We got absolutely everything we needed to hear and see from this CPRI print to reiterate it as a Best Idea Long over both a TREND and a TAIL duration. The quarter was outstanding, with the company coming in at $0.38 per share vs the Street's expectation for break-even. While earnings beats are no shocker this earnings season, the underlying business here has some really nice momentum. In fact, in what might be a first in many years, CPRI management actually guided UP 1Q expectations (it almost ALWAYS guides the upcoming quarter down), and it gave extremely detailed EPS guidance for the year (ending March 22). Though it straddled the street for the year, it's abundantly clear to us that management is extremely confident about its’ trajectory for all three brands. We're taking up our estimates for the year to $5.00 for the year, which is well above both guidance and the Street at $3.75.

If there was one theme that we'd point to, it's that Versace is really starting to turn a corner and become a meaningful contributor to the underlying results. Versace sales were up 10% for the quarter, on top of a +55% last year despite the fact that Europe was largely shut down this entire quarter. It's ecomm business was up triple digits, and along with MK and JC, it comped 100%+ in mainland China -- the most important luxury market in the world. The accessories business is particularly strong at Versace -- which proves many naysayers wrong who just a year ago were telling us that CPRI management lacked the chops to expand the brand into this margin-accretive business.

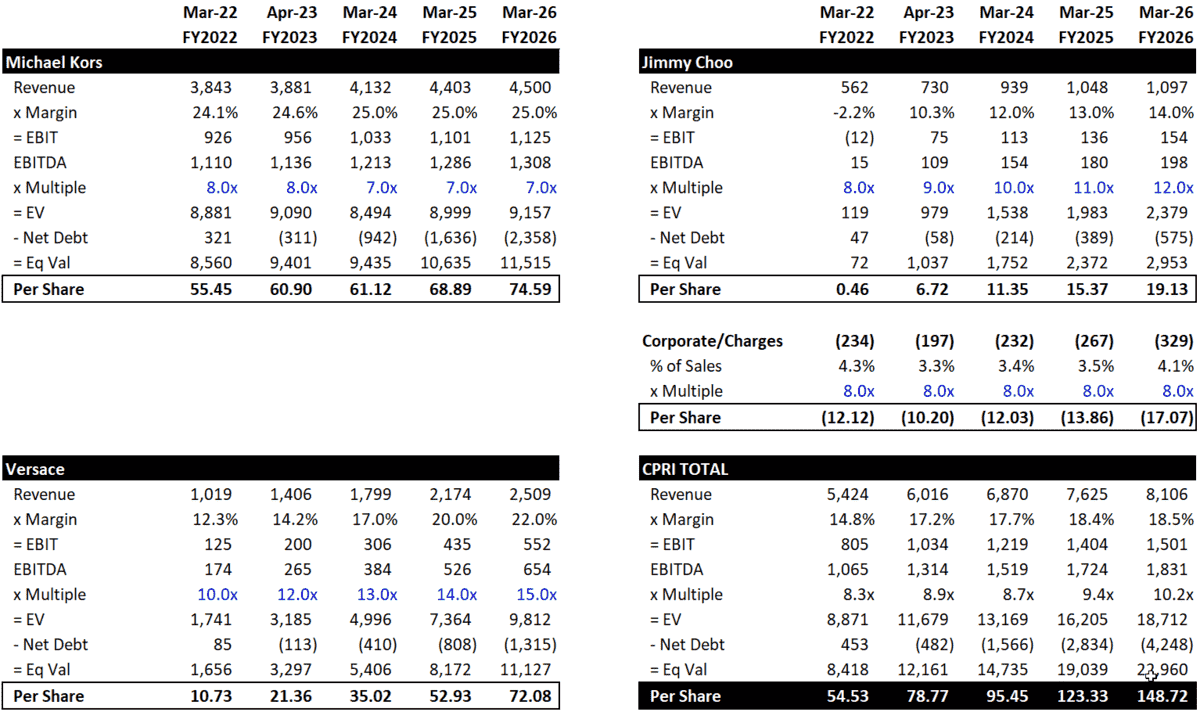

The company is hosting an analyst meeting on Jun 29th, where we think it will accelerate top line growth targets for Versace, and will give the nod that this is a mid-20s margin business (vs 12% today). To be clear, this is a business that is likely to break through $1bn in sales this year, growing 40%+yy with margins going to a low-teens rate vs losing money pre-pandemic. We think that it's ultimately a $2-$3bn business at 25% EBIT margins, which begs the question as to what you'd pay for such an asset. For a controlled, yet fast-growing high margin luxury brand growing at a steady-state rate of 20-30% -- a 20x EBITDA multiple is far from being considered a stretch. Do the math on that… in two years, a 20x multiple on Versace suggests a value for that brand alone of $55. In other words, at today's price, you're paying for one of the hottest luxury soft goods brands on the planet, and you're getting Michael Kors and Jimmy Choo for free. That's not half bad when you consider that using an annuity-like multiple of 7x on KORS at 25% margins gets you to better than $60 in value on top of that. If you assume that Jimmy Choo and Corporate Overhead wash each other out, which we do in our SOP model, that gets you to a double from $55 over a 1-2 year time period.

We might be playing down Jimmy Choo with that comment, but the reality is that high-end women's dress shoes is likely to be one of the hottest categories globally upon reopening. More social events means more outfit purchases, and a new dress is unlikely to be worn with a pair of 2-3 year old shoes -- not for this customer at least. We assume that this is ultimately a low-mid teens margin business, and can more than double in size from where it is today.

One of the most important parts of this story for us is the deleverage we're seeing on the balance sheet. This is a company that peaked out at $2.2bn in debt post acquisitions/pre-pandemic. But within 18 months, it should be sitting on a net cash position as the growth and margin profile (and therefore cash generation) accelerate. The leverage is actually one of the biggest points of push back we get from the long-only investment community in pitching the idea. For that reason, the one thing that would make us sour on this story is if it levered up further to do another deal. The way we see it, it has 5+ solid years of 20% EPS growth, which is all organic. The last thing the company needs to focus on -- at least today -- is integrating more brands into the fold. Fortunately, M&A is low on the priority list for management.

Ultimately, we're well ahead of the consensus. For this year, as noted we’re at $5 vs $3.75, and then have EPS growing by ~$1 per share per year up til $9 in EPS power 5-years out. Our Sum of Parts models is below, which gets us to 75% over 12-18 months, or 100% upside if we use a more aggressive (and more appropriate) multiple for the Versace Asset.