This commentary was written by Dr. Daniel Thornton of D.L. Thornton Economics. Thornton spent over three decades at the St. Louis Fed as vice president and economic advisor.

In a letter written to Senator Rick Scott (here) Fed Chairman Jerome Powell said, “We do not anticipate inflation pressures of that type, but we have the tools to address such pressures if they do arise.”

In a Meet the Press interview on Sunday, April 2, Treasury Secretary, Janet Yellen, stated that the Fed has the tools to handle inflation should it start to increase. In a Federal Reserve Bank of San Francisco Economic Letter in 2012 (here) John Williams said, “there is always a risk of inflation rising too high. Let me emphasize that the Fed has the tools to combat such a threat if it were to materialize.”

A strong reason to doubt these claims comes from noting that inflation has been consistently below the Federal Open Market Committee’s (FOMC’s) 2% inflation target in spite the Fed’s more than decade long historically easy monetary policy.

The personal income expenditure inflation rate—the rate that the Fed targets—averaged just 1.6% from July 2009 through December 2019. The inflation rate measured by the consumer price index (CPI) averaged 1.9% during the same period.

If the Fed’s excessively easy monetary policy failed to get the inflation rate up to the 2% target, why should anyone believe that it can pursue a tight monetary policy that will contain inflation should it begin to accelerate?

In his letter to Senator Scott, Powell attempted to allay this concern noting that:

|

In the United States, inflation has run below 2 percent on average for more than a decade. The [FOMC’s] new consensus statement conveys our determination to use our full range of tools to achieve our objectives and to avoid the experience in some countries in which central bank policy rates are pinned near zero with subpar economic performance and the associated downward pressure on inflation and inflation expectations. |

His statement suggests that the FOMC’s more than a decade long easy policy was successful because it prevented the U.S. from experiencing the “downward pressure on inflation and inflation expectations” experienced by other countries.

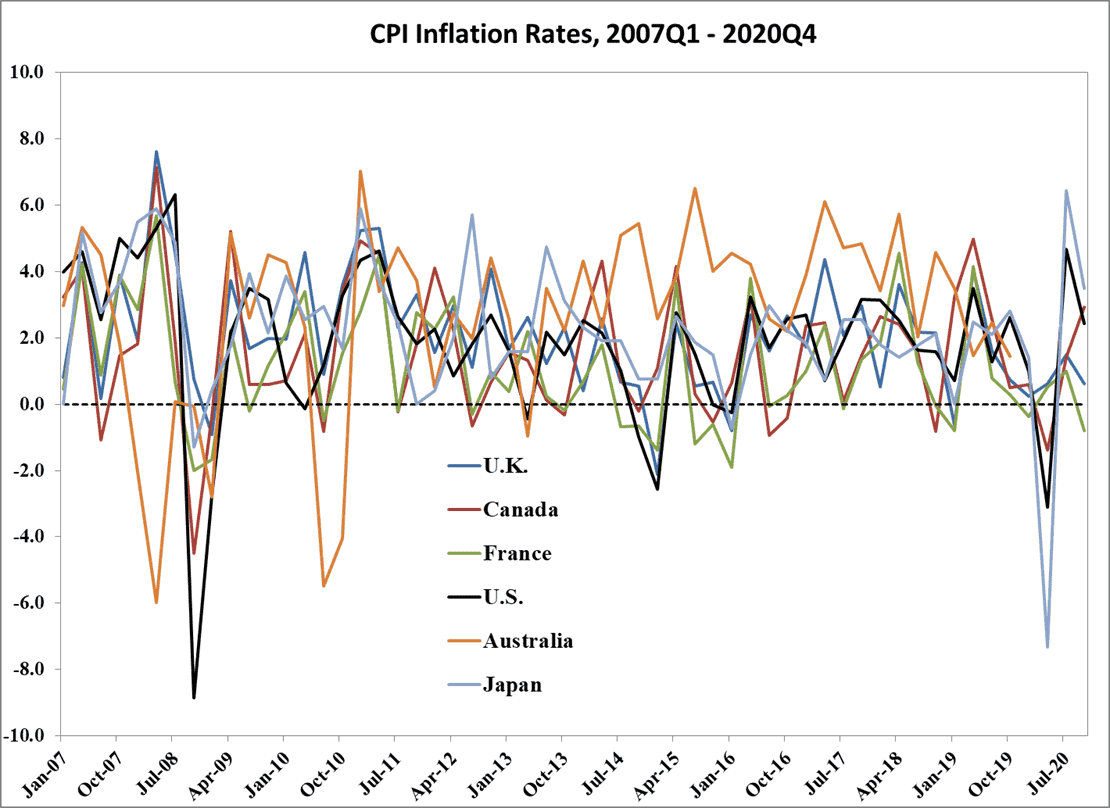

He neglected to mention which countries he was referring to. Apparently it is none of the countries shown in the figure below. This figure shows the CPI inflation rates for Canada, the U.K, Australia, France, New Zealand, Japan and the U.S. from 2007Q1 to 2020Q4.

None of these countries seem to experience any deflationary pressures. The average inflation rates of these countries, save France and Japan, was not significantly different than the U.S. inflation rate.

Japan’s average inflation rate for the period was just 0.3%, but this is only slightly lower than its 0.6% rate for the period 1990 to 2006.

In a recent op-ed in the Wall Street Journal (here), the influential economist, Alan S. Blinder, said he wasn’t worried about inflation because “the Fed knows how to shrink the mountain of bank reserves by selling assets rather than buying them.”

In my previous essay (here), I explained why the Fed wouldn’t be able to control inflation by reducing the money supply sufficiently, even if it were to sell essentially all of the $7.2 trillion securities that it currently owns.

So this tool won’t work. These policymakers need to be specific about the tools they will use to control inflation. The Fed won’t be specific. If it did, it could be held accountable.

There is another reason it won’t be specific—it has no other way to control inflation!

EDITOR'S NOTE

This is a Hedgeye Guest Contributor piece written by Dr. Daniel Thornton. During his 33-year career at the St. Louis Fed, Thornton served as vice president and economic advisor. He currently runs D.L. Thornton Economics, an economic research consultancy. This piece does not necessarily reflect the opinion of Hedgeye.