal improvement. In October, MCD needs to post impressive numbers in order to maintain the performance seen in September. Expectations are likely muted, and I would expect some leeway to be given in terms of how investors view the results.

U.S. - Facing an easy -0.1% compare (including a calendar shift which impacted results by +1% to +1.7%, varying by area of the world): As of today, the street is estimating a +6.1% comp in the U.S. Based on our checks, the slowing sales of smoothies and Frappes will negatively impact same-store sales by 1-2% versus September.

GOOD: A print of 8% or greater would be perceived as a good result because it would imply that the company was able to maintain two-year trends close to those seen over the summer months. While usually I look for an improvement in calendar-adjusted two-year average trends, and an 8% print would imply a significant slowdown from September, it is important to note that a +8% comp would be the strongest print since February 2008. This may sound slightly unrealistic to some, but given the especially easy comparison of -0.1% from October 2009, it seems like it could be in play.

NEUTRAL: Roughly 7% to 8% implies two-year average trends that are approximately between 23 bps and 73 bps below the calendar-adjusted two-year average trends seen over summer and considerably below those seen in September. However, given that a 7% print would still be 73 bps above the highest same-store sales number seen this year, in July, investors would likely view this as a neutral number.

BAD: Below 7% implies that two-year average trends deteriorated sharply on a sequential basis from September. Given that the U.S. was the only market to maintain sequential two-year trends over the last three months, a sharp drop off of the magnitude that a 7%-or-lower result implies would be received negatively (though it is important to remember that the current consensus estimate falls in this range).

Europe (facing a difficult 6.4% compare, including a calendar shift which impacted results by +1.0% to +1.7%, varying by area of the world): As of today, the consensus estimate is for Europe to post +4.2% same-store sales growth.

GOOD: A print of 5.5% or higher would be viewed positively because it would imply two-year average trends slightly below those seen during September in Europe (after accelerating sharply from August levels). This would be the highest print since May. Additionally, given the strong performance in September, investors will be watching to see if two-year trends maintain a level above 5% or have since moved lower towards the soft two-year trends in August.

NEUTRAL: A result of 4.5% to 5.5% would imply that sequential trends decelerated from the strong performance in September but maintained a level above those seen in August.

BAD: Less than 4.5% would imply, approximately, a 100 bp deceleration in two-year average trends from August. Additionally, two-year average trends would fall below 5% which, with the exception of August, has not happened since February 2010.

APMEA (facing a 4.7% compare, including a calendar shift which impacted results by +1.0% to +1.7%, varying by area of the world): As of today, the consensus estimate is for APMEA to post +5.5% in same-store sales growth.

GOOD: 8% or higher would imply a slight acceleration from the results seen in September (after slowing in August). Following the strong print in September, it will be interesting to see if performance in the APMEA region was maintained from the third quarter into the first month of the fourth quarter.

NEUTRAL: Between 7% and 8% would imply two-year average trends roughly in line with those seen in September. While the midpoint of this range implies a slight deceleration, it is unlikely to concern investors too much given the strong rebound in September sales in the APMEA region.

BAD: Below 7% would imply a significant slowdown from the two-year average trend in September and a return to the level of two-year average trends seen in August, which was a lackluster month for MCD APMEA.

Howard Penney

Managing Director