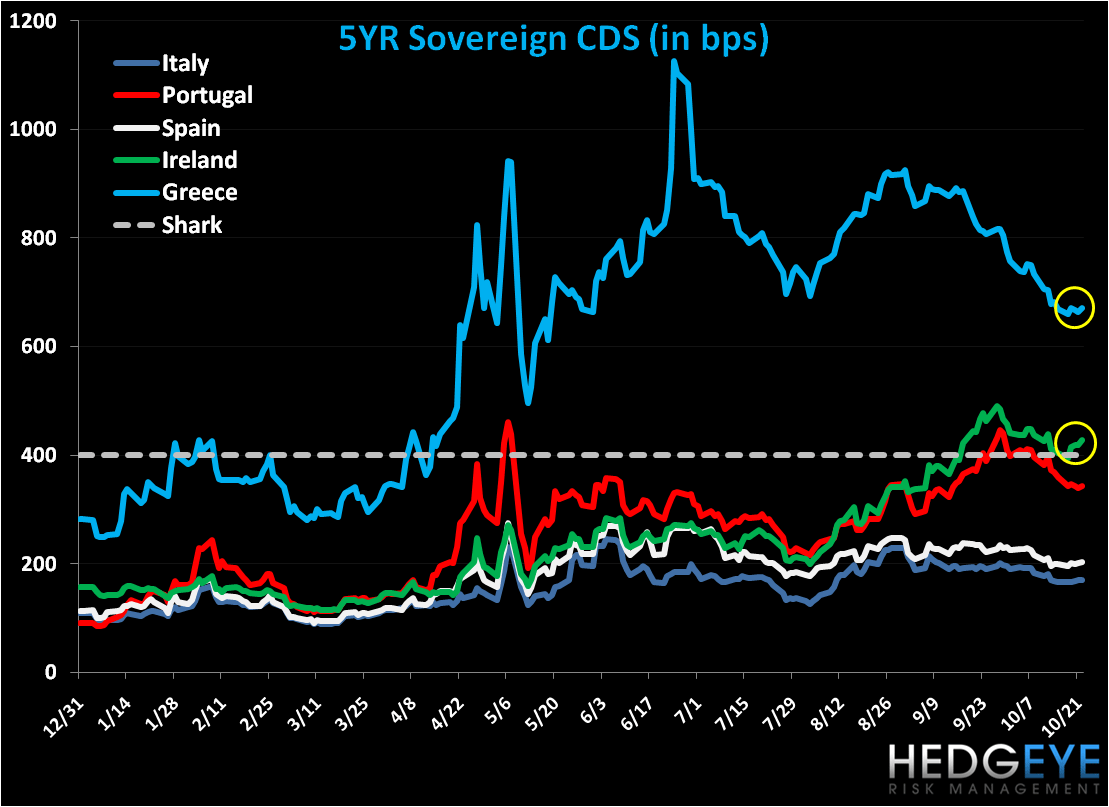

Below we show charts of 5YR Sovereign CDS spreads (in bps), Greece’s equity market (ASE), and the Greece 10YR bond yield. Interestingly, last week the Greek CDS spread and 10YR bond yield showed an upward inflection. Of the many risks being priced into Greece’s credit markets, we think it’s worth note that the country’s budget deficit is likely to be revised upward for both 2009 and 2010, as rumors spread that the country’s accounting (in conjunction with Eurostat) was wrong.

We are currently not invested in Europe after selling our position in Germany (via the etf EWG) this morning in the Hedgeye Portfolio. Keith sold EWG to take a gain with its immediate term TRADE overbought; however its intermediate term TREND is bullish. The DAX is up +11.4% YTD versus the UK FTSE at +6.4% or SPX at +6.7% YTD).

Matthew Hedrick

Analyst