The Investing Landscape is Changing... Fast

Our call is for U.S. growth and inflation to start slowing in 4Q 2018.

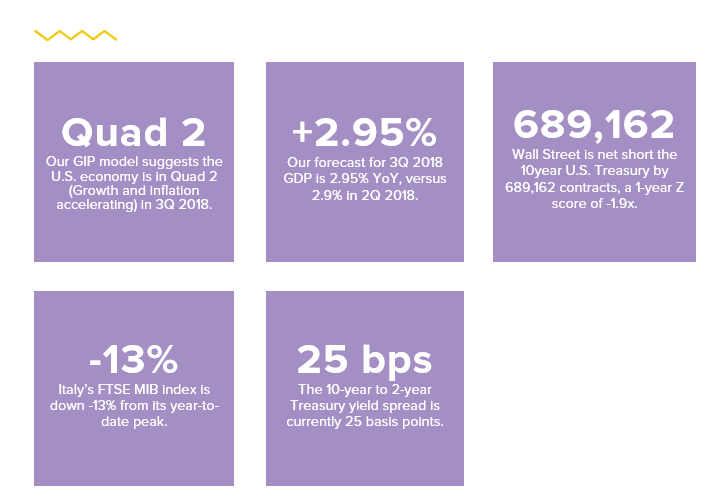

The third quarter ends this week. If we're right, after Q3 data is reported the U.S. economy will have accelerated for 9 straight quarters (from 3Q 2016 to 3Q 2018). This is an unprecedented streak in U.S. economic history.

As is often the case, Wall Street is taking this #GrowthAccelerating trend and extrapolating it far out into the future. This is dangerous. After a historic run for the U.S. economy, it's exactly the wrong spot to be long #GrowthAccelerating and short bonds. We want to get you prepared for the coming #Quad4 environment (U.S. growth and inflation slowing).

This week's Market Edges is all about getting you ready for #Quad4:

- In Client Talking Points, we dissect Wall Street consensus positioning and the perils of being long Europe and Emerging Markets.

- CEO Keith McCullough explains why we're sticking with our call long bonds and bond proxies in this week's Chart of the Week and What the Media Missed.

- Senior Macro analyst Darius Dale analyzes why short high beta, growth and momentum is the investing playbook heading into #Quad4 (see Sector Spotlight)

- Finally, in Around the World, we feature a letter and video from Keith explaining our Macro process from start-to-finish

Happy Macro Monday! Good luck out there this week.

WEEKLY ASSET ALLOCATION

No TACRM asset allocation update this week. Please note that we are updating and improving our model based on subscriber feedback. Stay tuned. CLICK HERE to watch a brief video, “Understanding How We Think About Asset Allocation."

CLIENT TALKING POINTS

Emerging Markets, Wall Street Positioning & Europe vs US

1. Emerging Markets = Selling Opportunity

Is this the beginning of the next “globally synchronized recovery” or just a bear market bounce in Emerging Markets? Argentina just printed a down -4.2% y/y GDP report. Chinese Stocks and Copper were up +5% and +9% in the last five days. Emerging Markets were up almost +4% last week. Plenty of short-selling opportunities at these lower-highs. "I've been waiting and watching for an Emerging Markets (EEM) immediate-term TRADE #overbought signal and last week we got it," CEO Keith McCullough wrote last week.

"We were the only independent research firm to make the SELL Emerging Markets call back in JAN 2018. While there seem to be plenty of experts who can tell you why EM "should be going up because its cheap", we'll stay with the measuring and mapping process that had us move to the bear side to begin with."

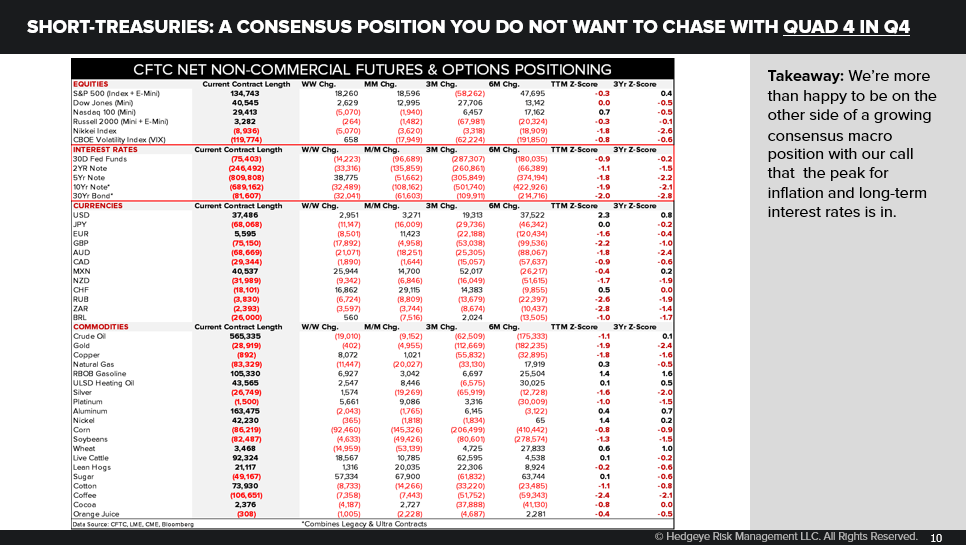

2. Wall Street is Still Short Bonds

In Quad 4 (our Q4 2018 forecast of Growth and Inflation slowing), short Treasuries (biggest net SHORT position currently in all of macro), is not where we want to be.

Consensus again moved shorter of bonds week-over-week in all contracts except the 5-Year. However the month-over-month reality is that positioning is marginally SHORTER in every contract. The most extended open interest based on the trailing twelve month & 3-Year Z-score methodology is now in the 30-Year bond (-2.0x TTM & -2.8x 3Yr).

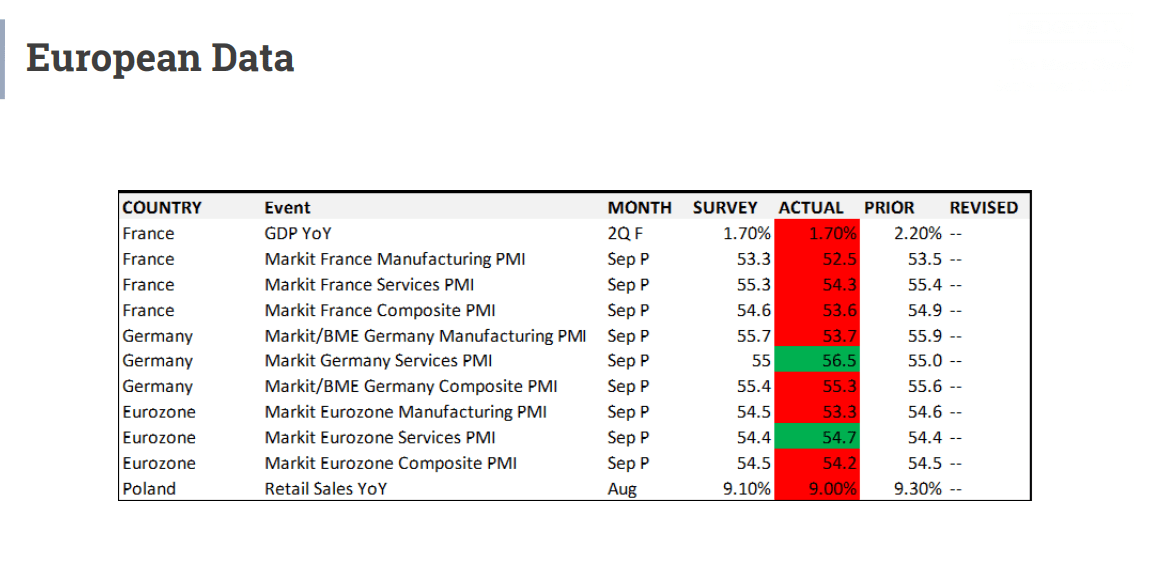

3. U.S. Beats Europe

French GDP is now below 2% after hitting its peak cycle last year down at 1.7% versus 2.2% last month. That’s in sharp contrast to what’s happening here in the U.S. Remember when we were telling you to short Europe last year? The bulls on Wall Street were telling to buy it because European stocks were cheap. And the election of Macron meant it was different this time in France. Nope.

Here's the performance from the year-to-date peak to present in European stock indices:

- France's CAC 40: -3%

- Euro Stoxx 600: -5%

- Germany's DAX: -9%

- Spain's IBEX: -10%

- Italy's FTSE MIB: -13%

... meanwhile, the S&P 500 +9.5% year-to-date.

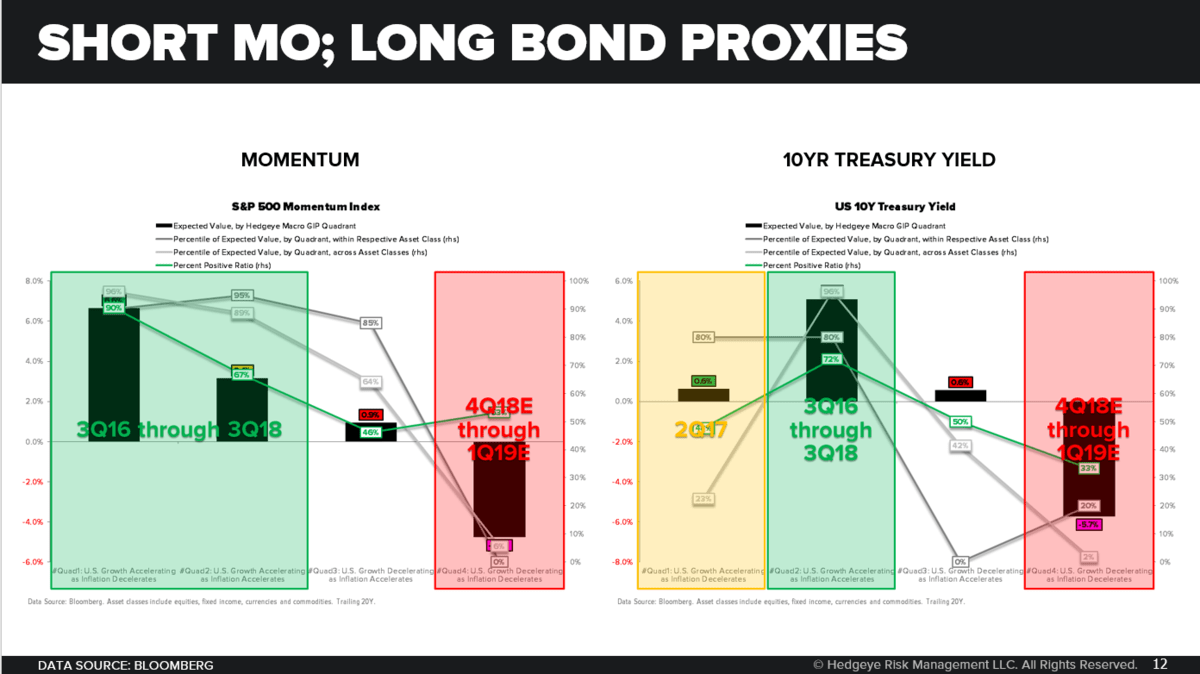

CHART OF THE WEEK

Early Look: Short Mo, Long Bond Proxies

Below is a key excerpt and chart from a recent Early Look written by CEO Keith McCullough. Click here to read this Early Look in its entirety:

|

Admittedly, I was somewhat fascinated by how fast the UST 10yr Yield ripped to 3.08% in the last few trading days. I was on the road in Texas and when asked on the why, my response was something like this:

Throw some Macro Tourist advertising about the “Fed Readying To Raise Rates” on top of all that and voila. I get one heck of a buying opportunity in everything I want to have in my p.a. in Q4. What should your portfolio be long of in Quad 4?

What should your portfolio be getting rid of heading into Quad 4?

I know. I know. This probably sounds as crazy as it did when we told you to get out of European Equities 1-year ago and out of China and Emerging Markets in January of 2018. I don’t do pot, but I do get crazy! What’s even crazier about all of this is that if the last 3 weeks are signaling anything, Mr. Market has already beaten me to the punch, selling the worst performing US Equity FACTOR EXPOSURE in Quad 4, Momentum, ahead of me. All I’ve done so far is move to buying the SECTOR STYLES I didn’t like for the 9-month run in Quad 2 (bond proxies). I haven’t gone all wild and crazy and started shorting something like Tech (XLK), yet. Pardon the pun, and bear with me. I have one more week to fully re-position (and get this slide deck done!). |

TOP 5 STATS

SECTOR SPOTLIGHT

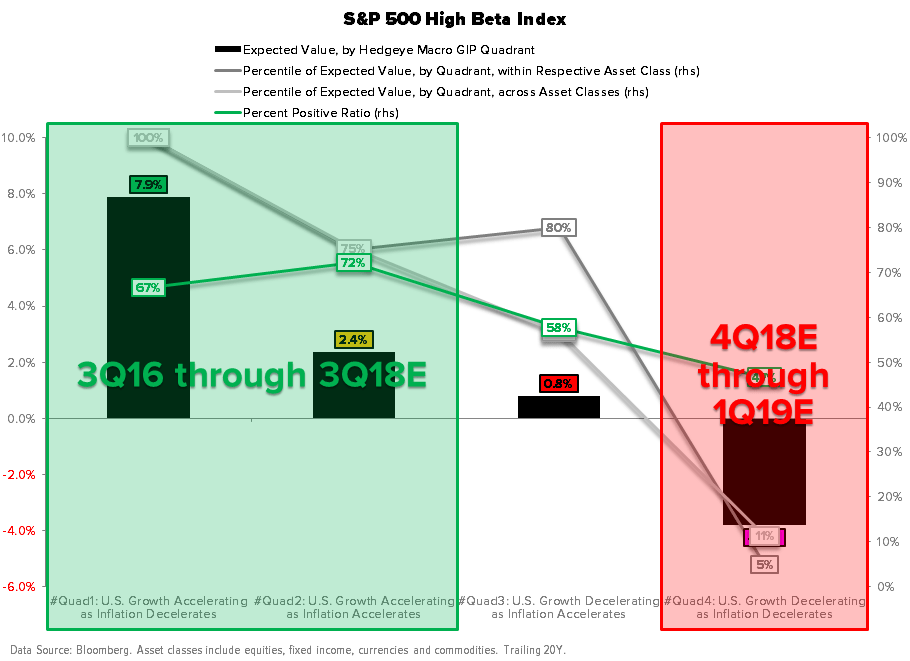

A Note From Darius Dale: #Quad4 = Short Momentum, High Beta & Growth

Below is a brief note written last week by Senior Macro analyst Darius Dale.

|

Keith alluded to this in his Early Look note this morning (see Chart of the Week), but the primary reason we sound so wacky when we author new calls is not because we’re overtly trying to be non-consensus, but rather the fact that no one else on the Street has our model. Indeed, our secret sauce is born out of the fact that we contextualize the world exclusively and dogmatically in rate-of-change terms. Moreover, our backtesting of financial market history according to our [proprietary] GIP Model quadrants allows us to generate alpha-generating research conclusions well ahead of investor consensus. On that note, history shows us that the three worst performing U.S. equity style factors in #Quad4 are:

Telling investors to book gains in these exposures before they crack probably sounds as silly as we sounded telling investors to sell Emerging Markets and Europe back in January (or telling them to overweight Growth in lieu of Value the entire ride up). Fortuitously for those among you who’ve entrusted the Hedgeye Macro Team to be your primary Macro research provider, we’re OK with sounding silly for a while if it means we help you preserve capital, generate alpha, and grow your business ex post. |

WHAT THE MEDIA MISSED

The Macro Show: We Reiterate Our Call On Bonds

We have received a number of subscriber questions about our call on long bonds and bond proxies given the recent move in bond markets. To be clear, we reiterate our call to be long bonds and bond proxies today.

Hedgeye CEO Keith McCullough answered subscriber questions on our bond call on The Macro Show recently. We wanted to pass along this 7-minute collection of video excerpts for you to watch.

Here’s the key takeaway from Keith:

|

“I don’t apologize for the process. I get up and I do my job… I’m not trying to minimize the pain you’re feeling this morning… But imagine the pain if you started capitulating on shorting Emerging Markets, China and Europe at the beginning of the year. These things were all careening to the upside when we first started making those calls. I’m always willing to take some pain for that longer-term gain.” |

The goal here isn’t to minimize the pain you might be feeling today.

Instead, we’re here to remind you to stick with the process that led to our call on bonds. “Understand that the process is in place to give you confidence,” McCullough explains. “You shouldn’t manage your money emotionally. That’s absolutely not the way to do it.”

Click here to watch this video. Below is a transcript of Keith’s comments.

* * * *

Subscriber: Long bonds, the dollar and the euro are each moving in directions counter to what you’re predicting for the #Quad4 (Growth and Inflation slowing) macro environment. Is this just a short-term pop? How much pain do you think we should expect to tolerate?

Keith McCullough: You have to incur some pain if you want to accomplish anything. Again, if the data were to change, I would change. If I get run over in a hockey game, do I change my skates? No, I get up and do what I do.

Pain is part of the game.

I don’t apologize for the process. I get up and I do my job. So that’s what we’re going to do. If anything changed on Utilities and Treasury bonds, I would let you know. It’s not my job to lose for protracted periods of time.

I know it’s hard. And I’m not trying to minimize the pain you’re feeling this morning. This will happen. And you should blame me, because I’m accountable to it.

If the worst pain you feel is a couple more basis points of upside in the 10-year yield, I can empathize with that, I get it, especially if you’re going big on it. But imagine the pain if you started capitulating on shorting Emerging Markets, China and Europe at the beginning of the year. These things were all careening to the upside when we first started making those calls.

I’m always willing to take some pain for that longer-term gain.

There’s nothing that changed other than there was #Quad2 (Growth and Inflation accelerating) data reported on Friday. I also told you on Friday that bond yields could go higher. Understand that the process is in place to give you confidence. You shouldn’t manage your money emotionally. That’s absolutely not the way to do it.

Subscriber: Your thoughts regarding fixed income. Should I buy and hold the 3-year Treasury?

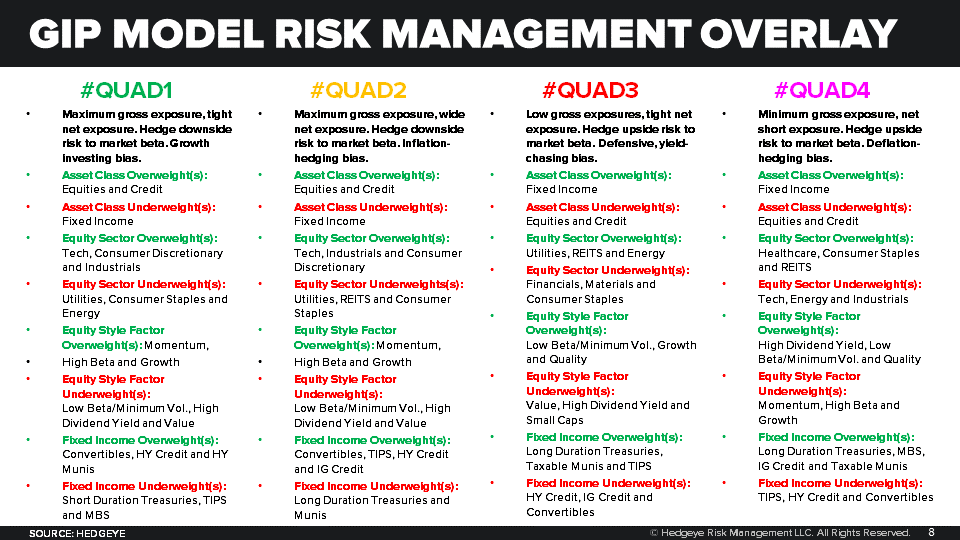

McCullough: The 3-year? That’s interesting. Sure. I think it’s more interesting to get long duration. Again, so if you look at slide 8 in the macro playbook, getting long duration is where you want to be, further out on the curve. So 10s, 20s, 30-year bonds. That’s what I do.

But if you want to buy 3-year paper I’m totally cool with that. The problem with buying 1, 2, 3-year paper is that you’re hostage to the Fed. And the Fed always stays too hawkish too long. That’s why the curve starts to invert.

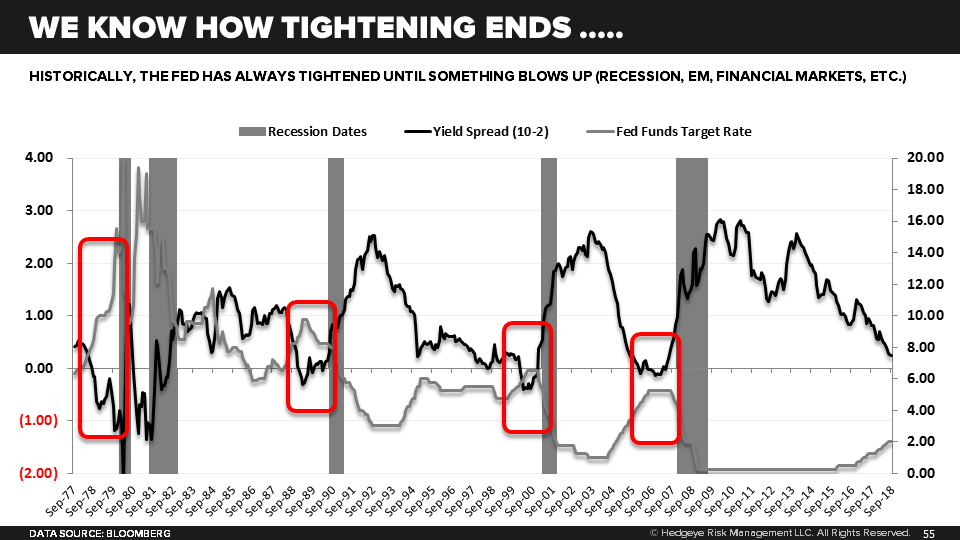

If you look at slide 55 in the macro deck—nothing has changed this morning. The shape of the curve is still 25-26 basis points.

Look at this chart. The yield spread is the 10-year Treasury yield minus the 2-year. The reason this starts to go down late cycle is that the 2-year yield goes up and the 10-year yield starts to go down. The Fed is effectively the 2-year, which is why I’m less interested in buying that. The 10-year is Mr. Market saying, ‘You know what, inflation expectations have peak, global growth has peak and earnings growth in the U.S. have peaked.’ There’s a triple peak.

So what I’m expecting to happen here over the next couple months is for the yield curve to invert. That’d be your target. Why? Because guess who gets hawkish too late in the cycle? The Federal Reserve. And the Fed stops being hawkish, either when you’re headed toward a recession, which we’re not headed toward currently. Or during an Emerging Market or Financial Market crisis, which we’re having right now.

There will be an opportunity for the Fed to go dovish but the current December rate hike expectations are 80%. I expect that will be true. The market now expects the probability of the first rate hike in 2019 is 56%. I expect that’s going to fall further as we go throughout 2019.

Subscriber: With oil turning bullish again and yields moving to the upside, when would you change your call on inflation and yields?

McCullough: That’s another big thing: Oil. Apologies for not mentioning the other big thing driving rates. Oil is the number one factor in inflation expectations. In the last couple days, it went from $68 and change to $71.50. That’s definitely had an impact on rates.

Here’s the main reason why you want to be long bonds. What I’m preparing you for here is the fall in inflation. That’s #Quad4 (Growth and Inflation slowing) in our model. The question I think you’re asking is ‘Did the move in Oil change that?’ No, no, no.

In Q4, Oil would have to go above $90. And in Q1, to make the change in our call, oil would have to go above $110. $90 and $110 is a lot higher than $71.50.

And remember, that’s just one thing. The rest of the commodity complex is collapsing, like corn. That’s agriculture, a big proxy for inflation expectations. Lumber is crashing. Coffee is crashing. There are plenty of problems out there. This is the main reason why the aggregate of the commodity complex, the CRB index, is going to a lower high today because oil stopped going up.

I hope this gives you confidence to be adding to positions in terms of the long bond.

CLICK HERE to watch this video from The Macro Show.

AROUND THE WORLD

A Letter from Hedgeye CEO Keith McCullough (+ special video)

Dear Hedgeye subscriber,

A significant sea change is underway in financial markets. Our forecast indicates U.S. economic growth will accelerate for the ninth straight quarter by the end of 3Q 2018.

This is unprecedented. Indeed, that means it’s literally never happened before in U.S. economic history.

(For the record, our non-consensus analyst team made that call for 2 years.)

The outlook after that looks decidedly grim. And we want you to be prepared.

My goal at Hedgeye is to:

- Deliver you the sharpest, most investable insights available

- Take you deep inside our investing research process

- Teach you the “secret sauce” underpinning our Macro risk management process

As a special thank you for subscribing, click here to watch this video in our educational Macro process series. In this 14-minute video, I’ll walk you through our Macro research process from start-to-finish.

You’ll learn:

- Why the “rate of change” in economic growth and inflation are critical market signals

- How we break down and track financial market data to help you beat other investors

- The ins-and-outs of Wall Street consensus positioning and how to track it

This video should get you fired up about financial markets. It will change how you think about investing.

Here’s the deal.

My co-founders and I started Hedgeye over a decade ago. We had one goal: deliver hedge fund-quality research to everyday investors. Hedgeye was created during the throes of the great financial crisis because Wall Street failed investors. Clueless pundits on CNBC were telling you to buy the dip, as trillions of dollars evaporated from the financial system.

Unlike Wall Street, I’ve never missed calling a bear market. (We actually launched the firm, in August 2008, with a bearish outlook for the U.S. stock market.) We’ve also been appropriately bullish over the years (in 2009, 2013 and late 2016 to be precise).

In other words, we go both ways.

Today, I’d humbly submit to you that our proprietary research process, developed by my team and I, is as strong as it’s ever been.

So take a moment to watch the important video below.

Thank you again for remaining a loyal Hedgeye subscriber!

Sincerely,

Keith McCullough

Chief Executive Officer

THE WEEK AHEAD