Overview

On March 19, 2021, we hosted the c-suite of UpHealth ($GIX) for a fireside chat. Tom interviewed Dr. Ramesh Balakrishnan (CEO), Jamey Edwards (COO UpHealth, CEO Cloudbreak), and Martin Beck (CFO), and we came away thinking, “Great story if true, and initially, it sounds true."

Takeaways

- UpHealth has assembled a credible group of offerings that should work well together and increase the value of the whole compared to the stand-alone companies.

- Their market strategy addresses many of the complaints we’ve been hearing from providers, consultants, physicians, and patients. The complaints are captured by buzzwords like integration, value-based care, point solution, hybrid delivery model, population health, ROI, digital health, etc.

- Plain language: patients want to see their own doctor and they want to see them in person or using their phone, whichever is best for them. They also want to use helpful medical apps. Everyone on the provider-side wants that too, but they need the patient data to be collected in the patient history.

- New payment models and the ability to take risk are increasingly available from Medicare and Commercial Insurance payors. The value-based pricing model dramatically increases the money on the table compared to fee for service but also increases the risk.

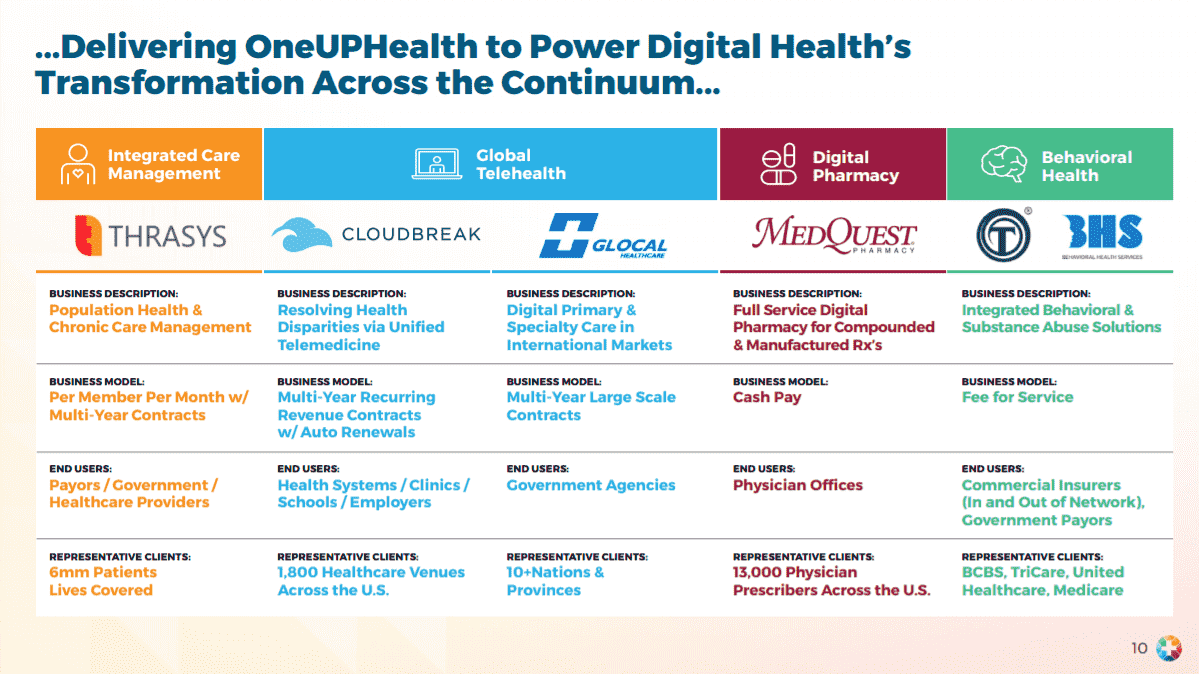

- The UpHealth model is based on a low PMPM model with customers having the flexibility to add combinations of services they’ve assembled; Pharmacy, Telehealth, Care Management, and Behavioral Health.

|

Healthcare Subscribers: CLICK HERE for event details (includes video, dial-in and materials link) |

Call Notes

Lightly edited for length and clarity (emphasis added).

How the deal came together, GigCapital and Cloudbreak, etc.

- Over the last 3 years, the co-founders of UpHealth have collectively been thinking through what a next-generation leader in the digital health space needs to be and how to enable that. The goal was to bring together integrated solutions and bring that whole to the market.

- Everything is centered around what UpHealth calls a virtual, connected care community. It's a platform of assets that create that player.

- The companies have operational depth, maturity, and are profitable in their own right. There are "tremendous" opportunities to accelerate what each is doing individually and as a part of the whole.

- UpHealth needed growth capital - GigCapital2 is not a generic SPAC (specializes in private-to-public equity model, experience of founders, etc.). The quick access to growth capital = accelerated growth in US and internationally.

What got Cloudbreak into the mix?

- JE: When we met with the other companies around 6 months ago (had been talking for ~2 years), the rubber hit the road. We saw the opportunity to bring everything together under one umbrella for physician offices, health systems, payers, etc., and create digitally enabled care communities, as well as the power to collaborate. There are a lot of different things we can do, cross-sell, etc. - it's an opportunity is to reshape health care.

What does integration actually mean here? What does it take (long roadmap or sit in a room and collaborate)?

- RB: It's close to the latter. We are serving these end markets from different angles, so we need uniform messaging (go-to-market customer education - broader capabilities), and then there's product integration - Thrasys serves as the backbone for the aggregation of data, analytic, coordinate workflows, and Cloudbreak provides the platform for outreach around comms and virtualization, Glocal can connect to IoT., etc. - it's all open APIs and built around interoperability. Not a heavy lift - we are in the process of launching the bundled offering.

Great, so capital intensity won't reaccelerate and FCF will line up with income statement etc.?

- MB: The projections are built from the ground-up and do not account for any synergies - revenue or cost. We are confident that there are significant opportunities. The cash flow conversion is fairly high, largely because working capital and capex requirements are modest. You'll see margins in 2021 consistent w/ historical levels at around 12.5% as we invest in sales, marketing, and product development initiatives. The operating leverage embedded comes to the forefront in 2022 - margins should climb to nearly 20% (EBITDA basis).

The Importance of Integration

- Disconnected point solutions are problematic, said Ramesh. Open integrated platforms are important. Customers are trying to manage a bunch of things: access to care, quality of care, health outcomes, and metrics around it for value-based programs.

- To do all of the above, customers need a view of what's happening with patients - patterns, stratification, bucketed into programs, etc. Then, providers must run a range of programs - running virtual care teams, chronic disease management and transition programs, etc. A set of disconnected solutions makes it hard.

- Customers are trying to get to a place w/ better access and outcomes; UpHealth brings an open platform that integrates the core things and is open to plugging things in.

The beauty and dream of integrated care remind me of American Healthways, but how do you help a health system get paid or operate in a value-based world?

- RB: You're right, we're targeting all end markets - value-based programs and fee-for-services. For entities that have taken on population health accountability - health plan or provider group, what we're doing is helping them succeed in the things that they must manage because incentives and payments are attached to that. Even if they aren't in those programs, the delivery side is transforming - UpHealth can help with the new business model - delivering care outside the walls of the hospital. UpHealth gets paid on a subscription model and helps bring funds to customers linked to success.

- JE: You have to do more than drop technology off at the door. We hand them a viable business model that helps with a sustainable advantage. It's the technology plus services and consulting. Everything is about the building blocks that come along with establishing a better local continuum of care. The building blocks for digital health allow for assembly in a way that fits the system's or plan's strategy. Patients don't want a new continuum of care, they want the people they work with to be enabled with digital health tools. We are supportive - a digital health Switzerland. Larger companies will start to cross paths with the people they are trying to serve.

- Cost, quality, and efficiency matter to a hospital. If you can help with those, you've got a well-run, profitable system. UpHealth is structured to solve for those three in a constructive way.

You're in the middle and name health systems, plans, and providers as customers - the consumer isn't there. Is that right?

- RB: Correct. We're not trying to disintermediate the relationship between local health care and the patient/consumer - B2B2C. We help, but don't want to take over that relationship or disconnect patients from their local healthcare systems.

Does Cloudbreak go from a narrow task (translation) to a technology that does lots of things?

- JE: Yes, you've hit the nail on the head. We're in 1,800 venues, doing over 100k encounters per month, and have 14,000 video endpoints. It's not just language services, it's become a health care disparities solutions business (LEP and deaf patients are throughout the system - L&D, inpatient, ER, etc.). Clients were asking for it. Cloudbreak is everywhere - tele-interpretation use case allows for permeation throughout the hospital, which is why we have so many endpoints. Can we add a button for our own telepsychiatry people? Yes. Can we add telestroke? Yes. It's all embedded in language services, launched tele-quarantine during COVID. We listened to what the market wanted and we're now doing tele-everything across the platform. Now we can bring in behavioral, pharmacy, etc. through our partner companies.

Use case for a multi-specialty group practice?

- JE: We're offering a holistic digital health infrastructure, with which they can manage their own medical group and share resources (bring cardiologists in for urgent care issues, for example). Right now, they aren't. But they can use their own resources better. And we can help break down barriers locally (medical group <-> hospitals and tie in payer working w/ Thrasys into the mix).

- Language services - super important - 20-30% of patients across the country speak a language other than English. These patients can't be ignored - they cost the system money if not cared for properly. It's a "digital health super-platform."

- RB: You mentioned direct contracting, taking responsibility for the cost of care - we bring all the authorization and workflows around that part of it too. Oak Street - UpHealth could be a platform for any direct contracting entity out there. We have the largest public health plan as a customer (at Thrasys) and all the workflows around programs, analytics, etc. - all those functions, member outreach, integration with the care team, clinical and community-based networks to become direct contracting for Medicare beneficiary are built-in.

How does the pharmacy piece fit in?

- RB: The model is designed to be a partnership w/ pharmacy and pharmacists that allows a clinical team to manage medications, specifically those that require personalization and compounding. Helping to manage medication regimens that patients are on as an extended member of the care team - again, not B2C. It covers adherence, efficacy, cost of medications, and it's open so could eventually help with value-based PBMs and managing the pharmacy benefit, especially for precision medicine in real time.

- Where does lab sit with all of this?

- The pharmacy facility does offer testing as well - e.g., hormone therapies that require ongoing testing.

Thrasys - hearing your story triggers the memory of things like DB Motion?

- RB: Thrasys is very different from an integration HIE platform. It's being built to enable an integrated model of care. One of the problems with early HIEs (aside from difficulty scaling it), was defined around document exchange vs. structured data and shredding of documents into a longitudinal health record. The integration level wasn't where it needed to be. That's only one piece of it. It was limited to clinical data. What we're talking about is integrated everything - health plan data, clinical side from, public health data, housing data, etc., etc. The analytics and the stratification are the next layers, but then that must be integrated with the workflow of the care team (across the community).

What do you charge an average health system for this?

- RB: For us, the customer becomes an anchor to the virtual community. Then, they can add to it. It's essentially a PMPM model for it - two-tier, low modest PMPM to aggregate info, create a 360-degree view, run analytics, etc. then, there are additional subscription fees associated with incremental programs.

- JE: If you look across UpHealth - it's mostly 3-5-year agreements, a lot of visibility around future revenue, etc. We have a lot of confidence in the model - there's below 5% churn over the last few years. It's a sticky platform because the value of a holistic view is impressive. A lot of health systems are driving a car w/ no dashboard. Digital front doors are not built out, but there's still a lot of work to be done and there's still a lot of white space.

Make the low PMPM more attractive, and then allow them to opt-in to other services?

- RB: The proposition isn't just cost savings. There are additional dollars available to customers. Star ratings are a piece for a health plan. There are quality scores, for example. If you're running a care transition program, CMS has dollars available. We help you get those dollars.

- JE: Cost savings - if you're talking about saving money, that's a losing sttaegy. Save $300k per year, or create $5MM of EBITDA to better serve clients? The latter is the message that we want US Health Care to be talking about.

- RB: Our customers must reinvent themselves around a digital health model.

Value-based care and integration - how are discussions different today vs. pre-COVID?

- RB: The conversations haven't substantially changed because of or w/ COVID. We're not going in saying you can't bring patients into an office or here's an alternative to deliver a disconnected episodic thing. On the managed care side, the conversations are "give us a better platform" as the managed care space evolves. More responsibility on the plans to impact health outcomes. Same conversations. Better information on members, integration of behavioral, etc. The extension of the care team, on the provider side, is something that was always needed.

- JE: What you're keying in on, the situation w/ digital health existed pre-COVID - increasing broadband rates, smartphone penetration, more digitally savvy consumers. COVID-19 accelerated the adoption of the at-home health model. Pre-COVID, digital health tools were alive and well in the hospital - telestroke, etc. saved lives millions of times per year. COVID helped people build muscle memory with telemedicine.

The other piece - the physician groups were forcing us to drive to the office, right?

- JE: Yes...because the whole system is built around the in-person visit. If you were to build the system today, you'd build a virtual first system, right? The conversation has changed because people don't want point solutions - they want easy-to-use platforms that allow them to do more. KLAS just came out with a report saying there will be a second wave of implementations because people chose the "right now" solution vs. the "right" solution during COVID. The right solutions are enterprise-driven, platform-based solutions that allow people to solve more than one commodity - seeing patients at home.

How much of a war chest are you pulling together and what are your thoughts on further M&A?

- RB: We'll think of it as a treasury chest vs. a war chest...

- MB: Pro forma, we'll have $240-245 million or so of cash vs. a $255 million of convertible debt - a solid balance sheet with which to pursue organic growth (sales, marketing, and new product development are on the docket for 2021 and 2022). Also, we will have cash and a public currency to look at selective accretive acquisitions. We'll look for things that enhance our product or service capabilities. Near-term, acquisition opportunities will be bolt-ons or tuck-ins to existing platforms - we wouldn’t add an extra leg of the table, so to speak. We have a lot of M&A experience on the executive team and we will be disciplined - acutely focused on accretive transactions.

Closing comments:

- RB: We didn't touch on the global opportunity - UpHealth is bringing infrastructure to other markets as well. The other thing, we don't think of it as "value-based care" - we want to allow providers to get back to managing health vs. contorting themselves to maximize billing. It's a hard habit to break, but if it doesn't happen, the provider will become a subcontractor.

- JE: The physician office workforce is burnt out - many of them aren't happy with the current status quo. The process is not sustainable. We want to add tools, put technology at their fingertips to help restore meaning to their work.

About the Speakers

Dr. Ramesh Balakrishnan is an entrepreneur who has founded technology companies in multiple industries. He was Director of Application Products at Measurex Corp. and introduced market leading products globally. Dr. Balakrishnan joined Asyst Technologies as Vice president with the successful merger of software spinout. Dr. Balakrishnan then co-founded ePropose and successfully exited the company in 2001. Currently, he is a co-Chief Executive Officer of UpHealth and leads Thrasys, Inc. (the Integrated Care division of UpHealth). Thrasys provides cloud-based solutions for the healthcare industry to share information, coordinate care teams, and manage health with advanced analytics and intelligence.

Martin Beck is the CFO of UpHealth. Mr. Beck, prior to joining UpHealth, was a Managing Director and co-founder of MAT Capital, LLC. Mr. Beck spent a large portion of his career as an investment banker and investor in the healthcare and industrials sectors, including with JPMorgan where specialized in M&A and at Macquarie Capital where he focused on both M&A and principal transactions. Martin also served as Managing Director of Weichai Power Co. where he led International Corporate Development.

Jamey Edwards will be the Chief Operating Officer of UpHealth post-combination and is currently the CEO & Co-Founder of Cloudbreak Health, a leading unified telemedicine company focused on resolving healthcare disparities. Currently performing over 100,000 encounters per month via 14,000+ video endpoints at 1,800 healthcare venues nationwide, Cloudbreak has been recognized as one of the top entrepreneurial companies in the country by Entrepreneur Magazine, and as one of the top medtech software solutions by MedTech Breakthrough, among other awards. Mr. Edwards has been named One of the Top 50 voices in Healthcare by Medika Life, a HIMSS Changemaker and a top 40 Health Transformer by M,M&M Magazine. He is a Board Member for the Los Angeles Chapter of the American Red Cross, American Heart Association, the Partners in Care Foundation, and the Young President's Organization (Santa Monica Bay Chapter).

Please send any questions or feedback to .

Thomas Tobin

Managing Director

Twitter

LinkedIn