“Money, it has been said, is the cause of good things to a good man and of evil things to a bad man.”

The big picture

That may or may not be true inasmuch as the legalization of pot may not expand its user base to infinity and beyond. We’re going to be launching an independent research vertical on marijuana in the 4th quarter. I can’t wait!

Macro grind

The other big thing we’re going to be doing in the 4th quarter is launching into our preferred Q4 Macro Themes portfolio positioning. We’ll be hosting that LIVE video/slide presentation @HedgeyeTV at 11AM EST next Thursday.

I’ll give you a hint on what our #1 Global Macro Theme is going to be: Quad 4 in Q4.

That’s right, unless I go off the rails at 5AM every morning popping some pot edibles, you should be able to proactively predict both my behavior and where I think the most money can be first saved, then made.

BREAKING: “OECD CUTS GLOBAL GROWTH FORECAST”

That’s mainstream “news” this morning. Amazingly, the OECD is the first establishment econ department to cut its growth forecast from the consensus call formerly known as GSR, the “globally synchronized recovery.”

And they’re 9 months late. Thanks for coming out.

In real-time market news the stock market crashes associated with:

- #ChinaSlowing

- #EuropeSlowing

- #EMSlowing

… continue this morning:

- Chinese stocks ended their 2-day bounce, closing down on the session and -23.3% since JAN 2018

- Greek stocks continue to crash, down another -0.6% this am and down -22.7% since JAN 2018

- Turkish stocks continue to crash, down another -1.0% this am and down -20.8% since JAN 2018

I’ll be damned if Mr. Market didn’t mark the peak in all 3 of those markets within the same week of that GSR peaking! Gotta love this game. Gotta love the political spin on it all too.

Allegedly, all of this #slowing stuff has nothing to do with #TheCycle and everything to do with Trump and #TradeWar… but none of the record 9 straight quarters of US economic growth #accelerating (year-over-year) does.

To use the Old Wall media’s favorite word these days, “fascinating.”

Admittedly, I was somewhat fascinated by how fast the UST 10yr Yield ripped to 3.08% in the last few trading days. I was on the road in Texas and when asked on the why, my response was something like this:

- The Setup: Treasury market volatility was at the all-time lows pre the US Wage Inflation report

- Post that #LateCycle Labor report, European Bond Yields ripped to the top-end of their @Hedgeye Risk Ranges

- And the USA got some #LateCycle Quad 2 data for AUG via those Retail Sales and Industrial Production reports

Throw some Macro Tourist advertising about the “Fed Readying To Raise Rates” on top of all that and voila. I get one heck of a buying opportunity in everything I want to have in my p.a. in Q4.

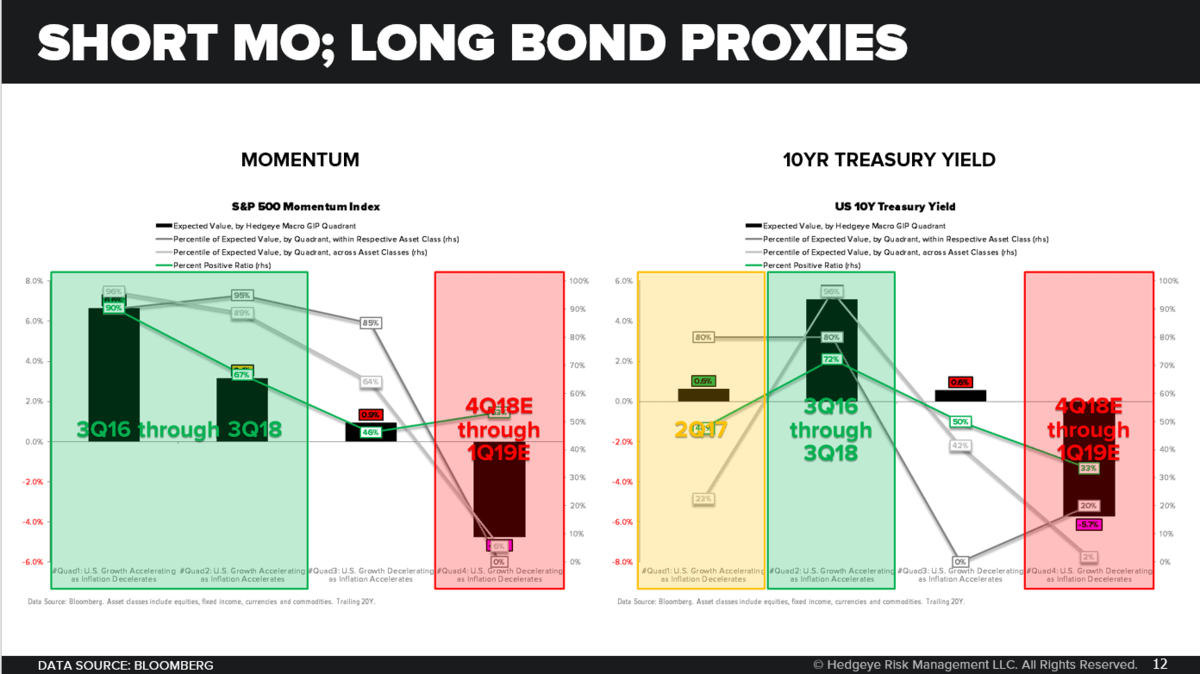

What should your portfolio be long of in Quad 4?

- ASSET CLASS OVERWEIGHT: Long-term Treasuries

- EQUITY SECTORS: REITS, Consumer Staples, and Healthcare

- FACTOR EXPOSURES: High Dividend Yield, Low Beta, Minimum Volatility, and Quality

What should your portfolio be getting rid of heading into Quad 4?

- ASSET CLASS UNDERWEIGHT: Growth Equities and Speculative Credit

- EQUITY SECTORS: Tech, Industrials, and Energy

- FACTOR EXPOSURES: Momentum, High Beta, and Growth

I know. I know. This probably sounds as crazy as it did when we told you to get out of European Equities 1-year ago and out of China and Emerging Markets in January of 2018. I don’t do pot, but I do get crazy!

What’s even crazier about all of this is that if the last 3 weeks are signaling anything, Mr. Market has already beaten me to the punch, selling the worst performing US Equity FACTOR EXPOSURE in Quad 4, Momentum, ahead of me.

All I’ve done so far is move to buying the SECTOR STYLES I didn’t like for the 9-month run in Quad 2 (bond proxies). I haven’t gone all wild and crazy and started shorting something like Tech (XLK), yet.

Pardon the pun, and bear with me. I have one more week to fully re-position (and get this slide deck done!).

Our levels

Our immediate-term Global Macro Risk Ranges (with intermediate-term TREND views in brackets) are now:

UST 10yr Yield 2.88-3.08% (neutral)

SPX 2867-2918 (bullish)

NASDAQ 7871-8033 (bullish)

Utilities (XLU) 53.06-54.99 (bullish)

Shanghai Comp 2631-2735 (bearish)

Nikkei 22507-23737 (bullish)

VIX 11.20-15.22 (bullish)

USD 93.90-95.61 (bullish)

Oil (WTI) 67.00-72.11 (bullish)

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer