|

Below is an excerpt from a complimentary research note by our Gaming, Lodging & Leisure analyst Todd Jordan. We are pleased to announce our new Sector Pro Product Gaming, Lodging & Leisure Pro. Click HERE to learn more. |

The Singapore government hopes to start normalizing the country when it comes to finally Covid. The goal is to start opening the borders in September which could bring in a lot of gambling seeking visitors.

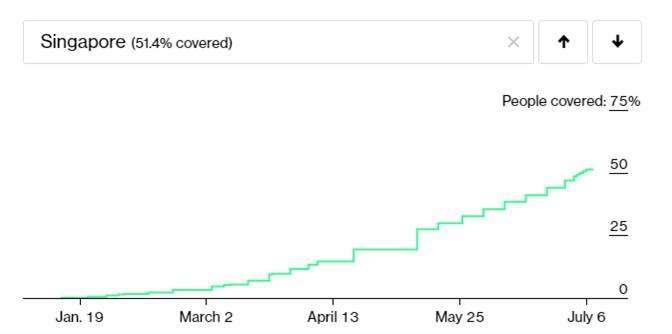

Unlike most of the rest of Asia, Singapore has made western like progress on vaccination with a rate above 50% as shown in the chart below.

By August 9th, the government hopes that 2/3rds of the population will be vaccinated.

Contrast this with Hong Kong at only 27% vaccinated, Macau at 28%, while China sits at 47%.

New Covid cases are down to single digits in Singapore and the country is feeling good about their Covid situation.

The upshot is that the city state seems ready to get back to normal including allowing foreign visitors from Australia, New Zealand, and, importantly, mainland China and Hong Kong.

Las Vegas Sands (LVS) and Genting Singapore would be 2 of the main beneficiaries of reopening as they operate the only integrated casino resorts in country.

It’s a long road back for Asian casino hotels back to 2019 levels but with a gambling local population, LVS managed to generate approximately 35% of 2019 quarterly run rate revenues in Q1 2022.

That number should skyrocket as soon as Q4 if all goes to according to plan. Macau, LVS’s other Asian market, could feasibly experience a big jump in Q4 as well but a lot needs to happen between now and then.

Macau did just lift the quarantine requirement for Guangdong visitors last night so that’s a start. But the short term road to recovery now seems a little more smooth for Singapore than the other gaming markets at this point.

LVS looks like a very inexpensive stock to us right now considering the low valuation, high quality assets, and long term growth profile. However, we all know that cheap stocks can get cheaper.

What the stock needs is a catalyst and while positive Macau developments would likely top the catalyst list, the Singapore developments are very encouraging.

Marina Bay Sands is the company’s largest property based on 2019 EBITDA so it should matter.

Macau has been frustrating but it's difficult to see the sentiment there getting much worse. All told, we’d be buyers at these levels and as such, LVS remains a Hedgeye Best Idea.