PNK beat our Street high EBITDA estimate pretty handily. Margins were better at every property – and they’re not done yet.

The PNK thesis is a secular margin story. EBITDA improvements are likely, even in a soft regional gaming environment. We like that PNK is 18 months behind the industry in terms of cost cutting. We like that previous management thought that three corporate headquarters and a couple of corporate jets were appropriate, that marketing was like a government agency that needed money thrown at it but didn’t need to produce results, that a fabulous high cost development pipeline was what mattered, and that they really didn’t care about margins. The new management is a beneficiary of previous management’s mismanagement, if you will.

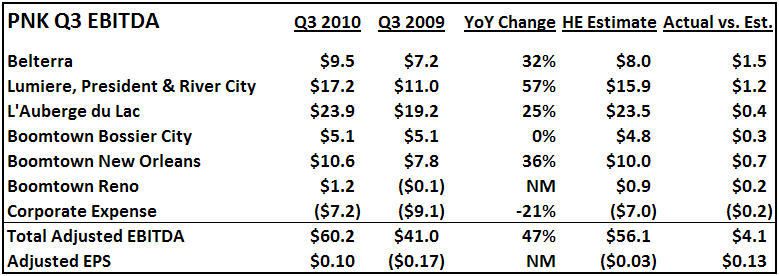

It’s not like the margin story isn’t well known. Consensus EBITDA projection was higher than last year despite sluggish revenues. However, we were a lot more bullish on the size of the margin improvement which drove our Q3 EBITDA estimate to $56.1 million versus the Street at $51.5 million. So where did they come in? $60.2 million. This management team is doing a great job. Forward estimates look too low.

PNK beat us in EBITDA at every property. While revenues were slightly better overall, margins were the story. Here are the numbers relative to our expectations: