There’s mounting anecdotal and macro evidence that suggests momentum has slowed in the home improvement sector over the past 4-6 weeks. Below we’ve taken highlights (lowlights) of commentary from major suppliers to the DIY channel from earnings calls over the past few weeks. While this is hardly scientific, the breadth of product categories covered here along with the consistency of the negative commentary is something to consider. Yes, we know that the supplier base to HD and LOW is highly, highly fragmented. Either way, these are several of their largest suppliers.

Putting anecdotes aside, we’re also including a handful of the latest data points supporting Hedgeye’s Housing Headwinds call. The data simply speaks for itself and on the very surface should be factored into anyone’s process for evaluating further recovery in the DIY marketplace. In our view, the topline challenges resulting from a double-dip in domestic housing will likely be too big to overcome in the near-term. As such in the absence of accelerated revenue growth, earnings should come under pressure.

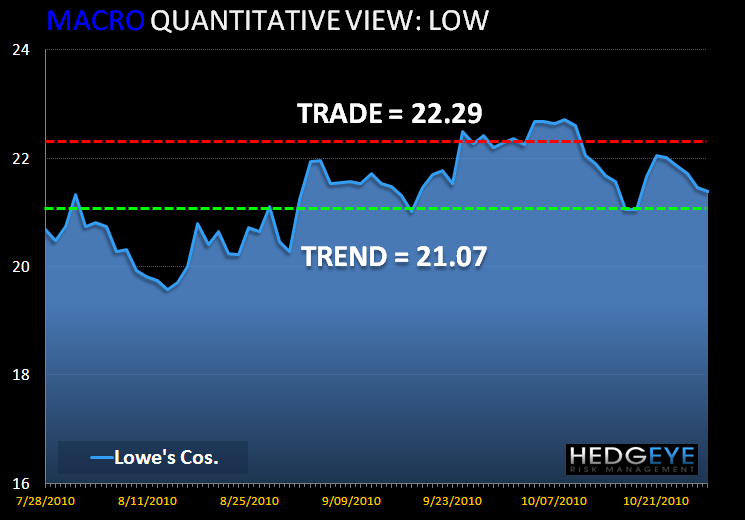

Finally, to complete the trio of comments and supporting macro data we’ve included our Macro team’s quantitative (and bearish) view on LOW. Of all the home related names, LOW stands out as the name with the greatest downside risk. Hedgeye’s key price levels are below:

Supplier comments

10/14 Universal Forest Products (UFPI)- We were disappointed in our sales to our big-box customers, but pleased with the advances we're making with other retail business. We were equally disappointed with our drop in margins, but I can't imagine a circumstance again that would lead to such challenges with inventories.

By market, our sales to the DIY market decreased 8% due to a decline in unit sales as a result of soft consumer spending. Within this market, our mix changed as well. Sales to our big-box customers declined 13% while sales to other retailers increased 11% due to market-share gains.

10/20 Stanley Black & Decker (SWK)- On the mechanical side, they're still battling tough market conditions. They had a negative 6% organic growth in legacy Stanley, five points of that was attributable to a large retail customer destocking residential hardware. That was pretty much as expected.

Okay, well I would say the weeks on hand, first of all, we have one major retailer that took about half a billion dollars of inventory out in their system in the last 90-120 days, and that may or may not continue into the fourth quarter, probably will continue to some extent.

…we see a scenario where point-of-sale is not robust at most of these customers. It's not terrible. It's just kind of bumping along flattish kind of territory, and our invoice sales was very consistent from a volume point of view, from a unit point of view, with that in the legacy Stanley business in the third quarter. So as we would step back from it I'd say we would probably see caution at the winds in the retailers, and part of our outlook reflects that, so we've kind of baked in the environment in a very reasonable way here.

10/21 Briggs & Stratton (BGG)- We continue to believe that overall inventories in the channel are reasonable for this time of year. It appears that OEMs, mass retailers and dealers are continuing to be very conscientious with regard to the amount of working capital invested in inventories.

10/26 Masco (MAS)- We'll start with Cabinets. Tough quarter in both North America and internationally. Sales for Cabinets were down 18%.

Other question I wanted to ask was on key retail sales or sales to key retailers that softened in 3Q, it looked like four points versus 2Q. Can you give any further perspective on to that and to sell in relative to sell through perhaps trends in the quarter and kind of how things have started out in 4Q there?

I think we saw slowness pretty much across-the-board, whether it's a smaller ticket item like paint or plumbing or a big ticket like cabinet, so there isn't any issue or concern relative to share. No concerns, just outside of the macro environment I think our feeling is that consumers have just sort of closed down to a certain extent and we talk a little bit about that coming out of the second quarter. So I don't think there's any unique trends or anything else going on Donny that I'm aware of.

I'll take the repair/remodel related activity. I think if anything, you can kind of see that in our sales to our key retail customers. We were positive in the first quarter of this year. We were flat in the second quarter. We're down a little bit in the third quarter, so if anything, our experience is that even lower ticket items we're seeing a little bit of slowness. Now, again, is that temporary? This year has been kind of funny. It started out very slow. March and April were pretty strong and since that point in time, things have tended to slow up a bit. Still not seeing a lot of traction for larger ticket repair/remodel activity.

I think there's maybe been a little bit more traffic. A little bit more in terms of people looking or considering but not necessarily willing to pull the trigger. In terms of price commodity over the last three months or your specific question is about price, I don't know that I would say that things are any more difficult than they normally are. That's always a tough conversation and will continue to be a tough conversation but I don't know that it's any more difficult. We continue to manage price commodity very aggressively and I don't know Donny if you have anything you want to add.

10/27 Whirlpool (WHR)- And we did see some softness in demand during the third quarter. In spite of this weakening demand environment, over all we performed very well from a branded share perspective.

And while we have had a very positive consumer receptions to our new product innovations launch during the third quarter, the overall price mix environment was more challenging than our previous expectations particularly North America.

But at the same time industry volumes and the pricing environment were more challenging than expected and we took actions to make some aggressive competitive pricing pressure.

Let me also allude a little bit to this one. North America has, right now, flat to high inventory levels so it's about what we consider optimal. And that's basically twofold, one is yes there's quite a bit of Q4 pre-build and the other piece, we saw the market slow down in particularly during the second part of the third quarter and obviously it takes a little while to take that out of inventory. We have taken measures to work the end of September particularly in October, November to run down production to what we would consider appropriate levels of inventory which given the somewhat choppy demand environment will be slightly higher because we have got to be able to respond to the change in demand trend.

Housing Headwinds

The following are excerpts from recent posts published by Hedgeye’s Financials team. If you’d like additional data or more detailed analysis supporting the Housing Headwinds thesis, please let us know

New Home Sales

New Home Sales rose 6.6% to 307k SAAR. Is this a cause for celebration? Remember that it was just six months ago that a then-record-low print of 300k caused significant angst and a material selloff. Since then the numbers have remained in this 300k range. Expectations appear to have come a long way. To summarize our cumulative displacement theory, there was an epidemic of overbuilding during the bubble, which will take a very long time to work off. Using a sales rate of 300k, we calculate that sales would have to continue at this level for ten years for the cumulative displacement from the mean to return to zero. Yes, new home inventory is very low, but we don't see sales rebounding anytime soon.

Home Sales Rise as Prices Fall

Existing Home Sales rose 9.7% to 4.53 million (seasonally adjusted annualized rate) in September. As Existing Home Sales are a lagging data series, it is still benefiting from a rebound off of the post-tax-credit lows. Below we show charts of existing home sales and median prices.

Case-Shiller

The following chart shows Case-Shiller home price data on a month-over-month basis. As we've highlighted previously, by S&P's own admission, investors should not rely on the seasonally adjusted (SA) data as their seasonal adjustment factors are essentially unreliable. Rather, investors should rely on the non-seasonally-adjusted data as a better indicator of underlying trends. It's worth emphasizing that the Case-Shiller series does have a notable seasonality - specifically, it generally improves sequentially through April, May, and June - so the NSA data has its own shortcomings.

Eric Levine

Director